March 2022

Table of Contents

- Key Definitions

- Background

- Methodology

- Findings: Relevance

- Findings: Performance

- Findings: Efficiency

- Conclusions

- Appendix A: Logic Model

- Appendix B: Supercluster Program Overview

- Appendix C: Endnotes

Key Definitions

Clusters are dense areas of business activity that contain companies, post-secondary institutions and specialized infrastructure and talent that act as engines of growth by creating jobs, encouraging knowledge sharing, driving business specialization and attracting "anchor" firms.Footnote 1

Innovation refers to the process through which economic or social value is extracted from knowledge in order to produce new or improved products, services and processes.Footnote 2

Innovation Ecosystem commonly refers to the evolving set of actors, activities, institutions and relations, including complementary ones, that are important for the innovative performance of an actor or population of actors.Footnote 3

Innovation Superclusters are hotbeds of innovation with strong collaborations between leading companies and academic and research institutions that can produce new solutions to complex problems and create new technologies. Innovation ecosystem participants are linked through their shared reliance on specialized inputs such as talent and technologies.Footnote 4

A triple helix model of innovation is a collaborative approach involving academia, industry and the government with the aim of generating regional development in the area of innovation.Footnote 5

Background IP refers to all intellectual property that existed or was developed prior to the commencement of a Supercluster project.Footnote 6

Foreground IP refers to all intellectual property that was conceived, produced or developed in carrying out a Supercluster project.Footnote 7

Background

ISI Overview

Launched in 2017-18, the Innovation Superclusters Initiative (ISI) is an Innovation, Science and Economic Development (ISED) program delivered by Innovation Canada. The program is a co-investment initiative designed to promote the growth and development of Canada's most promising regional innovation ecosystems by accelerating economic growth in highly innovative industries, encouraging a collaborative business approach, and positioning Canadian firms for global leadership. The ISI aims to strengthen collaboration among companies and other innovation ecosystem players in key areas of current and future competitive advantage for Canada.

- Budget 2016 announced the Inclusive Innovation Agenda, a plan to propel Canada to the forefront of the future economy. As part of this agenda, $800 million was committed over four years to support the development of five clusters to translate Canada's competitive strengths into commercial opportunities

- As part of the Innovation and Skills Plan, Budget 2017 outlined a priority to accelerate the development of business-led Superclusters that focus on innovative industries, increasing the level of support to $950 million (2018-19 to 2022-23).

- In February 2018, ISED selected five industry-led, not-for-profit consortia in five innovative areas representing current and future competitive advantages for Canada. Funding was approximately $153 million each to the Protein Industries, Digital Technology, and Ocean Superclusters, and approximately $230 million each to the Next Generation Manufacturing and SCALE AI Superclusters. Approximately $17.5 million is allocated to cover ISED operating expenditures.

- An additional $60 million was announced in Budget 2021 (allocated $20 million each to the Digital Technology, Protein Industries, and Next Generation Manufacturing Superclusters).

- Today, the entities continue to advance towards their objective of becoming world-leading Superclusters.

ISI Superclusters and Objectives

Through non-repayable contributions, the ISI supports the five industry-led, not-for-profit entities. These entities are responsible for bringing together the private sector, post-secondary institutions, and other ecosystem players to increase collaboration, increase business research and development, enhance the innovation ecosystems, and enhance productivity, competitiveness and economic growth.

- Digital Technology: Based in British Columbia, this Supercluster aims to unlock the potential of data. Through better datasets and applications of augmented reality and cloud computing, this entity aims to improve service delivery and efficiency in the natural resource, precision health, and manufacturing sectors. Ultimately, this entity seeks to arm Canadians with the best data to drive decision-making and connect the digital and physical worlds.

- Protein Industries (PIC): Based in the Prairies, this Supercluster aims to increase the value of key Canadian crops and serve the expanding middle class in foreign markets, as well as satisfy growing markets in North America and Europe for plant-based meat alternatives and new food products. Through plant genomics that improve nutrition, novel processing technology and digital solutions, it aims to help Canada capture markets for its agribusiness.

- Next Generation Manufacturing (NGen): Based in Ontario, this Supercluster aims to build up next-generation manufacturing capabilities, such as advanced robotics and 3D printing. Ultimately, NGen aims to position Canadian companies to lead industrial digitalization, maximizing competitiveness and participation in global markets. Worldwide, 'Made in Canada' will be recognized as excellence in innovative manufacturing.

- SCALE AI: Based in Quebec, this Supercluster aims to bring sectors such as retail and information and communications technology (ICT) together to build intelligent supply chains. Links between businesses will become faster and easier as new tools predict where and when products are needed. Ultimately, the Supercluster aims to make Canada a global export leader by capturing new market opportunities.

- Ocean (OSC): Based in Atlantic Canada, this Supercluster will tap the strengths of the industries operating in Canada's oceans (e.g., marine renewable energy). By harnessing emerging technologies, this Supercluster aims to digitize and optimize marine operations, maximize sustainable approaches to resources, and increase safety for those operating in marine environments.

Program Activities

Each entity is guided by a unique strategy that describes the activities they intend to pursue to build their innovation ecosystems. Entities undertake projects and/or redistribute funding to ultimate recipients (e.g., Canadian firms, post-secondary institutions etc.) through "calls for projects" or similar exercises. Each entity conducts its own independent processes with unique project selection guides, selecting projects that best align with their strategy. Although each entity's programs and activities are unique and dependent upon the strengths and needs of their ecosystems, projects and activities eligible for co-investment under the ISI are structured broadly around five general themes.

- Technology Leadership: Activities to advance technologies central to the Supercluster's future competitiveness and to build a technological advantage for the Supercluster in order for Canada to demonstrate its global commercial leadership (e.g., collaborative R&D project, demonstration or prototype development project with benefits for multiple firms, etc.).

- Partnerships for Scale: Activities serving a group of the Supercluster's members to enable their growth by increasing domestic demand for products and services or facilitating expansion (e.g., supply chain development; offering business mentoring, consulting and coaching; partnering with a public entity that provides capital and financing, etc.).

- Diverse and Skilled Talent Pools: Activities that involve industry in enhancing labour force skills and capabilities or address industry talent needs (e.g., developing industry curricula that focuses on addressing their talent needs, a recruitment campaign to repatriate Canadian talent to the cluster, re-training programs for existing workforce, assessment of industry's workforce or anticipated needs, etc.).

- Global Advantage: Activities that position the Supercluster as world-leading in its field enabling firms to seize market opportunities and attracting international investments and partnerships (e.g., Supercluster promotion, investment attraction to cluster region, studies to identify new global markets for cluster products and services, etc.).

- Access to Innovation: Activities that provide a benefit to members over time through investments in services, resources or assets (e.g., installing cutting edge equipment, access to specialized technical services, IP support etc.).

Projects Funded

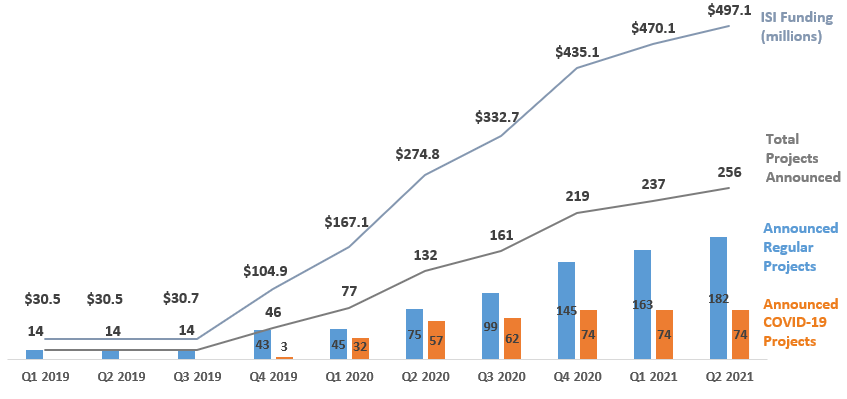

As of September 30, 2021, the Superclusters have allocated $497.1 million to 256 projects (182 Regular projects consisting of Technology Leadership and Ecosystem Development projects and 74 COVID-19 projects). The average size of Regular and COVID-19 projects based on ISI funding and industry/partner contributions is $4.7 million per project.Footnote 8

The ISI's co-investment model requiring entities to secure funds from industry to match federal government contributions at a minimum 1:1 ratio (excluding COVID-19 projects). For each entity, ISED funding for eligible administration and operating costs may cover up to 11.25% of ISED's total contribution.

Figure 1: Number of Announced Projects by Stream and Funding ($M)

This table contains data as of September 30, 2021.

Program Delivery Model

Governance, Target Population, and Stakeholders

Overall responsibility for administration and oversight of the Contribution Agreements with the five Superclusters lies with the Minister of ISED and Innovation Canada. Each Supercluster is an independent, not-for-profit corporation with its own industry-led Board of Directors that is responsible for its strategic direction, financial accountability, and governing policies. As stipulated in their Contribution Agreements, each entity is required to make best efforts to ensure the Board is representative of the Supercluster ecosystem and significantly represents Canada's multicultural diversity, including Indigenous peoples and visible minorities. Each entity also has an executive team and staff responsible for the administration of entity programs and activities.

The target population for the ISI program are ultimate recipients (e.g., companies, universities, etc.) who participate in ISI-funded projects as part of project consortiums. Ultimate recipients enter into Master Project Agreements with their respective Supercluster that provide an overview of project objectives and responsibilities.

By definition, clusters include a broad spectrum of key stakeholders with differing levels of involvement and participation. Although the ISI is the cornerstone initiative for developing Superclusters in Canada, the program is not expected to achieve this outcome in isolation from other federal programs and sustained effort from industry.

ISI stakeholder groups include:

- Project consortia participants (e.g., members participating in projects)

- Federal and provincial government departments/agencies involved in innovation programming and providing public sector funding to the entities or their members (e.g., National Research Council and Regional Development Agencies)

- Partner organizations involved in delivering entity programming (e.g., universities)

- Other actors benefiting directly or indirectly from Supercluster activities (e.g., members, industry or economic development associations)

Methodology

About the Evaluation

An evaluation of ISED's Innovation Superclusters Initiative is required in accordance with the Treasury Board Secretariat Policy on Results.

The objectives of this evaluation are to assess the relevance, performance, and efficiency of the program in accordance with the Treasury Board Secretariat Policy on Results and Directive on Results.

The scope of the evaluation includes each of the five Superclusters and covers the period from April 1, 2017 to March 31, 2021. It examines immediate-term outcomes and early progress towards intermediate outcomes.

The evaluation was conducted in-house by ISED's Audit and Evaluation Branch. The evaluation used a results-based approach, examining the achievement of expected outcomes, as identified in the ISI logic model in Appendix A.

All evaluation findings and recommendations were supported by at least three lines of evidence to the extent possible.

Evaluation Areas and Questions

The evaluation examined the following areas and questions.

Relevance:

- Unique and Demonstrable Need: To what extent is there a demonstrable need for the Innovation Superclusters Initiative (ISI)?

Performance:

- Fostering Collaboration: To what extent has the ISI contributed to increasing private, academic and public sector collaborations?

- Technological Investment and Development: To what extent has the ISI contributed to increasing the private sector's investment in technology research, development, demonstration and commercialization activities?

- Developing Regional Innovation Ecosystems: To what extent has the ISI contributed to the growth of regional innovation ecosystems?

- Commercialization: To what extent has the ISI led to the development and commercialization of new or improved products, processes or services?

Efficiency:

- Program Design and Delivery: To what extent is the ISI delivery model an efficient approach for developing Superclusters in Canada?

- Has the ISI been implemented as planned?

- Have lessons learned been identified and implemented to improve program design and delivery?

Data Collection Methods

Four data collection methods were used to support the evaluation.

Literature and Document Review: A review of literature and documents was conducted to help to gain an understanding of the current need for the Innovation Superclusters Initiative, as well as each entity's unique suite of programs and activities. Furthermore, the examination of documents helped to gain an understanding of each entity's technological and ecosystem development projects and priorities. The review of documents included a 2021 survey commissioned by the Program.

Performance, Administrative and Financial Data Review: Performance, administrative and financial data collected by ISED and each Supercluster was analyzed to provide evidence of progress made towards achieving expected outcomes and to assess the efficiency of its delivery model. Where possible and relevant, Gender-Based Analysis (GBA+) was incorporated into the evaluation.

Virtual Interviews: A total of 71 virtual interviews using MS-Teams were conducted jointly by AEB and a consultant commissioned by the Program across the following stakeholder groups to gather diverse perspectives on the relevance, performance and efficiency of the ISI: Project participants including businesses, industry associations and academia; Supercluster executives and management; Supercluster Board of Directors; ISED program management; Other senior government officials; and Provincial government representatives.

Case Studies: Five case studies were conducted of ISI-funded technology leadership projects completed over the evaluation period (one per Supercluster). These case studies aimed to provide detailed anecdotal examples of the outcomes of ISI funding, along with gathering the views of project consortium participants. Each case study included a document review and 2-4 interviews with project partners.

Challenges for the Evaluation

The evaluation encountered three challenges, outlined below.

- Attribution: The presence of other funding partners made isolating and measuring the direct impact of the federal government's contribution challenging. To mitigate this challenge, interview questions were designed and articulated in a way that respondents could answer, to the extent possible, the incremental impact of ISED's funding to the ISI and each Supercluster.

- Time Factor: The timing of the evaluation limited the availability of information on the intermediate and long-term outcomes of the ISI. Intermediate and long-term outcomes require more time to materialize beyond the end of the current funding period (i.e., 2022-23). Programs such as the ISI require sufficient time to generate desired outcomes and cluster theory indicates that cluster development is a long-term process. To address this limitation, anecdotal evidence for intermediate outcomes was collected, where possible.

- Respondent Bias: Given that some interview participants were involved in program delivery or are funding recipients, there is the potential for respondent bias. As such, the findings may be positively biased. To address this, the purpose of the interview and strict confidentiality was clearly communicated to participants and responses were cross-validated across stakeholder groups as well as other lines of evidence.

Findings: Relevance

Finding 1: There is a strong need for the development of innovation ecosystems in Canada. The ISI uniquely addresses this need via its collaborative approach and catalyzing effect on R&D investment for high-growth projects.

There is a demonstrable need for innovation ecosystems (clusters) in Canada.

The document review highlighted a need for innovation ecosystems in Canada as it relates to:

- The need to enhance the competitiveness of Canadian companies;

- Addressing Canada's innovation and commercialization gap;

- Improving collaboration between public, private, academic and not-for-profit sectors; and

- Increasing the translation of promising Canadian ideas and research into commercial outcomes.

Interviewed stakeholders echoed that there is a strong need for the development of innovation ecosystems:

- Canada's innovation ecosystems have traditionally been weak due to their siloed nature and lack of cohesion, meaning different organizations do not communicate well or connect to each other in a collaborative manner.

- Canadian under invests in R&D relative to other countries. According to OECD data, Canada's R&D spending in 2019 was 1.6% of GDP compared to 3.2% for Germany and 3.1% for the U.S.Footnote 9 Some interview participants felt that Canada does not have a strong self-starter innovation culture and that there is a level of risk aversion.

- Canada is largely a natural resources based economy and must invest more in innovation-driven enterprises, as that is where global growth is.

- Canada's provinces have unique strengths relative to one another, but these strengths are not leveraged or well connected.

It was generally agreed that the need for the development of innovation ecosystems has changed over time. Interviewees noted this as mainly being due to the recent advances in machine learning and AI, which is intersecting with manufacturing. Thus, opportunities need to be approached in a different way (e.g., collectively) than before.

With respect to the importance of clusters, the Chair of Ontario's Panel on Economic Growth and Prosperity noted that "strengthening clusters can lead to increased productivity, economic growth, and prosperity because clusters foster interactions that can energize the regional economy."Footnote 10

The ISI aligns with the needs of the innovation ecosystems.

According to the document review, in order to align their program and activities with the needs of their members and innovation ecosystem, each Supercluster developed a unique strategy that guides its technology leadership and ecosystem development projects and activities. AEB's review of each strategy shows that the unique program suite adopted by each Supercluster is based on the distinctive needs of their ecosystem as well as its strengths. This is consistent with the idea of a "made-in-Canada" approach to cluster building that emphasizes the industry-driven nature of the ISI. Each Supercluster has also made efforts to align programming with industry needs through consultations and engagement with innovation ecosystem actors, particularly industry.

Stakeholders interviewed remarked that the ISI uniquely addresses the needs of the innovation ecosystem by focusing on sectors with high growth opportunities via its triple helix model of innovation, which is a collaborative approach involving academia, industry and the government with the aim of generating regional development in the area of innovation. By introducing more and more organizations into an ecosystem, each entity is able to build knowledge and reapply that knowledge to other organizations, thereby organically building the ecosystem through these relationships. In addition, interviewees noted that by requiring project participants to invest their own capital, R&D investment in Canada is stimulated, thereby helping companies scale up faster than would otherwise be the case. Further, the governance model and structure of each Supercluster provides accountability to ensure outcomes are driven, while their management and executives provide advice (e.g., on intellectual property or regulatory issues) to companies due to their experience in the space.

Some interviewees highlighted the unique role of specific Superclusters, rather than speaking generally. For example, it was noted that Scale AI is helping to link geographic areas of AI excellence in Canada (e.g., Montreal, Toronto), thus contributing to the dissemination of AI research and knowledge from one region to other regions. Additionally, for PIC it was noted that ecosystem development is the key to success for the agriculture sector. For example, there are numerous facilities that companies require for ingredient processing work that few can afford and capital investments in these types of facilities is comparatively low in Canada. Therefore, the partnerships created via the ISI are critical for leveraging existing facilities and resources and incentivizing investment in new facilities rather than having this work conducted outside of Canada.

With respect to the role for government in cluster development, it is noted a source indicated that "the key role for government is that of enabling – whether in the form of providing direct access to finance or in less direct ways through the creation of enabling policy frameworks and strategic action plans."Footnote 11

The ISI does not duplicate existing cluster support programs.

The literature and document review highlighted a number of complementary programs in CanadaFootnote 12 :

- Supercluster Support Programs (NRC): Projects supporting Supercluster program objectives, involving a range of research and technical services, foundational R&D, knowledge mobilization, and pre-commercialization activities.

- Collaborative R&D Programs (NRC): A national network of researchers and facilities with a triple helix model of collaborators working on discoveries and technological breakthroughs to advance specific objectives in a variety of scientific disciplines.

- Industrial Research Assistance Program (IRAP – NRC) – Eureka Clusters: An international network for market-driven industrial R&D that includes over 40 global economies. Eureka Clusters are thematic programmes driven by communities of large companies, SMEs, universities, research institutes and end users. Through Canada's associate membership in EUREKA, Canadian innovators have a new advantage in accessing technology, expertise, and markets in Europe and beyond.

- Agri-Science Program (Agriculture and Agri-Food Canada): Provides support for pre-commercial science activities and research in the agriculture and agri-food sector. The clusters component of the program focuses on mobilizing partnerships among industry, government, and academia, while the projects component aims to support shorter-term research activities.

- Regional Innovation Ecosystem Stream (FedDev Ontario): Non-financial support for business innovation including supporting the development of clusters and consortia, thereby fostering peer support, mentoring and business opportunities.

There was consensus among interviewees that the ISI does not duplicate existing programming in Canada. It was noted that the collaboration component of the ISI is a key differentiator and helps match smaller start-up companies with the right businesses – something that other programs do not do. According to literature, given Canada's small population relative to its size, collaboration between Canadian firms allows them to share resources, reduce costs and decrease risk, helping them to become more productive, profitable and innovative.Footnote 13 The ISI was remarked as being national in scope, cross-sectoral, commercialization-focused, and helps companies scale up and bring projects to maturity more quickly. Further, the ISI is unique because it is industry-led – the Board of Directors for each SC can identify broad areas of policy and innovation that need focus. Therefore, because projects are reviewed from an industry lens, they tend to be more commercial results focused than other programming. Further, since it is one step outside of government, it was pointed out that it is more streamlined and less bureaucratic.

Although there are national cluster agencies elsewhere (e.g., Japan, India, Mexico, Russia, etc.), the literature review found that the European Union has one of the most advanced cluster support networks in the world, with the three main cluster support networks being the European Cluster Observatory, European Cluster Excellence Initiative, and European Cluster Collaboration Platform.Footnote 14 Literature indicates that national cluster programs in Europe place a high degree of importance on developing clusters focused on emerging industries (e.g., digital, logistical services, etc.) and technologies (e.g., automation, artificial intelligence, etc.).Footnote 15

Findings: Performance

Finding 2: The ISI has contributed to fostering collaborations between the private, public, academic and not-for-profit sector primarily through funding projects that aim to: accelerate the development and adoption of advanced technologies; address unique ecosystem gaps and challenges; and respond to the COVID-19 pandemic.

All Superclusters have facilitated collaborations through funding and supporting projects that aim to develop and advance technologies and address unique ecosystem gaps.

The document review and interviews indicated that one of the ISI's key objectives is to increase the scale and scope of collaborative activities, particularly through facilitating partnerships and connections between ecosystem players (i.e., companies, academia, etc.). Each Supercluster's five-year strategy emphasizes a focus on building a collaborative environment conducive to creating meaningful relationships such as those between technology suppliers and technology adopters.Footnote 16

Over the evaluation period, organizations participating as members in each of the Superclusters collaborated primarily through involvement in one of three types of projects:

- Technology Leadership (Regular Stream): All entities created program streams (i.e., unique areas of technological focus) that allocate funding to projects that accelerate the development, adoption and commercialization of advanced technologies by firms (Annex B). During the evaluation period, 93 projects were launched.

- Ecosystem Development (Regular Stream): Based on the unique set of challenges faced by their ecosystem, entities funded projects that aim to address ecosystem gaps such as skills and talent, SME scale up, and global branding. During the evaluation period, 52 projects were launched.

- COVID-19: Three out of five superclusters (NGen, Digital Technology and SCALE AI) funded projects that contributed to producing health solutions and supporting Canada's response to the COVID-19 pandemic. During the evaluation period, 74 projects were launched.

Figure 2: Distribution of All Supercluster Projects Announced and Launched between 2018-19 and 2020-21 (n=219)

The number of partners per Supercluster project reflects the success of the Superclusters in facilitating multi-partner collaborations.

Documents, interviews and case studies indicate that overall, the Superclusters have been effective in building multi-partner project consortiums. More specifically, the Superclusters foster connections between potential project partners both informally through cluster outreach and ecosystem events and formally through active efforts to identify complimentary partners.

Case studies indicated that Supercluster outreach and ecosystem events catalyzed "serendipitous" encounters between organizations with complementary capabilities (e.g., technological solutions), leading to decisions to submit a joint proposal for a Supercluster project. Case studies and interviews also showed that the Superclusters actively assisted project applicants in identifying complementary organizations during the project application and review phases. In one case study, the Digital Technology Supercluster identified complementarity between two organizations that had submitted separate project proposals and proceeded to facilitate discussions to examine the possibility of joining together to pursue a larger scale and potentially more impactful project. Project consortium participants viewed the Digital Technology Supercluster as instrumental in fostering complementarity while reducing the potential for duplication.

The prevailing opinion among project consortium participants interviewed for the evaluation was that the Superclusters have been successful in fostering collaborations through activities such as one-on-one match making and collaboration events. Project data corroborates this assessment showing on average, across all technology leadership and ecosystem development projects launched up to September 30, 2021 there was an average of 5 participants per project. The PIC and Digital Technology Superclusters had the highest average number of participants per project, while the NGen and SCALE AI Superclusters had a lower average relative to their counterparts.

Program reporting indicates that as of September 30, 2021, 38% of project partners for Regular Stream projects across all Superclusters were from academia/research institutions, not-for-profits and other government organizations while 62% were private sector partners (i.e., SMEs and large enterprises).

Figure 3: Average Number of Partners for Regular Stream Projects Announced and Launched between April 2018 and September 2021 (n=183) (COVID-19 projects excluded)

A horizontal yellow line shows an overall average number of participants per regular stream project of 5 across all five Superclusters.

Finding 3: There has been a high degree of engagement from innovation ecosystem players, reflected in the increasing number of members annually joining the five Superclusters. Each Supercluster hosts a unique array of outreach and engagement activities that have contributed to fostering stronger connections among members.

All Superclusters have attracted a high degree of participation from innovation ecosystem players, reflected in the rising number of organizations joining each entity annually.

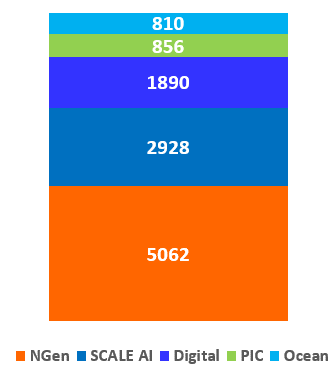

Documents and performance data indicate that the total number of organizations becoming members of the Superclusters has risen from approximately 1,300 in 2018-19 to over 7,000 as of September 2021, representing an increase of roughly 5.4 times since the Superclusters were launched. Although each Supercluster has a unique membership structure, they all operate according to an open membership model that provides organizations of different sizes and capacity with low barriers to entry. Interviews suggest that the diverse range of membership sizes is potentially due to some Superclusters such as PIC having a more narrow focus on specific sectors (e.g., plant protein food) while others such as NGen are broader. Due to unique membership data categories used by each Supercluster, it was not possible to conduct an in-depth analysis of member characteristics.

Supercluster Annual Reports also suggests that a significant proportion of Supercluster members are participating in projects. For example, as of 2020-21, 37% of Digital Technology Supercluster members and 68% of PIC Supercluster members were involved in a Supercluster project.Footnote 17 While some organizations may join a Supercluster and not participate in a project, they have access to resources such as networking events and membership databases.

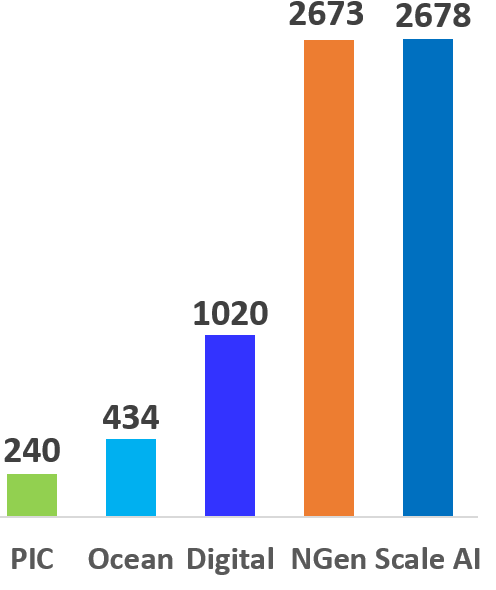

Figure 4: Distribution of Supercluster Membership as of September 2021 (n=7,045)

Each Supercluster engages their innovation ecosystem through extensive outreach and engagement activities that foster stronger ecosystem connections and communities.

The document review and interviews indicate that each Supercluster conducts extensive outreach and engagement activities to not only facilitate potential project collaborations, but to engage their innovation ecosystem and build connections. Each Supercluster's activities are diverse and include, but are not limited to, conferences, project workshops, information seminars and virtual member events that provide opportunities for members to exchange ideas regarding possible technology projects, identify potential partners with synergies, and attract potential investors. Annual reporting by the Superclusters showed that as of March 31, 2021, their activities have included approximately 569 outreach and ecosystem activities (e.g., workshops, conferences) which have reached approximately 13,281 participants and organizations over the evaluation period.Footnote 18

Finding 4: ISI-facilitated collaborations and connections are beneficial to innovation ecosystem participants, particularly private sector members such as small and medium-sized enterprises. Entity members participating in projects establish connections that in some cases, may not have occurred and are leading to new or continued engagement after completion of a Supercluster project. There is an opportunity to foster greater collaboration between the Superclusters.

ISI-facilitated collaborations generate benefits for project consortium partners.

Interviews and case studies show that project consortium participants benefit from involvement in a Supercluster project by establishing partnerships that may not have otherwise occurred and build upon them through continued post-project engagement. Private sector firms, particularly SMEs, have the opportunity to work with different innovation ecosystem players (e.g., multinationals on technology projects, acquiring increased knowledge about the potential applications of emerging technologies (e.g., AI), having the opportunity to access partner facilities and equipment, and gaining an increased awareness of the needs of other businesses, including technology end users. Furthermore, interviews suggest that the ISI has allowed small Canadian firms to participate in high-profile and impactful projects, allowing them to access mentorship, guidance and support from more experienced organizations which is particularly important for helping promising firms to scale-up.

Participation in Supercluster projects has also benefited large, multinational firms by providing them with an opportunity to connect to Canadian businesses. Interviews indicated that a large, globally renowned technology company credited the Digital Technology Supercluster with facilitating a series of technology projects with small Canadian companies that would likely never have occurred without the entity acting as an intermediary and connector.

The most common partnership reported by survey respondents were those with an academic or research institute (17%) and a small or medium-sized enterprise (16%). The least common partnership reported was with an incubator or accelerator (3%) and an industry association or agency (5%).

Case Study Highlights

Precision Agriculture to Improve Crop Health (Digital Supercluster): SMEs participating in the consortium indicated that in light of the project's positive results, they were either in the process of exploring or already engaging in further collaborative R&D activities outside of the original Supercluster project. Two companies indicated they would continue to develop and refine their products and technologies to support future collaborative activities and partnerships with the lead firm.

There is an opportunity to increase information sharing between the Superclusters and to identify opportunities for greater communication and collaborative activities.

Interviews and case studies indicated that while each Supercluster has been effective in fostering multi-partner collaborations in their respective areas, there is an opportunity to increase cross-Supercluster communication and identify potential opportunities for collaborative activities.

Some interviewees noted that given the ISI's early stages of implementation, it is understandable that each Supercluster is primarily focused on their unique domains. However, several stakeholders noted that as the superclusters mature, in addition to identifying opportunities for the Superclusters to work together, ISED could play a role in facilitating greater communication between the entities through identifying mechanisms or fora to share lessons learned and knowledge regarding topics such as common areas of interest, project administration and cluster development. ISED does have recurring monthly calls with all Supercluster Chief Executive Officers (CEOs), biannual meetings with Board Chairs and senior officials, and has established working groups between ISED and Supercluster staff on data and communications. In addition, the Superclusters hold regular meetings between their respective CEOs and Chief Technology Officers.

Interviews also indicated that there is an opportunity for ISED to actively facilitate the identification of common areas of interest or potential areas of overlap between the Superclusters. These activities would help to ensure that each Supercluster's activities are not siloed and help to improve stakeholder awareness of not only how each Supercluster relates to one another, but how they contribute to the overall objectives of the ISI program at a broader national level.

Case Study Highlights

The OceanVision Project (Ocean Supercluster): Organizations participating in this project noted that there is potential for cross-pollination and collaboration across the various Superclusters. In the case of the Ocean Supercluster, interviewees felt this was particularly true given that the Ocean Supercluster is primarily focused on Atlantic Canada and has less of a West Coast scope. It was noted that while the Ocean Supercluster has engaged in meetings and discussions with the Digital Technology and SCALE AI Superclusters on cross-cutting digital technology interests, no formal collaboration has emerged to date, but there is opportunity to do so.

Recommendation 1: ISED Innovation Canada should identify and implement approaches to facilitate and encourage collaboration and sharing of information and best practices across the Superclusters.

Finding 5: The ISI is contributing to increasing the private sector's investment in technology research and development activities through funding collaborative technology projects that are incentivizing firms to develop, adopt and commercialize technologies. The Superclusters are attracting partner funds for technology development projects that exceed federal investments.

All Superclusters have funded collaborations between innovation ecosystem actors focused on projects that incentivize firms to develop, advance and adopt advanced technologies.

In the current knowledge-based economy, the development, adoption and application of innovative technologies by Canadian firms, especially SMEs, is necessary to increase their current and future competitiveness nationally and globally. Under the ISI's co-investment model, the Superclusters have facilitated and invested in collaborative technology leadership projects focused on a broad set of advanced technologies such as artificial intelligence to address industry challenges, while improving the productivity and competitiveness of Canadian firms.

Given the ISI's industry-driven approach, each Supercluster defines a unique array of technology leadership programs most relevant to their respective innovation ecosystems (Annex B). The document review showed that these programs cover a variety of areas including, but not limited to, encouraging the adoption and commercialization of AI technologies in Canadian supply chains; increasing the application of Industry 4.0 technologies for advanced manufacturing; and accelerating the diffusion of digital technologies in ocean, health and agricultural industries.

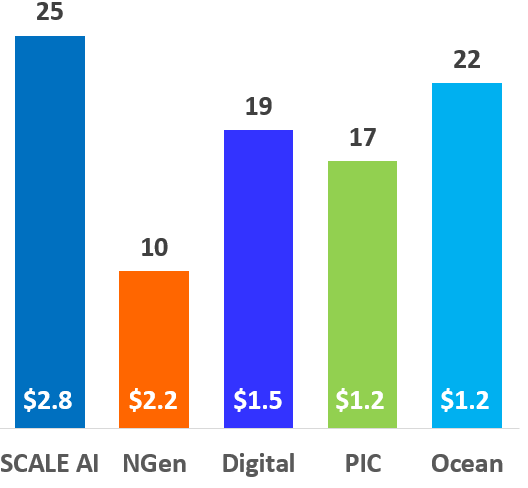

Performance data indicates that all Superclusters are attracting matching funds from industry and other partners for Technology Leadership projects that exceed a 1:1 ratio compared to federal investment. As of March 31, 2021, the overall ratio of industry and partner contributions to federal contributions was approximately 1.6:1 for all Technology Leadership projects, with individual supercluster ratios ranging from 1.2:1 (i.e., Ocean and PIC Supercluster) to 2.8:1 (SCALE AI).

Figure 5: Distribution of Technology Leadership Projects Announced and Launched between 2018-19 and 2020-21 and Amount Invested per Federal Dollar from Partners (n=93)

ISI co-funding for technology development projects catalyzes and incentivizes private sector participation and co-investment.

Interviews and case studies indicated that ISI funding for technology development projects acts as a catalyst for securing additional private sector and partner investments. This is particularly important given the low level of R&D investment among Canadian firms relative to OECD counterparts. Project consortium participant interviews indicated that ISI co-funding helps to reduce the risk associated with innovative activities and incentivizes participation. Without the ISI, many stakeholders felt that private sector investment into technology research and development may not have occurred to the same level or degree and that many project partners may not have been involved in technology projects or decided to co-invest funds. For example, in the case of SCALE AI, interviews suggest that while major companies such as Air Canada and Boeing may have invested in AI research and development independent of the supercluster, SME members would have had less interest, internal capacity and resources to develop and/or adopt AI solutions and technologies for their businesses.

Many project participants indicated that they would not have engaged with one another in technology development without involvement in an ISI-funded project. Interviews suggest that the Superclusters have facilitated non-ISI technology development collaborations through connecting organizations that decided to pursue a collaborative project without seeking the Supercluster's financial support.

Case Study Highlights

Precision Agriculture to Improve Crop Health (Digital Supercluster): SMEs participating in this project indicated that co-funding from the Supercluster was critical for their companies' ability to participate in the project. For one SME, the project allowed the company to test and share its technology with end-users, leading to valuable feedback for further product improvement. For a second SME, the project allowed the company to verify and validate the design and implementation of its software, resulting in information used to refine the product. Overall, the project is leading to new technology that will allow the Project Lead to pursue new business directions and follow-on activities.

ISI technology leadership projects have provided opportunities for firms to not only develop new technologies, but adopt and improve existing ones.

Interviews, case studies and documents indicate that ISI funding has allowed companies to develop new technologies. For example, the Digital Technology case study showed that the project led to the development of a new technology that has become central to the project lead's current technology portfolio and will become a key focus of the company's future business activities. In addition, according to the NGen case study, the Supercluster accelerated industry adoption of 4.0 technologies and reduced risks associated with the project. Project participants also indicated that while the project would have normally taken 10 years, it only took three years due to NGen's involvement. Finally, in the SCALE AI case study, the project led to the adoption of AI and machine-learning software among SMEs that is allowing companies to develop new solutions to solve their supply chain challenges.

84.6% of respondents to the survey who had completed their projects (22 out of 26) noted that the project provided their organization with support to access or develop innovative and/or disruptive technologies.

Finding 6: The ISI has facilitated ecosystem development activities to address known industry challenges, de-risked collaborative innovation projects, and helped connect organizations with complementary expertise.

The ISI has contributed to ecosystem development by establishing dialogue between ecosystem stakeholders, identifying and addressing innovation ecosystem gaps, and enhancing existing strengths.

According to interviews, the Superclusters play a key role in identifying ecosystem needs and areas of potential and then defining activities and projects around broad ecosystem-level goals, which includes a specific funding stream for ecosystem development. Interviews found that the Superclusters act as a galvanizing point around specific opportunities and problems faced by Canadian industry and de-risk collaboration and innovation by reducing private sector costs. The Superclusters connect companies with each other, including connecting companies to entities with key expertise and to end users of their products. Consortium partner interviews identified numerous instances in which the Superclusters helped to establish the initial connections amongst partners (e.g., via Supercluster member lists, conferences, introductions/referrals, and ecosystem development activities).

By helping bring together organizations' complementary skillsets and expertise via collaboration, the Superclusters are building awareness of the capabilities in industry and academia.

For example, it was said that the Scale AI Supercluster helped diffuse knowledge regarding the benefits of AI and helped businesses generate more data that can be used in AI applications. It was also said that receiving funding from the Superclusters provides a level of product validation, which also spurs interest among end users and financial investors. While interviews identified Supercluster activities aimed at increasing the domestic talent pool through training and upskilling, interviewees noted that the Superclusters could do more in engaging academia to develop HQPs and address domestic gaps in key skills areas where Canadian companies currently rely on hiring foreign labour.

Finding 7: In support of ecosystem development, the ISI is helping to spur job creation and employ underrepresented groups. Although the Superclusters are at different phases of implementation, numerous skills development and training programs have also been developed, including ones targeting underrepresented groups. However, it is too early to assess the full impact in these areas and the consistency and availability of data limits assessment of results.

All of the Superclusters are focused on developing a unique set of skills and talents for their ecosystems.

According to interviews, some Superclusters embedded skills development when they were first established, while others are only just beginning to focus on it (e.g., the Protein Supercluster launched its Capacity Building Program in 2020-21). Interviews and the document review highlighted examples of skills development programs delivered by the Superclusters, all of which were still ongoing/in-progress. While tangible and clear results appear limited to date, the projects show promise. For example, the Digital Supercluster has Capacity Building Projects (e.g., the Canadian Tech Talent Accelerator and Athena Pathways), which have led to 6,500 learning and development placements as of 2020-21. An example from the NGen Supercluster is the Amp-Up program, which subsidizes the cost of training across Canada for member companies (it has 17 education and training partners and has supported 156 employees as of 2020-21). Scale AI's Workforce Development Program was only partially deployed, but had approved 158 training programs for which it would subsidize 50% of registration fees and signed agreements with organizations to train 9,867 individuals by 2023.

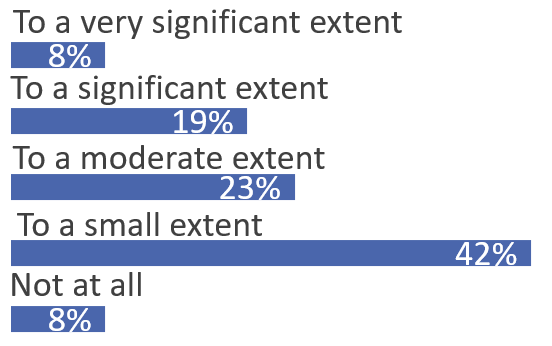

Participation in project activities contributed to employee upskilling.

There was limited data on upskilling in the Supercluster annual reports or Project Activity Reports. While it was not an explicit objective for all ISI projects, almost about half of the survey respondents said that the projects led to increased training or upskilling for employees (50%), including underrepresented groups (56%). Interviewees also agreed that the projects led to the development of employee skills, including for underrepresented groups. Case studies found that organizations participating in projects provided training to employees related to project activities as well as on-the-job learning, as the projects often involved developing new technological capacities to solve project-specific challenges. Training and transference of skills and knowledge also occurred amongst project partners, such as training and guidance to enable the use of a partners' technology or installation of their equipment.

Figure 6: Increased training or upskilling for employees on ISI projects

The source for this table is the 2020 ISI survey of project consortium participants.

Figure 7: Increased training or upskilling for underrepresented groups on ISI projects

The source for this table is the 2020 ISI survey of project consortium participants.

By increasing the number of professionals and HQPs in the ecosystem, the jobs created as a result of ISI projects support ecosystem development.

Interviewees and cases studies found that Supercluster activities led to the attraction and employment of professionals and HQPs, however, the full extent of job creation towards the target could not be validated by program data as many projects are still in progress. At the outset of the initiative, an initial target of 50,000 direct, indirect and induced jobs created/anticipated by March 31, 2028 as a result of Supercluster activities was set based on economic modelling developed by the Conference Board of Canada. ISED's intent is to measure the program's progress against this target through economic analysis conducted by an external agency, starting in 2022, and this work is on track.Footnote 19 The document review could not validate the total number of jobs created or maintained to date, as data was not reported consistently. It was often not specified in the Supercluster annual reports whether the jobs reported were direct, indirect, or expected. Project Activity Reports (PAR), prepared at project opening, identified the number of direct jobs expected to be created or maintained, not created to date. Data collected directly through the PARs estimate that as of August 2021, projects launched to date were expected to create or maintain approximately 11,500 direct jobs over the first five years of the program.Footnote 20 The case studies and interviews provided anecdotal examples demonstrating that the projects led to the creation of jobs. Interviews indicated that not enough time has passed to fully measure the program's success in terms of its potential job creation impacts.

Figure 8: Project Activity Report Estimates for the Number of Direct Jobs Expected to be Created or Maintained as of August 2021

According to interviews and case studies, most jobs were technical positions that employed HQPs with advanced degrees, particularly in STEM.

The survey found that 69% of jobs created from ISI projects were for HQP. Survey respondents (consisting of 27 organizations) reported 252 jobs created relative to the companies' total employment of almost 50,000 employees (0.5%). Consortium partner interviews noted that many newly created jobs were for underrepresented groups and that the Superclusters helped attract some of these underrepresented groups—notably Indigenous workers—through ecosystem projects. The Ocean Supercluster's (OSC) Ocean Allies project provides companies with tools and best practices around diversity, which is used to attract professionals of different demographics. The OSC also created an Indigenous Career Pivot Project help mid-career Indigenous peoples find positions within OSC businesses and provide on-the-job training.

Recommendation 2: To enhance measurement of aggregate program outcomes for the ISI program, ISED Innovation Canada should continue improving the consistency in how data is collected and submitted by the Superclusters. Collecting structured data, in areas such as jobs, training and skills development, would strengthen the quality of metrics used to assess progress against expected outcomes and enhance future modelling and assessments on the long term impacts of the program.

Finding 8: ISI projects are helping participants to develop or access innovative technologies; introduce new products, processes or services; increase revenue, profits and efficiency; and decrease costs. While most projects had expected commercialization benefits, more time is needed for commercialization objectives to be fully realized due to the longer-term nature of these outcomes.

ISI is supporting the advancement of project participants' technology development and commercialization activities.

According to the survey, 85% of respondents with a completed project (27 projects) said that the Supercluster/project provided their organization with support to access or develop innovative or disruptive technologies. In terms of the technology readiness stage of projects, it was noted that products had been proven through deployment in an operational setting (26% of respondents) or commercialization activities were underway (44% of respondents). Project Activity Reports indicate that the majority of projects (73%) had commercialization benefits that were expected to be realized from the projects. This aligns with the survey which found that 70% of respondents (19 out of 27) had introduced new or improved products, processes, or services to the market as a result of their participation in a Supercluster project. In total, these survey respondents reported 46 new or improved products, services or processes, which generated a total of $14 million in annual sales revenue. A few survey respondents (5 out of 27) also indicated that they had acquired new global markets as a result of the project.

However, interviews, case studies, and the document review found that an insufficient amount of time had passed to be able to identify the full extent to which the ISI has led to the development and commercialization of new or improved products, processes or services. Not every project has fully commercialized, and commercialization is on a continuum that includes prototypes and pilots. This points to the longer-term nature of the program – innovation impacts take time, often beyond the timeframe that the projects have been placed under.

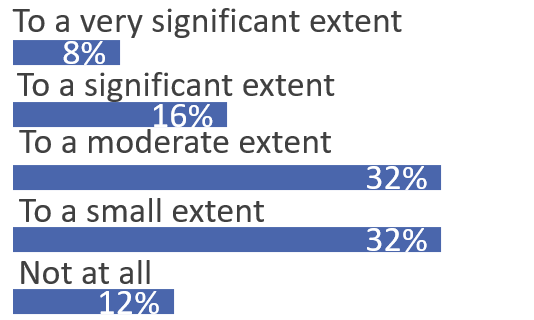

As a result of participation in a project, 38% of survey respondents reported a decrease in costs, 56% an increase in profits, 77% an increase in efficiency, and 79% an increase in revenue.

Figure 9: Survey respondents' reported outcomes resulting from participation in a Supercluster project

Finding 9: ISI projects are helping participants to advance their technologies to the commercialization stage by providing them with critical resources and connections to other organizations. While many projects are still ongoing, examples of product development, process improvements, and commercialization were provided by project participants.

Projects facilitated participants' progression to commercialization stage.

Interviews showed that Supercluster projects are instrumental in getting to the commercialization stage in terms of being able to hire staff; acquire equipment; leverage expertise, intellectual property (IP), and technology of partners; and collaborate and connect with potential customers. For example, as a result of participation in ISI projects: a food processing company said the project allowed them to create an R&D department; a cleantech company was able to get equipment to build a demonstration plant; and an energy company was able to hire a variety of expert personnel.

While many examples related to expected outcomes, as it was too early for commercialization to have occurred, some interviews identified products and processes that had been developed or commercialized. For example, a genetics company launched three new products in three different markets. In terms of improved business processes, one business association said their project enabled them to triple productivity by implementing virtual delivery of its programming. Several manufacturers operating in diverse areas such as steel, pulp and paper, food processing, and additive manufacturing also said that their projects increased the efficiency of processes. Case studies also identified instances of commercialization. For example, a clean agriculture technology company reported that it shifted its business direction into entirely new product lines. Another consortium partner indicated that innovative processes developed for steel production could be applied to the company's other facilities and to other sectors.

Case studies also noted that the projects helped to attract private sector investors and potential customers and end-users. For example, a digital technology company involved in a Scale AI project noted that participation enabled them to expand their customer base to Canada, where they previously did not have a presence.

Case Study Highlights

Digital Transformation of Secondary Metallurgy Facility at ArcelorMittal Dofasco (NGen Supercluster): Participants found that the project allowed them to move from proof-of-concept to commercialization, with partners noting opportunities to apply the project's innovations to other operations, facilities, and sectors.

Precision Agriculture to Improve Crop Health (Digital Supercluster): The project enabled the lead firm to shift its business into new areas and supported increased private sector investment. The other consortium partners said the project helped establish new business opportunities with post-secondary, private sector, and government end-users of their products.

Finding 10: The ISI supports the development, protection, and sharing of IP. The majority of IP created to date was via trade secrets. Early on in the implementation of the Superclusters, there were concerns among members over the sharing of IP. However, over time, the terms developed in IP agreements provided clarity to participants. There has also been increased awareness and gaps in knowledge addressed among participants in the creation, management, and sharing of IP.

The ISI aims to support development, protection, and sharing of IP to help business growth and commercialization.

According to interviews, the idea of collaborative IP is new—most companies want to protect IP for themselves. As a result, the development of the IP agreements and negotiations with project participants was one of the more challenging aspects of the Superclusters. Small firms tended to object more to sharing IP, as it often represents a larger share of their organizational value. Over time, the IP agreements helped address these concerns by providing flexibility and transparency in the use and sharing of IP. The sharing requirements are specific to each project, although there is a base level of sharing via a project IP registry that identifies foreground IP, which is IP that is created from the project.

A lot of time was spent upfront developing a governance model for project IP in terms of ownership, development, use and monetization.

Participants bring background IP, which is IP created prior to the project, that is then used to create new foreground IP. As such, there are mechanisms in the IP agreements that require companies to value their background IP and determine who owns it and how it will be shared when new IP is created. There is also an IP manager in each Supercluster that educates firms on IP protection and ensures that negotiations between parties protects background IP while allowing foreground IP to be shared fairly. As a result of these processes, interviews found increased awareness and openness among participants regarding creating, managing and sharing/licensing IP. For example, an interview noted that for Scale AI, the IP agreements helped SMEs to think more strategically about their IP and better understand how to get value out of it. The Superclusters also offer advice on IP strategies, as well as offering workshops, resources, and tools, especially for SMEs that are less knowledgeable. It was said that this has been helpful in addressing gaps in SME knowledge regarding the protection and exploitation of IP.

Case Study Highlights

Digital Transformation of Secondary Metallurgy Facility at ArcelorMittal Dofasco (NGen Supercluster): It was said that in other jurisdictions such as Europe, IP developed in similar types of consortium projects is automatically owned by all partners, which is a disincentive to engage in collaborative projects. In contrast, the NGen IP agreement clarified the background IP and how foreground IP would be managed and owned for the project, providing assurance that IP would be protected.

ISI contributed to the creation of IP assets among project participants.

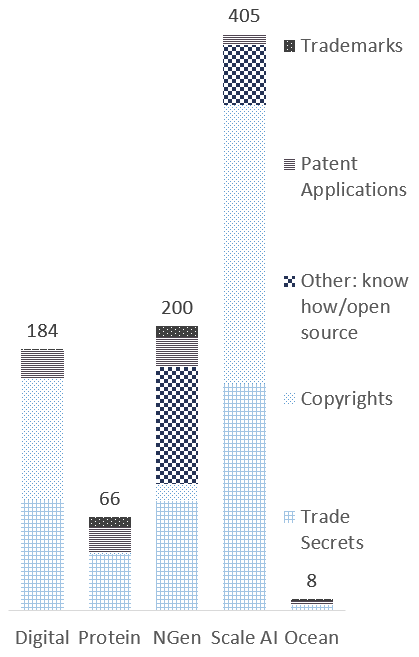

Interviews, including with consortium partners, identified instances of IP creation protected by IP rights, including copyright, trade secrets, and patent applications (e.g., augmented reality for predictive maintenance, modelling of COVID-19 variants, digital platform for PPE procurement), although many of the examples of IP cited by interviews were expected to be created in the future. According to the survey, for completed projects almost half of the respondents (46%) created IP as a result of participation in a project. Relative to trade secrets, interviews found that there were fewer instances in which patents or copyrights were created. This conforms with program data, which found that the majority of IP created so far for the projects was from trade secrets (358), with fewer IP rights generated in the form of trademarks (17), patent applications (70), or copyrights (294). As well, 124 IP rights were generated in other categories (e.g., know how, open source, etc.).

Figure 10: A total of 863 IP rights were generated over 114 reported projects as of September 2021

ISI contributed to the sharing of IP assets among project participants.

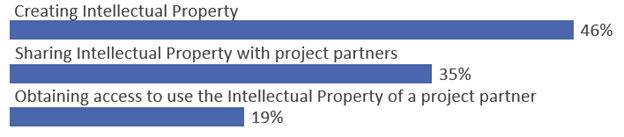

Case studies, interviews and the survey found instances in which IP was shared among participants, including through royalty free licensing agreements. For one case study it was said that IP from one partner was used in the project to support the development of another partner's IP. Another case study established commercial licenses for its technology, as well as providing free, open-source materials to other businesses. The survey found that respondents whose projects were completed (28 out of 176 respondents) had the following outcomes (see Figure 11):

Figure 11: Innovation-related outcomes reported by survey respondents whose projects were completed

The source for this table is the 2020 ISI survey of project consortium participants.

Findings: Efficiency

Finding 11: Through ISI's unique industry-led approach, cross-sectoral collaboration model, and administrative support and flexibility, the delivery model evolved and adapted in response to the shifts in members' needs and ecosystem priorities. As a result of this flexible and responsive approach, stakeholders found that the delivery model was effective and efficient at responding to the emerging complexities and priorities in the innovation landscape and policy pressures such as the pandemic response.

Due to the supercluster's unique delivery model, a longer period of time was required for the Superclusters to become fully operational.

Although the ISI was launched in May 2017, it was not until February 2018 that the five Superclusters were selected. During this period, the ISI received forty-two eligible Letters of Intent from industry-led consortia, nine of whom were invited to submit full applications. After a series of comprehensive assessments (e.g., economic analysis, expert review, etc.) five applicants were chosen based on high potential areas of growth and existing networks and capacity. The initiative's first year of being fully operational was in 2019, albeit in a piloting stage; stakeholders noted that the program's uniqueness and lack of precedents left the Superclusters on the foundation-building phase from 2019 to 2020.

Members saw a gradual evolution in the ISI's delivery model as it underwent several adjustments over the years, and actively contributed to the program's foundation-building phase.

Interviews and case studies spoke to the communication challenges around the members' initial misconception of the ISI purely as a funding agency. The Superclusters' project approvals were slow overall in the beginning, and were hit with further delays as the focus shifted towards COVID-19 project streams and/or pandemic-related adaptation efforts. In the end, interviews and case studies pointed to the Superclusters as being able to gain momentum as they became more experienced at managing projects and the ecosystem, and successfully set clear expectations for members. Some pointed to the role that members played in shaping the delivery model by providing feedback to Superclusters on the operations and management of projects, speaking to the initiative's unique industry-led approach.

Stakeholders identified the ISI delivery model's emphasis on cross-sectoral collaboration, administrative support and flexibility, and its industry-led approach as being an effective and efficient model for responding to gaps in innovation ecosystems.

Cross-sectoral collaboration: Once the delivery model was fully implemented, stakeholders felt that the ISI was operating and functioning how it was designed and intended to be. The ISI is the only model to date that has effectively achieved large-scale coalescence between various sectors, with structured and substantive outcomes. The collaboration component was identified as key to the success of the program, as it leads to the participation of more companies and better results from more perspectives in projects. The collaboration piece also bridged gaps between various sectors in an unprecedented way, especially in terms of SME inclusion.

Administrative support and flexibility: Interviews indicated that most project consortium participants had positive things to say about the delivery model, with the application process being straightforward and quick compared to other funding programs. The ISI differs from other innovation programs in that it goes beyond funding and the Supercluster staff provides support and helps identify gaps. For example, there is an IP manager in each Supercluster to educate firms on IP protection and facilitate the IP agreement negotiations between parties. Board members expressed that the ability to leverage other government funding was an added benefit to the 1:1 industry match funding. They also felt that the oversight and approval processes showed good stewardship of taxpayer funds while not being onerous. Also, allowing funding to be accessible to companies of all sizes has helped SMEs overcome the high barriers to entry.

Agile industry-led approach: ISED officials pointed to the delivery model's agility and industry-led approach as a key strength in allowing the Superclusters to effectively respond to the identified and emerging industry priorities and mobilize during the pandemic. The industry's active involvement in program decision-making and project selection ensures commercially relevant projects. Since government programming may at times be out of sync with industry, ISED officials felt that an arms-length role would achieve better synchronicity with industry, while making room for accountability and alignment with government priorities and opportunities for mutual reinforcement.

The ISI and ecosystem members co-developed a strong foundation for a delivery model that responds best to industry needs and priorities.

Most members lauded the industry-led approach as effective and responsive to their needs and priorities. Each Supercluster determines their own funding allocations and internal operations based on their sectoral needs and interests, such as project calls for approvals and membership fee allocations. According to interviews, early on, the strong industry voice in the ISI played a role in switching to a contribution model with a transparent sharing ratio from the onset so that members could feel more comfortable investing money towards project funding rather than just a general fund. Also, an IP manager was deployed to help mitigate the disagreements and misunderstandings in IP sharing requirements and balance out the playing field for smaller firms. To help members adapt to the pandemic, the Superclusters allowed those with projects to take advantage of the program's provisions for advances. Some Superclusters also provided fee deferrals and employee wage funds to help members to continue participating in projects without having to rely on their existing cash flow.

The Superclusters' pivot to the pandemic response was a testament to the program's flexibility and the agility of the industry-led approach.

With the flexibility of the program, Scale AI, NGen, and Digital Tech were also able to prove themselves as key government partners by pivoting towards developing distinct COVID-19 programming streams. As of September 2021, approximately $215.9 million went to announced COVID-19 projects, of which $81.3 million was from partner contributions and $134.6 million was from the Superclusters. The 2021 federal budget provided $60 million to top up the ISI and ensure the continued support of projects over a period of two years: $36 million for 2021-22, and $24 million for 2022-23. Although the pandemic did create delays and disruptions, the Superclusters' participation in the pandemic response generated new business models and gains for members and the ecosystem overall. For instance, an NGen funded project, led by a firm focused on face shields, was able to expand their new business line into a manufacturing cluster in rural Ontario that did not exist previously and would provide a new source of employment over the medium term.

Finding 12: Each Supercluster is on track to meet the 1:1 industry matching funds ratio required over the five-year timeframe. Private sector investment increased overall, even during the pandemic.

Approximately $957.0M has been leveraged from industry partners (i.e., industry matching funds) for approved Regular Stream projects across the five Superclusters as of July 31, 2021.Footnote 21 The Supercluster Contribution Agreements require that every dollar of ISI funding received and spent be matched by industry contributions – each Supercluster must be at least evenly matched by the end of the five-year period. ISI funding includes administration and operating costs as well as project costs, meaning that industry contributes funds towards projects and the day-to-day operations of the Supercluster.

Each Supercluster has the flexibility to take different approaches to industry matching meaning they can determine a minimum amount of industry support (from 0-100%) for any project. By requiring more or less industry support, the Superclusters can choose how and where they allocate ISI funds. As of July 31, 2021, each Supercluster has exceeded the 1:1 ratio.

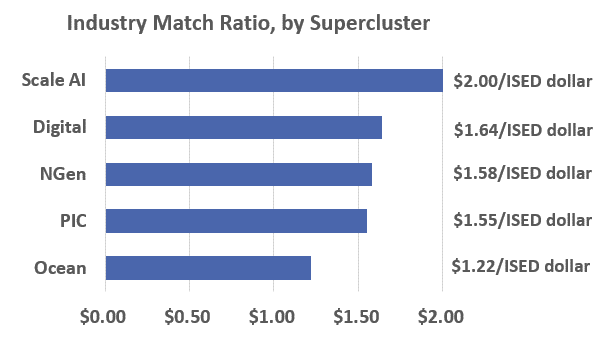

Notably, Scale AI was able to generate $2.00 of industry investment for every ISED dollar and leveraged $53 million from the Government of Quebec – a level of investment that other Superclusters did not achieve with their provincial counterparts. This additional funding enabled Scale AI to increase its coverage of program costs from 25% to 50% in Quebec, which helped safeguard key industry jobs through the pandemic.

Most interviewees agreed that the Superclusters' projects overall have had no issues in securing financial support from other players. For Regular Stream projects, data shows that the industry match ratio is approximately $1.55 for every ISED dollar, and COVID-19 projects that were exempted from the usual IP and industry match requirements were still able to attract industry funding. Although there was an economic slowdown during the pandemic, interviewees observed that industry investment in the program still increased overall even with the pandemic's period of high uncertainty.

Figure 12: Industry Matching Funds to ISED Contribution, by SuperclusterFootnote 22

The source for this table is approved Regular Stream ISI projects as of July 2021

Figure 13: Industry Match Ratio, By Supercluster

The source for this table is approved Regular Stream ISI projects as of July 2021

Finding 13: The use of available operating and administrative funds varies by Supercluster and correlates with the proportion of project funding each Supercluster has used, suggesting that the Digital Technology and NGen Superclusters are furthest along in operationalizing their activities. All Superclusters have remained within spending limits for operating and administrative funds.

The Superclusters have varied significantly in their use of available operating and administrative funds to date.

Each Supercluster is allotted a proportion of ISED's funding to cover operating and administration costs (O&A). For each Supercluster, ISED funding for eligible O&A costs may cover up to 11.25% of ISED's total contribution. The evaluation found that the proportion of available O&A funds used by each Supercluster as of March 2021 varied widely between 20% (SCALE AI) and 64% (Digital Technology). While the SCALE AI and Ocean Superclusters have used the lowest proportion of available funds to date, the Digital Technology and NGen Superclusters have spent the highest. Despite this, all Superclusters have remained within their O&A spending limits.

Figure 14: ISI O&A Funding Used

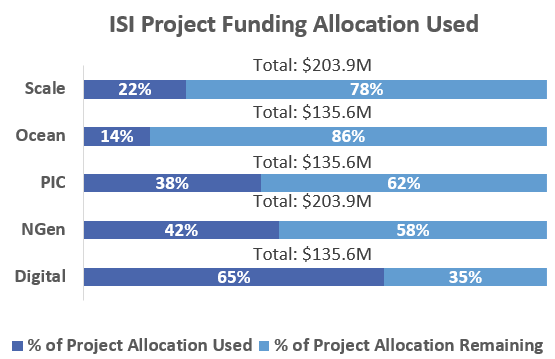

Superclusters that have used a higher proportion of available operating and administrative funds, have also used a higher proportion of available project funds, suggesting that some entities are further along in implementing their activities than others.

Superclusters that have spent a higher proportion of their available O&A funding have also used a greater proportion of available ISI funding for projects, suggesting that some entities are at a more mature stage than their counterparts and are selecting and implementing projects more efficiently than others. For example, the two Superclusters with the lowest proportion of O&A funding used (Scale AI and Ocean) have also used only 22.1% and 14.3% of available project funding. In contrast, the Digital Technology and NGen Superclusters have used 64.8% and 42.2% of their available project funding to date, suggesting these entities are facing less challenges in operationalizing their activities.

Figure 15: ISI Project Funding Allocation Used

Finding 14: Although the Superclusters committed to equity, diversity, and inclusion (EDI) in their practices, the robustness of existing policies and programs to promote EDI within each of the Superclusters varies due to a lack of formal requirements that go beyond gender parity.

The Superclusters made various EDI commitments and undertake unique projects to address inequities in their ecosystems.

Organizational EDI commitments: ISED commissioned a report by the Diversity Institute at Toronto Metropolitan University (formerly Ryerson University) to conduct a baseline review of the Superclusters' equity outcomes for gender and racialized people based on publicly available data on Boards of Directors, staff and membership. Each Supercluster's Contribution Agreement stipulates that they promote and practice values related to Equity, Diversity and Inclusion (EDI) that align with ISED. As specified in the agreements, the Superclusters must ensure that Board composition includes representatives of its ecosystem and significant representation of Canada's multicultural diversity, including visible minorities and Indigenous peoples. Any Board executive committee must be comprised of no less than 50% women. Beyond these formal commitments, every Supercluster but Scale AI has pledged to the 50-30 Challenge, which encourages boards to go beyond gender parity and have 30% representation from underrepresented groups.

EDI promotion in program activities: All Superclusters have also undertaken projects that seek to address inequities relevant to their platform or sector with a built-in GBA+ lens for improving access for underrepresented groups. Some highlights include:

- The Digital Supercluster's Canadian Tech Talent Accelerator project will provide in-demand digital skills to young Canadians underrepresented in the economy. 80% of graduates have secured IT related employment or higher education placements within 12 months of the program.

- NGen provided in-kind support for Women in Science and Engineering university programs and other Women in Manufacturing and Women in Technology initiatives, and developed strategic partnerships with the Black North Initiative and the Martin Family Foundation to integrate advanced manufacturing into entrepreneurship courses for Black and Indigenous youth.