Final Report

August 31, 2009

Tabled and approved at Departmental Evaluation Committee on October 30, 2009

Table of Contents

- Executive Summary

- 1.0 Introduction

- 2.0 Evaluation study

- Evaluation Findings

- 3.0 Relevance

- 4.0 Success

- 5.0 Cost Effectiveness

- 6.0 Program Delivery

- 7.0 Other Observations

- 8.0 Recommendations

- Bibliography

- Management Response and Action Plan

Executive Summary

This report presents the results of the 2009 evaluation of the Canada Small Business Financing (CSBF) Program.

In accordance with the Canada Small Business Financing Act, a Comprehensive Review of the provisions and operation of the Act must be tabled in Parliament by March 31, 2010 for the period from April 1, 2004 to March 31, 2009. This evaluation study will contribute to the Comprehensive Review requirements.

Purpose of the Program

The Canada Small Business Financing Program is a loan loss sharing program which facilitates loans to small businesses who might not otherwise qualify for a conventional loan. Term loans are eligible under the CSBF Program for the specific purposes of financing the purchase of land, buildings, or equipment, or, to improve buildings (including leasehold improvements) and equipment.

In partnership with financial institutions who offer the program on behalf of the federal government, the CSBF Program shares the burden of risk with lenders by sharing in losses that may be experienced as a result of extending financing to SMEs who might not otherwise qualify for a conventional loan.

Industry Canada administers the CSBF Program, registers loans, collects fees and pays lenders eligible portions of losses on default loans, but is not involved in assessing individual loan applications. It is lender's responsibility to approve and administer loans, as well as disburse loans.

In addition to its primary goal of facilitating financing for small businesses, the CSBF Program has two official objectives:

- Incrementality: the program's effectiveness in extending financing that would otherwise have been: unavailable to small businesses; available but for smaller amounts; or, available only under less attractive conditions such as higher fees, higher interest rates, more collateral required, less timely, etc.; and

- Cost recovery: means that the CSBF Program's revenues will offset claims on defaulted loans.

Evaluation Approach

The evaluation has employed a synthesis approach of qualitative and quantitative evidence. Many pieces of research, which form the basis of this evaluation, were conducted by independent third parties using acceptable social science research methods.

The evaluation study was managed by the Audit and Evaluation Branch of Industry Canada. The evaluation was conducted by KPMG, and the team was led by the Associate Partner of Advisory Services, who had been involved in the 2004 CSBF Program evaluation. In addition, one AEB resource participated in the conduct of the interviews with lenders. The evaluation was done in consultation with a Steering Committee established for the purpose of the evaluation. (See Annex A for a list of Steering Committee members).

The following evaluation methodologies were employed in this evaluation:

- Analysis of available data and documents

- Stakeholder Interviews

- Risk Assessment Workshop

- Cost Benefit Analysis

Findings and Recommendations

Findings

Relevance

Industry Canada's delivery of the CSBF Program is consistent with its mandate and Government directions.

There is limited evidence to support a widespread belief that there is an SME financing gap. There is no evidence to indicate that SMEs have more difficulty obtaining financing than larger firms simply because they are SMEs—i.e., SMEs are not disadvantaged relative to larger firms.

However, firms that are higher risk with regard to their likely ability to repay loans do have more difficulty obtaining financing than lower risk firms, and many SMEs, such as start-ups, fall into this high risk category. The main factors that influence lenders to offer the CSBF Program to potential borrowers are lack of collateral and small size of firm. Therefore a gap appears to exist for very young businesses with limited experience, lack of collateral and which have a high credit risk score. As a result, the CSBF Program fills a marketplace financing gap for these types of firms.

There are no other federal programs that duplicate the CSBF Program for SMEs. The Business Development Bank of Canada, a federal Crown corporation, and a lending organization, provides SMEs with financing through "Term Loans" and," Subordinate Financing" which are similar to the term loans guaranteed under the CSBF Program, and thus there is some overlap between the two.

There are substitute programs for specific targeted SME populations such as rural entrepreneurs, and/or for specific reasons, such as commercialization. Federally, the closest substitute program is the Community Futures (CF) Program, funded by the Regional Development Agencies (RDA) and Industry Canada, but delivered through community not-for-profit organizations. The CF program is targeted towards rural SMEs, which represent 33% of the portfolio of borrowers under the CSBF Program.

All provinces have various types of assistance programs targeted towards SMEs. Seven provinces offer a loan guarantee program to SMEs, similar to that of the CSBF Program.

In addition to government programs, there has been greater availability and accessibility to various credit options through conventional lenders over the past ten years.

Success

Since 2004, the levels of incrementality achieved by the CSBF Program have been maintained, and have steadily increased, from a rate of approximately 75% to a rate of 80–85% in 2007.

In several key areas, CSBFP borrowers outperform comparable SMEs who have not received a CSBFP loan. SMEs who are CSBFP borrowers have consistently higher levels of business survival compared to non-CSBFP borrowers. They are able to increase their business investments (total assets) at a faster pace when compared to non-CSBFP borrowers. Their companies also experience higher levels of sales growth.

CSBFP borrowers experience greater employment growth compared to non-CSBFP borrowers, and their employment levels increase at a faster pace. There does not appear to be an impact on profits as a result of obtaining a CSBFP loan.

In spite of the benefits experienced by businesses that receive a CSBFP loan, there has been a steady decrease in the number of loans made over the life of the CSBF Program. A drop from 17,741 loans in fiscal year 1999–2000, down to 9,015 loans during fiscal year 2007–2008, represents a decrease of 49.2%. The reasons for this drop are not well defined but are partially as a result of lenders' experiences and some dissatisfaction with the program. Lenders perceive the program as not profitable, and some lenders have decided not to offer the program after negative experiences with CSBFP loan claims. Borrowers themselves have a low level of awareness of the CSBF Program and rarely request the program.

The factors that pose the greatest risk to the CSBF Program's ability to achieve its objectives and intended impacts are related to lender perceptions and behaviour:

- the risk that the program is not perceived to be an attractive vehicle by the lenders due to program design features (e.g., high administrative requirements)

- the risk that the internal policies and actions of individual lenders may impair the program's ability to achieve its goals.

Cost Effectiveness

The CSBF Program, as it is currently structured, is not cost recoverable when administration and registration fees are the only revenues used in the calculation. However, it can be considered cost-recoverable over the study period when incremental federal income taxes and GST generated by CSBFP borrowers are considered.

The CSBF Program generates significant net benefits for Canada as a result of the impacts of incremental CSBFP loans on the economy. The estimated benefits of the program far outweigh the program costs. Total net benefits of the program, including both direct and indirect benefits are estimated to be $4,869.7 million over a nine year period of study between 1999–2000 and 2007–2008.

Program Delivery

Lenders have identified a heavy administrative burden, which includes a paper-based system, and difficulties with the claim process, as major obstacles to their use of the CSBF Program. These factors have also been identified as the biggest risk to the program. The cap on fees has also caused lenders to reconsider using the CSBF Program, as it is not profitable to them.

Overall, there is very limited knowledge of the program by CSBFP borrowers and non-borrowers.

Marketing efforts by the program have been limited, and there has been reluctance on the part of head offices of lending institutions to allow the program to approach individual branches. However, lenders interviewed felt that the level of awareness of the program by lending officers is average to good. As program staff are not able to market directly to loan officers, this may contribute to the decreasing number of loans.

Recommendations

As a result of the findings of this evaluation, there are opportunities for improvement in areas of Program Design, Delivery and Measuring Success.

Program Design and Delivery

Since the current program parameters were put in place in 1999, the number of loans under the program has fallen by 49%, and the total value of loans within the program portfolio has also decreased. Both lenders and program staff perceive that the largest risk to the program is that it is increasingly perceived to be an unattractive vehicle by the lenders due to program design features.

Recommendations:

- 1. Given that both borrowers' representatives and lenders during the interviews supported expanding the asset classes; consider the possibility of broadening the range of assets against which a CSBFP loan can be made, thereby increasing the attractiveness of the program to both lenders and borrowers.

- 2. Measures should be put in place that would make the program more appealing for the lenders to offer. These measures could include: providing increased flexibility regarding administration fees and interest rates; lowering the administrative burden for lenders, by assessing the feasibility of establishing an automated system for registration and claims in order streamline those processes; and considering whether a risk-based approach might be applicable to ensure the accuracy of claims. These measures should be balanced and should consider the impact on the borrower.

- 3. Increase communication with lenders and undertake more pro-active marketing of the program to the lending community. During the interviews, lenders placed particular emphasis on obtaining information about the program itself but more importantly about the types of expenses that are eligible for a claim. Providing lenders with an understanding of eligible claims would reduce their frustration with the claims process and may increase utilization of the program.

Measuring Success

The CSBF Program has two objectives – incrementality and cost-recovery. These objectives have an inverse impact on each other. The higher the incrementality of the program, the riskier the portfolio becomes, which leads to a higher incidence of claims. This decreases the ability of the program to achieve a high percentage of cost recovery. Within this context, the program is meeting these objectives as well as could be expected, and significant economic benefits are being generated to the Canadian economy.

The program is relevant; an incrementality rate of between 75–85% indicates that the Program is providing loan guarantees to SMEs who would be unlikely to receive a conventional loan. The Program appears to be successful as the CSBFP borrowers have been able to achieve a higher level of economic performance than a comparator group of non-CSBFP borrowers with similar characteristics. Because the program has a relatively high level of incrementality, it also faces high levels of risk.

Since its inception, the CSBF Program has not been cost recoverable. The cost recovery rate has been forecasted at 67.7% for the first cohort (1999–2004) and 58.9% for the second cohort (2004–2009).

Between the high level of incrementality that the program has attained and the fact that the loan portfolio is riskier since 2004, it is anticipated that the gap between claims and fee revenues will continue to exist and most likely expand.

Recommendations:

- 4. Review the program's cost recovery objective, given that the program has not been fully cost recoverable. In reviewing this target, consideration must be given to the balance between potential burden on borrowers, profitability for lenders and government accountability.

- 5. When communicating the results of the CSBF Program in the Annual Reports, care should be taken in presenting the job creation numbers estimated by borrowers at the time of the loan application, given the discrepancies between those and actual realizations.

List of Acronyms and Definitions

| BDC | Business Development Bank of Canada |

| CFIB | Canadian Federation of Independent Business |

| CSBFA | Canada Small Business Financing Act |

| CSBF Program | Canada Small Business Financing Program (used when referencing the Program itself) |

| CSBFP | Canada Small Business Financing Program (used when referencing various elements of the Program, such as loans or borrowers) |

| FDI | Financing Data Initiative |

| FTE | Full-time equivalent (usually used in relation to jobs) |

| OAG | Office of the Auditor General of Canada |

| SBTB | Small Business and Tourism Branch (of Industry Canada) |

| SBL program | Small Business Loans program |

| SMEs | Small and medium-sized enterprises |

| SBFD | Small Business Financing Directorate (of Industry Canada, responsible for the administration of the CSBF Program) |

| RMAF | Results-based management and accountability framework |

Definitions

Small businesses: Statistics Canada defines small businesses as enterprises having annual revenues between $30,000 and $5,000,000. The CSBF Program is restricted to small businesses with less than $5 million in gross annual revenues. Official documents produced by the CSBF Program use the terms small business and SME interchangeably when referring to borrowers under their program.

SME: Small and medium sized enterprises. Statistics Canada defines SME as enterprises with less than 250 employees and less than $50 million in total revenue.

SME-FDI Survey: Statistics Canada surveys enterprises with fewer than 500 employees and less than $50 million in revenues.

Industrial Sector: Statistics Canada classifies industrial sectors under the North American Industry Classification System (NAICS) Canada, 20071. Under the two digit first level classification, Accommodation and Food Services, is the three digit lower classification entitled Food Services and Drinking Places. Official documents produced by the CSBF Program use the term Food and Beverage Services. Both terms are used in this document depending upon the source referenced, and represent the same sector.

1 http://www.statcan.gc.ca/concepts/industry-industrie-eng.htm (Return to Reference 1)

1.0 Introduction

This report presents the final results of the 2009 evaluation of the Canada Small Business Financing (CSBF) Program. This evaluation is an element of the comprehensive review of the program, which the program is required to table in Parliament, every five years under the Canada Small Business Financing Act.

1.1 Program Description

The Canada Small Business Financing Program facilitates loans to for-profit small and medium enterprises (SMEs). It is a statutory program governed by the Canada Small Business Financing Act (CSBFA), which came into force on April 1, 1999, replacing the Small Business Loans Act (SBLA).

In the context of the CSBF Program, an SME2 is defined as "a for profit small and medium size businesses in Canada with gross revenues or projected revenues of less than $5 million". These businesses can be corporations, sole proprietors, or partnerships, but exclude farming businesses. The Program adopts a more restrictive definition of SMEs than the broader definition used in the Statistics Canada SME-FDI survey which is, enterprises that have fewer than 500 employees and have annual gross revenues of less than $50 million.

The objective of the Canada Small Business Financing Program is to facilitate access to asset-based debt financing that would otherwise have been unavailable to SMEs for the establishment, expansion, modernization and improvement of small and medium-sized enterprises.

The CSBF Program relies on a partnership with private lenders to deliver the program, as it is private lenders who provide the funding directly to borrowers. Industry Canada administers the CSBF Program, registers loans, collects fees and pays lenders eligible portions of losses on default loans, but is not involved in assessing individual loan applications. It is lender's responsibility to approve and administer loans, as well as to disburse loans.

In fiscal year 2007–2008, the CSBF Program helped SMEs obtain over 9,000 loans with a value of over $1 billion. Since 1999, almost $10 billion in loans has been made3.

The program has two specific objectives:

- Incrementality: the program's effectiveness in extending financing that would otherwise have been unavailable to small and medium-sized businesses, available but for smaller amounts or, available only under less attractive conditions such as higher fees, higher interest rates, more collateral required, less timely, etc.…

- Cost recovery: means that the CSBF Program's revenues will offset claims on defaulted loans.4

For the period under review, the main parameters that define the structure of the program are listed in the following table.

| Parameter | Description |

|---|---|

| Eligible businesses | For profit enterprises (except "agricultural industries") with estimated gross annual revenues of $5 million or less. |

| Loss-sharing ratio | 85% government, 15% lender |

| Cap on lender claims | The government's liability to an individual lender is to pay eligible claims on defaulted loans in it account up to a maximum of the aggregate of: 90% of the first $250,000 of loans registered by the lender 50% of the next $250,000 10% of all loans in excess of $500,000. |

| Ministerial Cap on Claims (for each 5 year lending period) | $1.5 billion |

| Eligible purposes | Purchase or improvement of real property and immovables Purchase of leasehold improvements, Improvements to leased property. Purchase or improvement of new or used equipment. |

| Maximum loan amount | $250,000 for equipment, leasehold improvements, and real property. |

| Financing rate | 90% |

| Payment terms | Maximum of 10 years |

| Registration fee | 2% of the total amount loaned under the program (can be financed as part of the loan). |

| Administration fee (annual) | 1.25% of outstanding loan amount (paid quarterly). |

| Maximum rate of interest | Variable rate: maximum chargeable is the lender's prime lending rate plus 3% (which includes the 1.25% administration fee). Fixed rate: The maximum chargeable is the lender's single family residential mortgage rate plus 3% (which includes the 1.25% administration fee). |

1.2 Program History

The Government of Canada started assisting small businesses under the Small Business Loans program, which was launched in 1961. From that time until 1993 the program remained relatively stable and also relatively modest. Only companies with under $250,000 in sales were eligible at the beginning of the program; this increased slowly over the years to $2 million in 1985. The maximum loan size started at $25,000, reached $100,000 in 1980, and remained at that level until 1993. A number of changes were made to the program in 1993 in order to extend its coverage. This was in response to economic difficulties and uncertainty being experienced in Canada at that time and a commitment by the government that it would help small businesses lead the way to recovery.

Several of these changes resulted in increased risk to the government and the likelihood of a larger gap between fees paid to the government (the registration fee only at that time) and the cost of claims paid by the government. These changes included:

- expansion of program eligibility to encompass firms doing up to $5 million of business per year;

- Government coverage of 90% of the cost of claims (up from 85%);

- increase to 100% from 80%–90% of the cost of assets that could be financed, and

- increase in the maximum loan size to $250,000 (up from $100,000).

Not surprisingly, the number of loans skyrocketed, as did the number of loan defaults and claims a few years later.

In 1995 the most significant of these changes were reversed—in particular, the government's guarantee was decreased to 85%, and maximum financing levels returned to 90% of asset value. In addition, the government introduced a cost recovery mandate and began to move toward an increased degree of cost recovery by introducing the annual administration fee of 1.25%. Some additional changes were made in 1999, largely as a result of the comprehensive review of the program undertaken in 1998–99. These were intended to increase the accountability of lenders and strengthen the program's ability to move toward cost recovery. The program was renamed the Canada Small Business Financing program at that time.

Changes to Program Parameters—Budget 2009

The 2009 federal budget changed some of the parameters of the CSBF Program. Three major changes include:

- An increase in the maximum eligible loan amount a small business can access under the Canada Small Business Financing Program for loans made after March 31, 2009. The new limits are $350,000 for equipment and leasehold improvements, and, $500,000 for real property

- An increase in the losses reimbursement limit for institutions with a portfolio of eligible loans above $500,000. The rate has gone up from 10% to 12%.

- In addition to the program modifications, regulatory amendments will reduce the program's associated paperwork burden.

These changes were enacted on April 1st, 2009, after the completion of the lending period being reviewed in this evaluation.

top of page1.3 Current CSBF Program—Loans and Claims

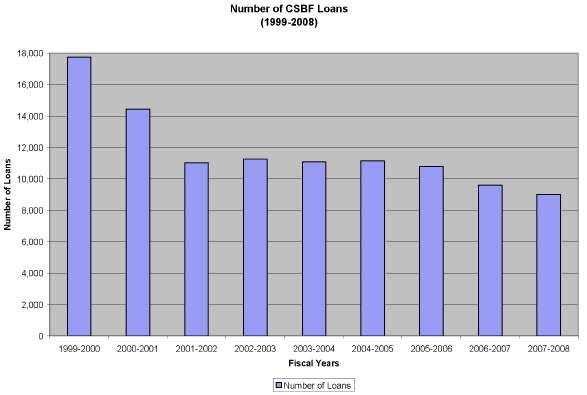

Number of Loans5

Overall, between 1999 and 2008, the number of loans granted has decreased by almost 50%. From a maximum of 17,741 loans in 1999–2000, the number of loans reached its lowest point in 2007–2008 with 9,015 loans, a reduction of almost 50%.

Year over year, the rate of change in the number of loans is negative with the exception of two slightly increases in fiscal years 2002–2003 (2.24%) and, 2004–2005 (0.52%).

The table below presents the evolution in the number of loans during the period 1999–2008.

| Fiscal Year | Number of Loans | Number of Loans—Yearly Change (%) |

|---|---|---|

| 1999–2000 | 17,741 | |

| 2000–2001 | 14,442 | -18.60% |

| 2001–2002 | 11,016 | -23.72% |

| 2002–2003 | 11,263 | 2.24% |

| 2003–2004 | 11,085 | -1.58% |

| 2004–2005 | 11,143 | 0.52% |

| 2005–2006 | 10,790 | -3.17% |

| 2006–2007 | 9,596 | -11.07% |

| 2007–2008 | 9,015 | -6.05% |

| Total | 106,091 |

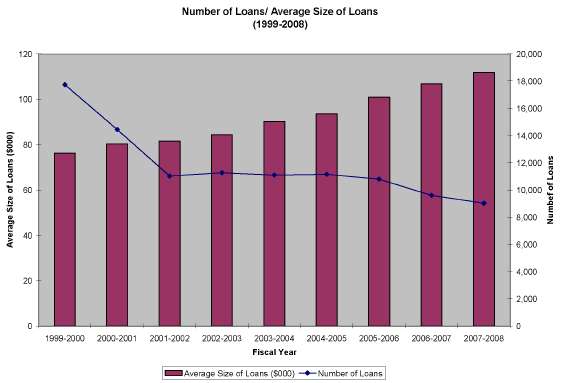

Average Size of Loans6

At the same time as the number of loans decreases, the average loan amount has increased. Between 1999 and 2008, the average size of a loan has moved from $76,200 to $111,700, an increase of 46.6%. Between fiscal year 1999–2000 and 2007–2008, the average size of loans has consistently increased every single year.

The table below presents the evolution of the average size of loans between 1999 and 2008.

| Fiscal Year | Average Size of Loans ($000) | Average Size—Yearly Change (%) |

|---|---|---|

| 1999–2000 | 76.2 | |

| 2000–2001 | 80.3 | 5.38% |

| 2001–2002 | 81.6 | 1.62% |

| 2002–2003 | 84.4 | 3.43% |

| 2003–2004 | 90.2 | 6.87% |

| 2004–2005 | 93.5 | 3.66% |

| 2005–2006 | 100.8 | 7.81% |

| 2006–2007 | 106.8 | 5.95% |

| 2007–2008 | 111.7 | 4.59% |

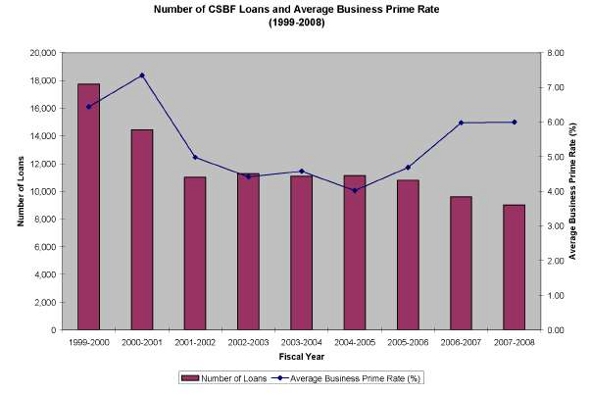

The contradictory trends (number of loans decreasing vs. the average amount of loans increasing) can be seen in the following chart. The time frame covered is between fiscal year 1999–2000 and fiscal year 2007–2008.

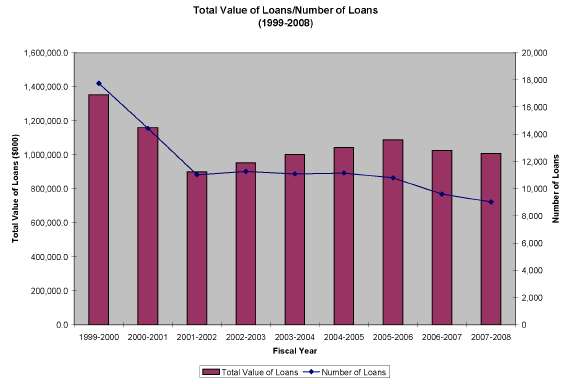

Value of Loans7

Contrary to measures such as the number of loans and the average size of loans, the overall value of loans has not followed a definite trend. The annual total value of loans declined during the fiscal years 2000–2001 (14.3%) and 2001–2002 (22.4%), but, increased steadily between fiscal years 2002–2003 and 2005–2006 (an overall increase of 20.9% between those two fiscal years). In the last two fiscal years, the value of loans has decreased, at a rate of 5.8% for the 2006–2007 fiscal year and, 1.8% for the fiscal year 2007–2008.

The following chart shows the evolution of the total value of loans compared to the number of loans between fiscal years 1999–2000 and 2007–2008.

top of page

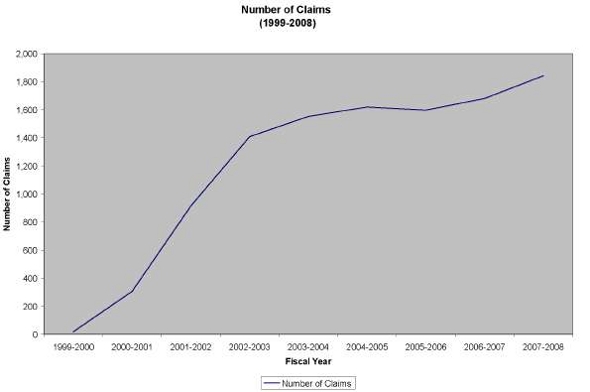

Number of Claims

Despite the reduction in the number of loans, the trend in the number of claims is to the upside. The number of claims has increased year over year. Between 1999 and 2008, the numbers of claims has increased, with the exception of a slight reduction of 1.4% for fiscal year 2005–2006.

| Fiscal Year | Number of Claims Paid | Number of Claims—Yearly Change (%) |

|---|---|---|

| 1999–2000 | 19 | |

| 2000–2001 | 307 | 1515.8% |

| 2001–2002 | 915 | 198.0% |

| 2002–2003 | 1,409 | 54.0% |

| 2003–2004 | 1,553 | 10.2% |

| 2004–2005 | 1,620 | 4.3% |

| 2005–2006 | 1,598 | -1.4% |

| 2006–2007 | 1,681 | 5.2% |

| 2007–2008 | 1,843 | 9.6% |

| Total | 10,945 |

Value of Claims Paid

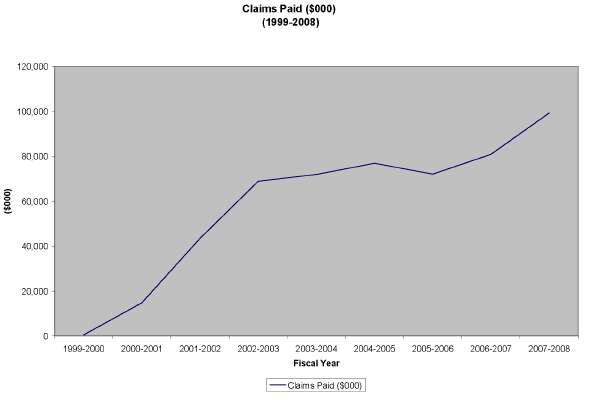

The value of claims paid follows the same trend as the number of claims. The annual total value of claims paid has increased year over year between 1999 and 2008, except for fiscal year 2005–2006, when the value of claims decreased by 6.3% with respect to fiscal year 2004–2005. This dip matches the reduction in the number of claims for fiscal year 2005–2006.

| Fiscal Year | Claims Paid ($000) | Number of Loans—Yearly Change (%) |

|---|---|---|

| 1999–2000 | 494.6 | |

| 2000–2001 | 14,769 | 2886.0% |

| 2001–2002 | 43,466 | 194.3% |

| 2002–2003 | 68,891.60 | 58.5% |

| 2003–2004 | 71,949.10 | 4.4% |

| 2004–2005 | 76,872.60 | 6.8% |

| 2005–2006 | 72,065.50 | -6.3% |

| 2006–2007 | 80,855.90 | 12.2% |

| 2007–2008 | 99,269.20 | 22.8% |

| Total | 528,633.50 |

1.4 Borrower and Loan Demographics

Industrial Sector8

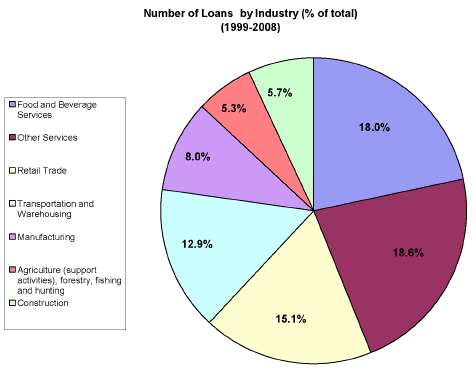

Between 1999 and 2008, the largest number of CSBFP loans (18.6% of the total number of loans) has been granted to SMEs in the "Other Services" sector. Other services includes such services as: repair and maintenance services related to automotive, electronics, commercial, household goods; personal and laundry services related to personal care, funeral services, dry cleaning, pet care services. Following closely in second place at 18%, are SMEs in the "Food and Beverage Services" sector. "Retail Trade" ranks third with 15.1% of the total number of loans.

The chart below presents the share of loans granted for the top seven industrial sectors9.

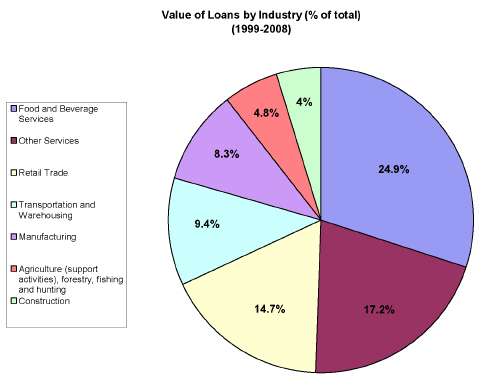

In terms of the industrial sector composition of the CSBFP loan portfolio by value, the "Food and Beverage Services" sector represents the largest amount, 24.9% of the total value of loans granted. SMEs in the "Other Services" sector had the second largest share of the total value of loans, with 17.2%.

The chart below presents the percentage value of the top seven each industrial sectors within the total value of loans in CSBFP portfolio.

The industrial sector with the highest average value of loans is the "Food and Beverage Services" sector, where the average loan is $124,300. The industry with the second highest average loan value is "Manufacturing", where the average value of loan is $93,800. "Retail Trade" and "Other Services" follow, with average loan values of $87,700 and $83,300 respectively10.

The chart below presents the average loan value per industry. Only the industrial sectors with the highest average value of loans have been included.

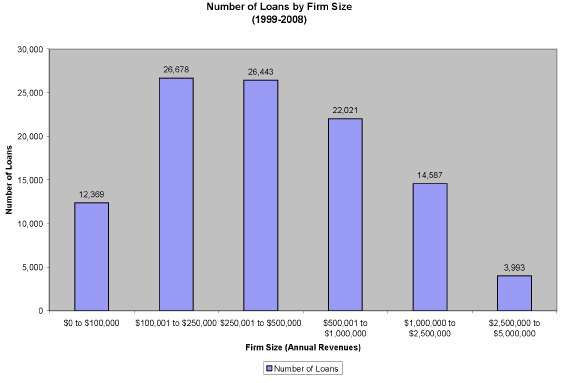

Firm Size

CSBFP borrowers are smaller firms, with less than 20 employees, however the majority of these have between 2 and 4 employees. Over half of the CSBFP borrowers had revenues under $300,000, although one-quarter of these had revenues under $100,000.

The largest group of SMEs receiving financing under the CSBF Program is those with revenues between $100,001 and $250,000, with 25.2% of the loans. Those SMEs in the $250,001 to $500,000 group are the second largest, with 24.9% of the loans. The third largest group receiving loans is that of SMEs with revenues between $500,001 and $1,000,000. The smallest number of loans under the CSBF Program is seen in the SME group with revenues between $2,500,000 and $5,000,000.

The following chart presents the number of loans by borrower firm size11.

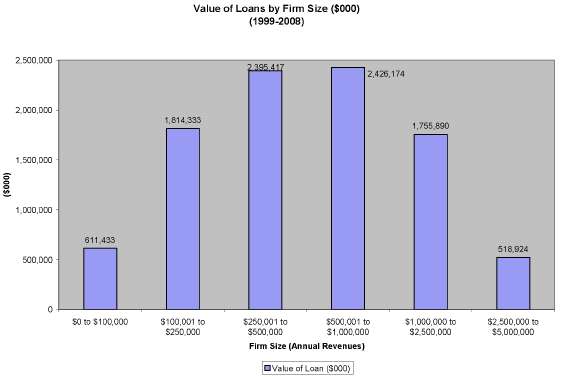

When examining the value of loans by firm size, SMEs with revenues between $500,001 and $1,000,000 have the largest share of the total loan portfolio. SMEs with revenues between $250,001 and $500,000 are a close second.

The SME group that receives the smallest value of loans in the portfolio is those with revenues between $2,500,000 and $5,000,000.

The following chart presents the value of loans by borrower firm size12 13.

top of page

Age of Borrower Firm

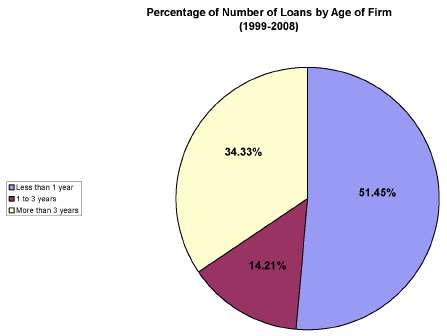

The majority of CSBFP loan recipients are smaller firms, with less than five years old. The majority of these are startups, less than one year old.

In 2004, 51% of CSBFP borrowers were young firms who began selling products or services within the previous 5 years. 36% of CSBFP borrowers were start up companies that entered the market between 2002 and 200414.

Over the 1999–2008 period, the majority of CSBFP loans were granted to firms that are less than one year old (51.5%). Firms that have existed for longer than 3 years receive the second highest share of loans with 34.3%. SMEs aged between 1 to 3 years benefit the least from the CSBF Program, as only 14.2% of them have received loans.

The following chart presents the distribution of the number of loans based on the age of the firm.

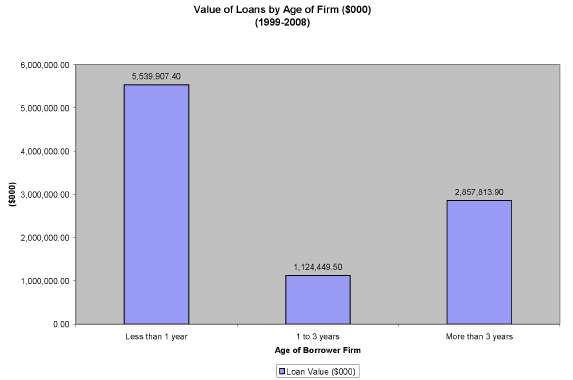

When examining the data in terms of total loan value, the above trend still holds true: SMEs that are less than 1 year old receive the largest CSBFP loan amounts, followed by SMEs that have been in business for more than three years. The group in between, SMEs that have been in business between 1 to 3 years have the lowest loan values.

The following chart presents the value of loans based on the age of the SME15.

Owner Characteristics

CSBFP borrowers are, on average, younger than other SME owners. 26% of CSBFP borrowers are between 30 and 39 years old, and, 43% are between 40 and 49 years old.

Owners of CSBFP borrowing firms have less managerial experience. 22% of the owners have less than 5 years experience, and, 20% have between 5 and 10 years experience.

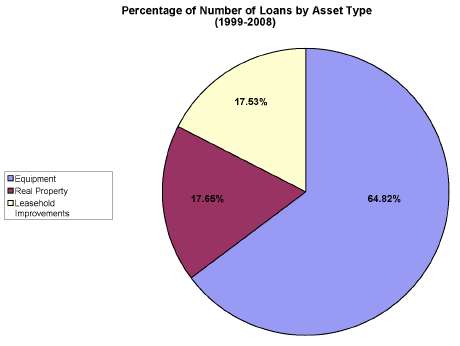

Loans by Asset Type

Between 1999 and 2008, the majority of the loans granted went towards "Equipment". Loans earmarked for "Real property" and "Leasehold Improvements" are not as prevalent, as the share of number of loans that corresponds to both of those categories dos not go beyond 18%.

The chart below presents the split of the number of loans based on asset type16.

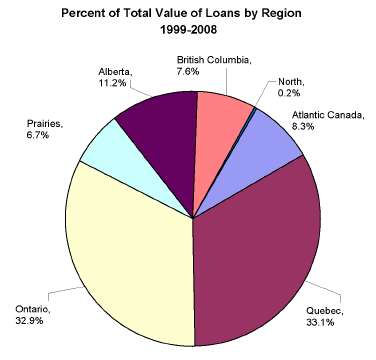

Provincial and Regional Distribution

Québec and Ontario are home to the majority of SMEs and the majority of CSBFP borrowers, 33.1% and 32.9% respectively. SMEs in rural areas only represent 19%, but they represent around 33% of CSBFP borrowers. The highest concentration of CSBFP borrowers are in urban areas.

Alberta has the third highest percentage of CSBFP borrowers at 11.2%.

top of page

1.5 Trends in the CSBF Program Portfolio17

The CSBFP portfolio of loans has undergone some changes over the past ten years. Although the profile of the portfolio presented above is as of 2007–08, the following table illustrates the trends that it is experiencing.

| Factor | Emerging Trends in the CSBFP Portfolio |

|---|---|

| Sector |

|

| Type of Borrower | Fewer sole proprietorships; more incorporated businesses. |

| Type of Operation | Proportion of franchises is increasing. |

| Age of Firm | New firms account for a high and increasing proportion of portfolio. |

| Size of Firm | Possible decrease in fraction of portfolio accounted for by one-person firms. |

| Size of Loan | Clear trend towards larger loans. |

| Class of Loan | Clear trend towards loans for financing leasehold improvements, possibly a result of higher frequency of loans to firms in the "Food services & drinking places" sector. |

2 http://www.ic.gc.ca/eic/site/csbfp-pfpec.nsf/eng/h_la02296.html#s4 (Return to Reference 2)

3 Industry Canada (2008). Canada Small Business Financing Act Annual Report 2007–2008, p. 3. (Return to Reference 3)

4 Ibid. (Return to Reference 4)

5 Industry Canada (2008), Canada Small Business Financing Act Annual Report 2007–2008, p. 18. (Return to Reference 5)

6 Industry Canada (2008), Canada Small Business Financing Act Annual Report 2007–2008, p. 18. (Return to Reference 6)

7 Industry Canada (2008), Canada Small Business Financing Act Annual Report 2007–2008, p. 18. (Return to Reference 7)

8 Industry Canada (2008), Canada Small Business Financing Act Annual Report 2007–2008, p. 22. (Return to Reference 8)

9 The top seven industries represent over 83% of the number of loans. (Return to Reference 9)

10 Industry Canada. (2008). Canada Small Business Financing Act Annual Report 2007–2008. p. 22. (Return to Reference 10)

11 Industry Canada. (2008). Canada Small Business Financing Act Annual Report 2007–2008. p. 26. (Return to Reference 11)

12 The values in the chart represent the value of loans for the entire portfolio of loans, between 1999 and 2008. (Return to Reference 12)

13 Industry Canada. (2008). Canada Small Business Financing Act Annual Report 2007–2008. p. 26. (Return to Reference 13)

14 Industry Canada (2009); CSBF—Borrowers under the Canada Small Business Financing Program. (Return to Reference 14)

15 The values in the chart represent the value of loans for the entire portfolio of loans, between 1999 and 2008. (Return to Reference 15)

16 Industry Canada. (2008). Canada Small Business Financing Act Annual Report 2007–2008. p. 19. (Return to Reference 16)

17 Equinox, Sources of Portfolio Risk. (Return to Reference 17)

2.0 Evaluation Study

2.1 Scope

The objective of the evaluation is to determine whether the program has met its objectives under the evaluation issues of relevance, success and economic performance.

Evaluation Issues

Evaluation issues were derived from the 2006 revised RMAF developed for the CSBF Program. The following are the evaluation issues and questions for this evaluation study:

| Evaluation Issue | Evaluation Questions |

|---|---|

| Relevance |

|

| Success |

|

| Cost-effectiveness |

|

| Program Delivery |

|

2.2 Approach

Planning for this evaluation began in the summer of 2008. The evaluation study was conducted over the period December 2008, through June 2009; and it is, to some extent, an update of the evaluation of the CSBF Program that was carried out in 2004.

The evaluation study was managed by the Audit and Evaluation Branch of Industry Canada. The evaluation was conducted by KPMG, and the team was led by the Associate Partner of Advisory Services, who had been involved in the 2004 CSBF Program evaluation. In addition, one AEB resource participated in the conduct of the interviews with lenders. The evaluation was done in consultation with a Steering Committee established for the purpose of the evaluation. (See Annex A for a list of Steering Committee members).

The evaluation has employed a synthesis approach of qualitative and quantitative evidence. Many pieces of research, which form the basis of this evaluation, were conducted by independent third parties using acceptable social science research methods.

top of page2.3 Methodology

Analysis of available data and documents

A significant portion of this project involved the review, analysis and integration of information contained in other studies and data collection activities. A complete list of the documents reviewed may be found in the bibliography. The most heavily used of these studies are described below.

- Evaluation of the Canada Small Business Financing Program—Final Report, BearingPoint, 2004.

The 2004 evaluation provided a benchmark and a good starting point for the majority of the questions addressed in this evaluation.

The 2004 evaluation addressed issues such as:

- Does an SME financing gap exist?

- Is there a need for a program such as CSBF Program?

- How cost recoverable is the program?

- How incremental are CSBFP loans?

- What is the level of awareness of the program, both from lenders as well as borrowers?

- SME-FDI Surveys, Statistics Canada, 2004 & 2007.

The SME-FDI is a knowledge base of information on SME financing in Canada.

The SME-FDI Surveys are undertaken every three years (first one in 2001), and the SME population surveyed are those enterprises that have fewer than 500 employees and have annual gross revenues of less than $50 million.

For the purposes of this evaluation study, findings from the 2004 and 2007 surveys were used. There were slight differences in the questions posed in each of the surveys. In 2004 a breakdown was done of those SME's that had "No credit authorized" by reason. In 2007 this breakdown was not identified. Rather the question focused on whether full or partial amounts were authorized. A separate question asked the reasons for turning down requests.

This data source was heavily used in this report as it contains relevant information about the type of debt, capital lease and equity financing that SMEs use.

As well, SME-FDI data was used in some of the research undertaken by Industry Canada in the area of SME financing. Some of these research papers were used as references in this report.

- Sources of Portfolio Risk and Revenue Generation of the Canada Small Business Financing Program phase 1 & 2, Equinox Management Consultants Ltd, 2008.

The objective of this two phased study was to examine the drivers of risk within the CSBFP loan portfolio and determine how the specified "risk" characteristics of CSBFP borrowers and loans relate to the program's risk and cost recovery.

Phase 1 focused mainly on discussing the risk profile of the CSBFP portfolio, while the focus of phase 2 was to estimate the impact of these risk factors in the CSBFP objectives of incrementality and cost recovery.

- Canada Small Business Financing Program(CSBFP), Awareness and Satisfaction, Phoenix Strategic Perspectives Inc., (2007)

The objective of this study was to better understand the experience of businesses when they try to obtain financing, as well as the extent to which they are aware of and satisfied with the Canada Small Business Financing Program Program.

To accomplish that, the authors present the characteristics that define CSBFP borrowers when compared to non borrowing SMEs, as well their level of knowledge about the program.

- Canada Small Business Financing Program: Updated Analysis of Incrementality, Canada Works Ltd. (2009)

The objective of this research study was to update an incrementality model for the CSBF Program, which had originally been developed in 2004 to determine the extent to which loans made under the CSBF Program are incremental.

The first stage of the research was the construction of the model with the appropriate parameters and statistical properties using logistic regression. Then the model was used to determine outcomes (turned down or not) of decisions on loan applications for non-guaranteed loans using data on firms comparable to those which had received CSBFP loans.

The second stage of the analysis uses the resulting model to classify CSBFP loans as to whether or not the applications would have been turned down in the absence of the CSBF Program.

- Canada Small Business Financing Act—Annual Report 2007–2008, Industry Canada, 2008

The annual report contains information about the uptake of the CSBF Program, as well as key statistics that describe the CSBFP borrowing population, from the inception of the Program in March 1999 to 2007–2008.

Stakeholder Interviews

The data collection for this study involved interviews regarding several of the evaluation questions with senior representatives of stakeholder organizations – borrowers, lenders, and government stakeholders. A total of 43 stakeholder organizations were identified in consultation with Industry Canada as organizations representing important participants in the program who would be expected to be knowledgeable regarding these questions. Of these, 37 were able to be interviewed. The breakdown of the interview sample and responses by type of organizations follows:

| Lending Organizations | Borrower Representative Organizations | Government Stakeholders | |

|---|---|---|---|

| Completed | 30 | 3 | 4 |

| Unable to reach or unwilling to participate | 6 | 0 | 0 |

| Total | 36 | 3 | 4 |

A list of the organizations that were interviewed is presented in Annex B. The interview guides were designed to address questions regarding:

- difficulties that SME face when accessing financing;

- role of the CSBF Program in mitigating SME financing difficulties;

- specific cases in which the CSBF Program is suggested;

- lender's views of alternative loan guarantee programs, and

- potential risks for the program from the lender's perspective

Please refer to Annex L for the interview guides.

Risk Workshop

A risk assessment workshop, held on May 28th, 2009, was undertaken to define the main risks to the CSBF Program. Industry Canada officials involved in the policy and operational aspects of the program participated in the session.

The workshop had three main objectives:

- Identification and review of risks to the program.

- Assessment of the likelihood and impact of CSBF Program's risks.

- Likelihood and impact of risks to the program after introducing controls and management to address the risks.

Cost Benefit Analysis

A separate Cost Benefit Analysis study was undertaken to complement this evaluation and to inform the evaluation issue of cost effectiveness. This study was undertaken by KPMG.

The cost-benefit analysis examined the full social benefits and costs of the CSBF Program. This analysis was conducted to inform Industry Canada of the impact to businesses in receipt of loans under the CSBF Program and the impact to the Canadian economy.

The Cost-Benefit Analysis examined the nine-year time period from 1999–2000 to 2007–2008. The period of analysis includes the time period since the creation of the CSBF loan guarantee program in 1999–2000. The costs and benefits, as well as broader economic impacts associated with loans provided in any given year are realized during a lag period, in some cases even near the end of the maximum 10-year amortization period for loans. 2008–2009 has been excluded from the analysis due to a lack of all data for that period at the time of this study.

top of pageLimitations to the Methodology

Important data issues were encountered during the documentation review and data analysis phases of this study. These limitations have centered mostly on data availability and data quality.

Data Availability

- The individual studies, reports and borrower's survey which represent the key data sources for this evaluation were commissioned by the Small Business Financing Directorate (SBFD) as per the approved RMAF for the CSBF Program. However, the terms of reference for these were developed without the involvement of the Evaluation Directorate. As such, some of the data obtained does not directly answer the evaluation questions.

- The borrower's survey contracted to Phoenix and Associates by SBFD was focused on awareness and satisfaction with respect to the terms and parameters of the CSBF Program. It did not address the impact/outcomes achieved by SMEs as a result of obtaining a loan under the CSBF Program. Although the Evaluation Directorate and KPMG specifically recommended that the borrower's survey be repeated as part of this evaluation study in order to contribute to the analysis of outcomes, SBFD declined due to financial constraints. To attempt to compensate for this, interviews were conducted with two associations that represent broad categories of borrowers, together with one member of an association who was also a borrower under the CSBF Program. Therefore, this study is limited in its ability to evaluate the outcomes of the program with respect to the effect on the borrowers.

- The data available in the longitudinal study has significant limitations when it comes to answering the question "Which firms/industries and loan characteristics create the most economic impact?" The hypotheses presented to Statistics Canada to analyze were at a higher level than required in order to properly respond to the question. Rather than testing for hypotheses such as: "CSBF loans promote one of the following two outcomes: sales and employment growth or, lower production costs and higher labour productivity", the hypothesis should be more targeted to be able to obtain meaningful results and answer the question adequately. A hypothesis such as "CSBF Loans promote employment growth in each of the 19 industries" and providing the list of industries that are most relevant, would help Statistics Canada run the appropriate tests and provide good quality data to answer the question.

- Obtaining information to respond to the question concerning the comparison of the CSBF Program to other programs at a federal and provincial level was difficult as most entities only provide a high level description of the program, and key elements in the comparison such as maximum loan amount, interest charged, and fees or repayment terms are withheld. This information is only available by contacting one of their advisors. This was particularly true when conducting the comparison between the CSBF Program and the BDC.

Data Quality

In the Statistics Canada Economic Impact Study it is unknown whether the comparator group received or did not receive a conventional loan. As a result, the interpretation of the findings of this study is qualified in the appropriate sections.

Generalization of Certain Study Findings to the CSBF Program

The SME population surveyed for the Statistics Canada SME-FDI surveys are those enterprises that have fewer than 500 employees and have annual gross revenues of less than $50 million. This definition differs from that used by the CSBF Program. Although a subset of the respondents are CSBFP borrowers, the findings from the survey cannot be generalized to be representative of the potential population of SMEs as defined by the CSBF Program.

Evaluation Findings

3.0 Relevance

3.1 To what extent does the CSBF Program align with Industry Canada's mandate and government directions?

Findings

Industry Canada's delivery of the CSBF Program is consistent with its mandate and Government directions.

The Program's mandate is derived from the Department of Industry Act and Canada Small Business Financing Act. The CSBF Program is also a separate identified element of Industry Canada's Program Activity Architecture and contributes to the strategic outcomes Competitive Businesses are Drivers of Sustainable Wealth Creation. Finally, the Program is consistent with the small business priorities of the Government, and its parameters were specifically enhanced in the 2009 Budget.

Discussion

A variety of documentation was examined to ascertain whether Industry Canada's delivery of the CSBF Program is consistent with Industry Canada's mandate and government directions. These documents included the Department of Industry Act, Canada Small Business Financing Act and Regulations, the federal Budgets and Industry Canada's Program Activity Architecture.

The Department of Industry Act states in Part I, Section 4.1(n) that the Minister's responsibilities include all matters relating to small businesses.

The CSBF Program is governed by its own legislation, the Canada Small Business Financing Act and its associated regulations, the Canada Small Business Financing Regulations, which set out the parameters of the program and the obligations of the Crown.

Current Government priorities as set out in the 2009 Budget show the commitment to the financing issues experienced by small businesses. The budget increased two specific parameters of the CSBF Program, the size of the loan amounts that could be guaranteed and the total percentage of the losses that lenders are allowed within their portfolio of loans.

The official Industry Canada MRRS strategic outcome Competitive Businesses are Drivers of Sustainable Wealth Creation is directly related to the CSBF Program. The CSBF Program is situated in the Program Activity Architecture under the program activity Entrepreneurial Economy and is its own defined sub-activity element.

top of page3.2 To what extent is there a marketplace financing gap for SMEs—i.e., to what extent are SMEs disadvantaged relative to non-SME's in obtaining financing from the financial markets?

To what extent does the CSBF Program fill the marketplace gap and meet the financing needs of SMEs?

Findings

Based on the literature reviews there is no consensus on a standard definition of a financing gap, but rather a widespread belief that SMEs have more difficulty obtaining financing than large firms. SMEs for which the level of risk is higher than the risk threshold of financial institutions have difficulty obtaining financing, but this would also be the case for large firms with the same level of risk. This means that while there may be a gap, it is a "high risk loan gap," not an "SME gap". Evidence identifies those businesses with the highest risk characteristics as: very young businesses, which would include start-ups; those with insufficient collateral; and those SMEs operating in less stable industries, such as Food and Beverage services. In addition there are some types of expenditures that lenders consider to be risky because of the difficulty in recovery in the event of a default; particularly expenditures related to leasehold improvements.

While the main finding is that there is no financing gap, the main factors that influence lenders to offer the CSBF Program to potential borrowers are lack of collateral and small size of firm. Therefore a gap appears to exist for very young businesses with limited experience, lack of collateral and which have a high credit risk score. As a result, the CSBF Program fills a marketplace financing gap for these types of firms.

Discussion

This question examines whether there is a financing gap for SMEs, but not whether there is a financing gap for those SMEs as defined by the CSBF Program (for-profit, gross revenues under $5M).

The list of studies reviewed for this evaluation include the OECD's SME Financing Gap, Theory and Evidence, KPMG's evaluation of the UK Small Firms Loan Guarantee Scheme, Green's analysis of Credit Guarantee Schemes for Small Business, Equinox's analysis of Working Capital Financing and the CSBF Program, CFIB's 2007 Banking Matters Survey and, the SBFD's gap analysis document. The analysis of this question was also based on the review and analysis of Statistics' Canada's SME-FDI data, as well as interviews with lenders and borrowers.

A number of researchers have tackled the issue of a possible "financing gap" for SMEs, but one of the challenges in carrying out this research has been that there is no commonly accepted definition of a financing gap.

Based on the research consulted, three prevalent views exist on the topic of the "SME financing gap". All of these views relate to the same underlying concept, and the differences lie mainly in the level of restrictions that the definition imposes.

Defining the Gap

Three main definitions are used in the literature:

- SMEs have difficulty obtaining financing.

- SMEs have more difficulty obtaining financing than large firms (i.e., because factors used in lending decisions are, in general, disadvantageous to SMEs, such as the level of risk of the loan).

- SMEs have more difficulty obtaining financing than large firms simply because they are SMEs (i.e., because of biases).

| Definition 1 | Definition 2 | Definition 3 |

|---|---|---|

| OECD: "A financing gap exists if a sizeable share of economically significant SMEs cannot obtain financing from banks, capital markets, or other suppliers of finance." | Used implicitly by many authors, based on the fact that, in general, loans to SMEs are riskier. | CFIB: There is discrimination against small and younger firms…18 |

| Equinox: "A gap exists when identifiable groups in the population are unable to obtain financing at any price."19 | Equinox: "A gap exists where groups of businesses are systematically denied access to financing that they ought to, based on objective criteria, be able to access.20 | |

| KPMG (UK): A financing gap is a situation where two borrowers with an equal probability of repayment have an unequal probability of obtaining credit."21 |

SMEs have Difficulty obtaining Financing

This interpretation of the "financing gap" is the most intuitive and the broadest. It is the one used by the OECD in its report, The SME Financing Gap: Theory & Evidence22 which simply states that SMEs have difficulty obtaining financing, although they are clear that evidence to support this finding is limited. According to the OECD, a "financing gap" exists if "a sizeable share of economically significant SMEs cannot obtain financing from banks, capital markets or other suppliers of finance".

The OECD postulates that there are four categories of financing gaps: inherent structural weaknesses in the financial system; the use of capital markets as a source of capital as opposed to the banking system; financial systems which marginalize SME's of specific types and in specific industrial segments; and country-specific policies that marginalize SME's of specific types and in specific industrial segments.

The paper Gaps in SME Financing: An Analytical Framework23 uses a very similar definition. According to this paper, the gap is a situation in which "identifiable groups in the population are unable to obtain financing at any price". The paper argues that the idea of a gap conveys the concept of a shortage, which in economic terms translates as demand being larger than supply. As a consequence, this gap can only exist if there is an imperfection and the total demand for loans by borrowers is not equal to the total supply of loans from lenders and the loan market is not in equilibrium (markets cannot clear).

The concept of specific types of SMEs not gaining access to financing was also adopted in SBFD's analysis of the SME-FDI data. It is important to emphasize the difference between the concept of SME used in the SME-FDI data analysis and that being used in the context of the CSBF Program. The SME-FDI uses the Statistics Canada definition of an SME; an enterprise that employs fewer than 500 employees and generates an annual gross revenue of less than $50 million. The CSBFP definition is a subset of that and is considerably more restrictive, as, in order to be eligible for the CSBF Program, an SME has to have gross revenues or projected revenues of less than $5 million.

The US SBA gap analysis study, also discussed the concept of the inability of specific types of SMEs to obtain financing.

SMEs have more Difficulty obtaining Financing than large Firms

The second interpretation of the gap, which is closely related to the first interpretation, states that SMEs have more difficulties obtaining financing than larger firms.

SMEs are defined as enterprises that have fewer than 500 employees and have annual revenues of less than $50 million24. Their structure, age, and business track record differ significantly from those of large firms, and it is believed that these factors affect their probability of obtaining financing.

This interpretation of the financing gap is used consistently across the literature and it conveys the message that SMEs are generally not as credit-worthy as larger firms. Some of the reasons that are frequently cited for this are as follows:

- SMEs, because of their age, do not have collateral to obtain credit (compared to larger firms that do).

- SMEs do not have an established business track record.

- In general, loans to SMEs are systematically perceived to be riskier than loans to large firms.

SMEs have more difficulty obtaining financing than large firms because they are SMEs

The third interpretation, and the most restrictive, states that SMEs have more difficulties obtaining financing than large firms because they are SMEs—i.e., not necessarily because their loan is riskier. This interpretation of the gap implies that SMEs are disadvantaged in obtaining financing simply because they are SMEs, not for reasons related to the risk of the loan.

According to this interpretation, the main reasons why financial institutions would deny financing to an SME just for being an SME would include:

- Lender's aversion to lending to SMEs (i.e., favouritism toward large firms).

- Lack of business interest in lending smaller amounts (e.g., because of higher relative costs of processing small loan applications).

- Lack of information about the company (e.g., because of the short life of the organization).

Existence of a Gap

Based on the evidence in the literature, it is difficult to support the existence of a financing gap for SMEs. Most of the studies reviewed have concluded that no conclusive evidence exists to support the concept of a financing gap. For example:

- The OECD study found that, even using definition 1, there is no conclusive evidence to support the existence of a financing gap.

- Research done by Equinox Consulting also concludes that there is no evidence to support a financing gap.

- Research conducted by Industry Canada concludes that the number of SME loans rejected is low, which supports the argument that there is no gap.

There are some studies that state that a financing gap exists, but they provide no data to support this. Examples are the KPMG UK Evaluation, the US SBA gap analysis, and the 2007 survey report by the CFIB, Banking Matters25.

top of pageOther Forms of Gaps

While a gap has been difficult to establish from the evidence examined as part of many pieces of literature and other studies, it is recognized that SMEs do have difficulty obtaining credit in various circumstances, and in certain industries.

Difficulties Obtaining Credit

Based on the results of the lender interviews conducted in this study, the slight majority of lenders mention that SMEs do indeed have more difficulties obtaining financing compared to other firms, but these difficulties are most often related to banks' aversion to risk (i.e., they stated that, if one adopts definition 2, there is a gap). Analysis indicates that 47% of lenders interviewed mentioned that SMEs did face difficulties obtaining financing, 33% of respondents indicated that SMEs did not have difficulties obtaining financing, while 20% were not able to provide an answer.

Industrial Sector

The Statistics Canada SME-FDI survey groups responses by the following industries: Agriculture/Primary, Manufacturing, Wholesale and retail, Professional services, Knowledge-based industries, Accommodations and food services, and Other industries. The rates of loan rejection or, "non-authorized credit" vary significantly from one industry to another, but the findings do provide an insight about the rate of credit approval by sector.

It is important to note that the percentage of each industrial sector seeking credit approval varies over the 2004 and 2007 SME-FDI surveys. When examining the rates of approval by industrial sector, it is difficult to identify which specific industrial sectors have more difficulties obtaining loans compared to others, as the rankings change significantly between the two surveys. Also, the industrial sector breakdown changes between the surveys. In 2004, Tourism was identified (and constructed) as a separate sector; while 2007 it was included in "Other Industries". In 2007 Accommodation and Food Services was identified as a separate sector; while in 2004 it was included in "Other Industries".

In 2004, of the seven industrial sectors listed above, and of those SMEs requesting debt financing, the one that seemed to have the most difficulties obtaining credit approval was the manufacturing sector, which had 64.2% of its requests approved. However, when examining the 2007 data, that industrial sector had the third highest approval rate of 87.5%26.

In 2004, in the case of SMEs in the Knowledge Based Industry (KBI), their rate of credit approval at 70.2% was the second lowest. In 2007, KBI had the third lowest rate of credit approval at 84.5%.

Note that within the context of the CSBF Program, the majority of loans are in the Other Services sector and the "Food and Beverage" subsector of Accommodation and Food Services27. As mentioned above, the 2004 SME-FDI does not break out this industrial sector but rather included it under "Other Industries". In 2007 the SME-FDI does break out the findings by this sector, and finds that 80% of those requesting credit in the Accommodation and Food Services Sector had the credit authorized.

Size of Business

The Statistics Canada SME-FDI survey findings on rates of approval based on the size of business are more consistent across time compared to the breakdown by industry. The SMEs that have the highest rate of approval are those with over 99 employees.

Smaller firms have more difficulties getting financing, and this is true particularly for the firms without employees and those with 1 to 4 employees. Firms without employees had a rate of approval of 79.5% (the lowest level) in 2004, and of 85.5% (second lowest level) in 2007. Similarly, firms with 1 to 4 employees had a rate of approval of 81.2% (the second lowest level) in 2004, and of 84.6% (lowest level) in 2007. Even though the rates of approval may seem high, they are slightly below the averages, which were 83.2% in 2004 and 89% in 2007.

Gaps in Products Offered

While not specifically defined in the literature, another concept of gap in financing for SMEs could be with respect to the financing products offered in the commercial marketplace. There have been various studies commissioned by the Industry Canada SME-FDI analysis group and the SBFD group, which have examined whether gaps exist in financing for working capital and risk capital, including venture capital. This discussion will not explore venture capital, which is very high risk and usually involves taking an equity stake in a company.

In the 2006 Study on Working Capital Financing and the CSBF Program, Equinox examined the requirement for working capital, whether there was a gap for this product, and whether the reason for seeking credit for working capital influenced the turn-down rates. From both the qualitative and quantitative review, the data was not consistent with the hypothesis that applications for working capital loans are turned down any more frequently that other loans, given age, size, sector, and other reasonable factors in the loan decision.

The OECD28 places particular emphasis on financing gaps experienced by innovative SMEs (ISMEs); those SMEs that seek to exploit innovation for growth and competitive advantage. In the particular case of ISMEs, a financing gap exists when it comes to the type of financing, as debt financing (as opposed to equity financing) is not suitable for ISMEs and, makes obtaining financing more complicated.

Another gap that may currently exist was the one left by the end of the Capital Leasing Pilot Project, which had been offered by CSBF Program from 2002–2007. In absence of that program, assets such as new equipment and used equipment that has a remaining economic life greater than the term of the lease can no longer be financed through a government loan guarantee program. Although judging by the fact that the pilot was discontinued due to a lower than anticipated number of companies participating as a result of high levels of approval for these types of loans through conventional means, the existence of this gap can be questioned.

Findings from Lenders and Borrowers

During this evaluation study, interviews with both lenders and borrower representatives included questions about whether there were certain products that they felt represented a gap under the CSBF Program.

Lenders provided an extensive list of additional products they felt could be offered to borrowers through the CSBF Program without necessarily increasing the level of risk, which may be representative of a gap. The following kinds of financing were most commonly mentioned and supported:

- Working capital (thought to be no more risky than leasehold improvement loans)

- Rentals

- Inventory

- Purchase of shares (when the borrower is purchasing a business)

- Goodwill and intangibles

- Franchise fees

- Current account financing

- Renting of space

Borrower representatives mentioned a variety of fees (franchise fees, consultant fees, etc.) and support for market development and brand development (although one of the three borrower representatives did not agree with expanding the types of assets covered by the CSBF Program).

Reasons for Loan Rejection

While there is disagreement over the definition of a gap, a review of the literature found that studies focus on the reasons for loan rejection, and provide essentially the same reasons regardless of what definition is being used for the "financing gap." In addition the SME-FDI surveys also provide information about the reasons for loan turndowns.

Therefore, the following analysis will focus on the reasons why SMEs are believed to have a higher rate of loan rejection.

Main reasons

The most frequent reasons SME loan applications are turned down, according to the literature, are:

- Asymmetric information (i.e., lenders do not have the same amount and quality of information as borrowers)

- Lack of relationship with banks

- Small business size

- Principal/agency problems

- Lack of management skills and poor business plan

- Lack of a track record and collateral

- Conservative nature of financial markets.

Many of these are related to the perceived higher level of risk associated with loans to many SMEs.

According to the 2007 survey Banking Matters conducted by CFIB, reasons cited by their members as reasons for difficulties in obtaining credit include: small size of business, fewer years of experience in business, and that the business is in hospitality sector.

Reasons Identified in the Statistics Canada SME-FDI Surveys

In 200429, only 18.5% of SMEs approached a credit supplier in the previous twelve months, while in 200730, only 18% did.

In 2004 in the case of all SMEs, the number one reason why credit suppliers refused to provide credit is "Insufficient income, sales or cash-flow," accounting for 30.4% of all rejections. "Other reasons31" was the second reason for refusal (23.5%), "Insufficient collateral security" was the third reason for refusal (18.1%), and, "Poor credit experience or history" was the fourth reason (14.3%).

In 2007, in the case of all SMEs, the number one reason why credit suppliers refused to provide credit is "Other" accounting for 43% of all rejections. "Insufficient Collateral" and "Business is too young" were the refusal reasons that had the second highest percentage (25%), and, "Insufficient sales, income or cash flow" was the fourth reason for refusal at 24%.

Rejection reasons by industry are very sparse and are not available for all industries. Based on the limited data available32, 9% of SMEs in the "Other Industries" sector were turned down for an unspecified reason. In the "Manufacturing" sector, 6% of loan applicants were turned down due to "Insufficient Collateral" and, 2% of SMEs in the "Accommodation and Food Services" were turned down due to "Business operates in an unstable industry" and, 2% were turned down due to the fact that the "Business is too young". In 2004, in the case of SMEs in the Knowledge Based Industry (KBI), 30.4% were refused due to "Insufficient income, sales or cash flow".

Reasons Identified by Lenders

Lenders who believe SMEs have difficulties obtaining financing were asked about the reasons that influence their opinion. All of these lenders believe that it is particular SME characteristics that make them ineligible to get financing as these characteristics increase the risk profile of the SME. Lenders presented the following as reasons why SMEs get turned down (in random order):

- Financial health of SME

- Lender having doubts about the capacity of SME to repay loan

- Low capitalization of SME

- Type of collateral presented

- Industrial sector in which SME does business

- Age of SME

- Lack of track record

- Lack of investment from firm's owners.

In summary, there is no conclusive evidence to indicate that SMEs have more difficulty obtaining financing than large firms simply because they are SMEs—i.e., SMEs are not disadvantaged relative to large firms. However, firms that are higher risk with regard to their likely ability to repay loans do have more difficulty obtaining financing than lower risk firms, and many SMEs, such as start-ups, fall into this high risk category.

top of page3.3 Are there viable alternatives to a federal loan-loss sharing program, which would not rely on delivery by the federal government?

Findings

There are no attractive alternatives to a federally managed loan loss guarantee program similar to the CSBF Program, yet offered by other sectors. Interviewed lenders did not see any incentive for private financial institutions to offer an equivalent loan guarantee program and they were not aware of any existing loan loss guarantee programs either in Canada (aside from the CSBF Program) or around the world that did not rely on government involvement.

A potentially viable alternative could be a loan loss reserve fund program, into which the federal government contributed, but otherwise was not directly involved in the program delivery or claims process. This type of program could have some relatively minor advantages to the CSBF Program, mainly administrative simplicity, but it would reduce the degree of control of the government in the claims process, which may not be acceptable. For a program with as large a loan portfolio as the CSBF Program (about $1 billion per year) and consequent large loan losses, taxpayers may want certain controls on claims payments (e.g., assurance that guidelines were followed, assurance that loans were used for the intended purposes).

A few loan loss reserve programs have been implemented in Canada. One federal government program, WED's Loan and Investment Program, has existed since 1995 and could serve as a model. INAC has just launched a new "Loan Loss Reserve Initiative" for medium and large aboriginal businesses, in partnership with the BDC. In the recent past, Heritage Canada had piloted a loan loss reserve program, which was subsequently abandoned when the lender advised that they would no longer participate in the program because of the high risk.

The concept of a government-supported system of mutual guarantee associations was considered in this evaluation. These are popular in the European Union, and serve mainly to address the problem of asymmetric information between borrower and lender, often within specific sectors. However, this issue, while identified as one of several reasons for potential difficulties in obtaining credit in Canada, has not been a core reason or a significant issue. Some of these associations also serve to guarantee loans made through conventional lenders to businesses within their sector. This role would require the implementation of a legislative and regulatory system to allow them to exist. These kinds of associations could reduce the options available to the federal government for direct intervention to support SMEs with the objective to stimulate economic development.

The question of alternative programs was presented to interviewed lenders and none of them was able to present an alternative. Lenders believe that the CSBF Program should be federally administered and that the responsibilities for managing a similar program should not be transferred to private sector organizations. Lenders also mentioned that financial institutions such as theirs would not be interested in offering such a program.

The 2004 BearingPoint evaluation also sought to explore viable alternatives to federal loan-loss sharing program. "Viable alternatives" were considered to be different types of programs that would not rely on the delivery of the program by the federal government33. In these alternatives, the federal government would still be responsible for guaranteeing the loans, but the administration of the program would be devolved to other organizations (private sector lenders, provinces or BDC).

The 2004 evaluation report concluded that the alternatives would be impractical for three main reasons34:

- The administration of the program requires very few resources (in 2008–2009, the program had 31 FTEs and a salary budget of $2 million) which makes contracting out the administration not a very interesting cost saving measure.

- Policy decisions made by Industry Canada are politically sensitive.

- Large amounts of federal money are at stake.

All these reasons apply to all three categories of alternatives—i.e., delivery by the private sector, the provinces, or the BDC. Devolution to the provinces or the BDC would have additional disadvantages. Devolution to the provinces would have the additional disadvantage of being unable to ensure uniform program delivery across the country. Devolution to the BDC would have the additional disadvantage that lending organizations would most likely be uncomfortable with the BDC having information on their loan portfolios, since the BDC also has a commercial mandate.

In the current context, the findings reached in the 2004 BearingPoint evaluation still holds true.

Discussion

This question was interpreted as whether there were different types of alternative programs that would not rely on the delivery of the program by the federal government—not alternate systems that would mirror the current program but without the federal government involved in the program delivery. This means that the federal government would not be involved in the registration of loans or in the decisions concerning claims.

The approach to this question was based on the review of literature where alternative options to having the federal government deliver the program were considered. The results from the literature review, and other publicly available program documentation, were complemented with the feedback obtained from lender and borrower interviews.

Research was conducted to establish if alternatives to having a federally managed loan guarantee program exist, and two options were considered:

- A mutual guarantee association system and,

- A loan reserve fund.

Mutual Guarantee Associations

Mutual Guarantee Associations are private societies formed by potential borrowers, possibly together with other partners. There must be a legal and regulatory environment under which they can operate.

The main rationale for these associations in the countries in which they exist, mainly the European Union, appears to be to provide better information to lenders regarding potential loans by virtue of local knowledge and entrepreneur representation, thus addressing the problem of asymmetric information between borrower and lender. The association thus plays the role of an intermediary between the businesses and banks; businesses join the association to obtain credit from banks and the association negotiates with banks to secure loans for its members.

Green35 presents these associations as the best option as they are perceived to be better equipped to deal with the problem of "asymmetric information", meaning that borrowers have more information than lenders regarding the viability of their projects and their ability and willingness to repay, so lenders have difficulty distinguishing between good and bad loans36.

Lack of information for evaluating loan applications does not appear to be a significant problem in Canada. In addition, there is no indication in the literature that mutual guarantee associations support riskier loans than would be supported by lending institutions on their own if they had access to complete information regarding the loan.

Loan Loss Reserve Fund Programs

Definition