PDF version

Evaluation of the Community Futures Program

1.1 MB, 45 pages

Final Report April 2014

Presented to the Departmental Evaluation Committee on March 26, 2014

Approved by the Deputy Minister on April 29, 2014

This publication is also available online at: www.ic.gc.ca/eic/site/ae-ve.nsf/eng/h_03683.html

To obtain a copy of this publication or an alternate format (Braille, large print, etc.), please fill out the Publication Request Form at www.ic.gc.ca/Publication-Request or contact the:

Web Services Centre

Industry Canada

C.D. Howe Building

235 Queen Street

Ottawa, ON K1A 0H5

Canada

Telephone (toll-free in Canada): 1-800-328-6189

Telephone (Ottawa): 613-954-5031

TTY (for hearing-impaired): 1-866-694-8389

Business hours: 8:30 a.m. to 5:00 p.m. (Eastern Time)

Email: ic.info-info.ic@canada.ca

Permission to Reproduce

Except as otherwise specifically noted, the information in this publication may be reproduced, in part or in whole and by any means, without charge or further permission from Industry Canada, provided that due diligence is exercised in ensuring the accuracy of the information reproduced; that Industry Canada is identified as the source institution; and that the reproduction is not represented as an official version of the information reproduced, nor as having been made in affiliation with, or with the endorsement of, Industry Canada.

For permission to reproduce the information in this publication for commercial purposes, please fill out the Application for Crown Copyright Clearance at www.ic.gc.ca/copyright-request or contact the Web Services Centre (see contact information above).

© Her Majesty the Queen in Right of Canada, as represented by the Minister of Industry, 2014

Cat. No. Iu-lu4-154/2014-E-PDF

ISBN 978-1-100-24444-0

Aussi offert en français sous le titre Évaluation du Programme de Développement des Collectivités.

Table of Contents

- Executive Summary

- 1.0 Introduction

- 2.0 Methodology

- 3.0 Findings

- 4.0 Conclusions and Recommendations

- Evaluation of the Community Futures Program Management Response and Action Plan

List of Acronyms used in Report

| Acronym | Meaning |

|---|---|

| APR | Annual Performance Report |

| ACOA | Atlantic Canada Opportunities Agency |

| AEB | Audit and Evaluation Branch |

| BDC | Business Development Bank of Canada |

| CSBFP | Canada Small Business Financing Program |

| CF | Community Futures |

| CFP | Community Futures Program |

| CFDC | Community Futures Development Corporation |

| CED-Q | Economic Development Agency of Canada for the Regions of Quebec |

| EDI | Economic Development Initiative |

| FedDev | Federal Economic Development Agency for Southern Ontario |

| FedNor | Federal Economic Development Initiative for Northern Ontario |

| IC | Industry Canada |

| LIC | Local Initiatives Contribution |

| NODP | Northern Ontario Development Program |

| NOHFC | Northern Ontario Heritage Fund Corporation |

| OACFDC | Ontario Association of Community Futures Development Corporations |

| OSEB | Ontario Self-Employment Benefit |

| PM | Performance Measurement |

| RDA | Regional Development Agency |

| RED | Rural Economic Development Program |

| SMEs | Small and Medium sized Enterprises |

| SBEC | Small Business Enterprise Centre |

| SFT | Speech from the Throne |

| TEA | The Exceptional Assistant |

| WD | Western Economic Diversification Canada |

List of Tables

List of Figures

| Figure # | Figure title |

|---|---|

| Figure 1 | Community Futures Development Corporations in Northern Ontario |

| Figure 2 | Community Futures Program Logic Model |

Executive Summary

Program Overview

The Community Futures Program (CFP) supports rural economic development across Canada through four key activities: working with local partners to advance strategic community planning and socio-economic development; providing business services to small and medium-sized enterprise (SMEs); providing access to capital for SMEs; and supporting community-based projects and special initiatives. In Northern Ontario, the program is delivered by Industry Canada's Federal Economic Development Initiative for Northern Ontario (FedNor), which provides funding to 24 Community Futures Development Corporations (CFDCs) to support costs related to delivering the four key activities. These CFDC's are independent, arms-length organizations that employ professional staff and are governed by volunteer local boards of directors.

Evaluation Purpose and Methodology

In accordance with the Treasury Board Policy on Evaluation and the Directive on the Evaluation Function, the purpose of this evaluation was to assess the core issues of relevance and performance of the CFP. The evaluation covered the period from April 2008 to March 2013.

The evaluation findings and conclusions are based on the analysis of multiple lines of evidence. The methodology included a review of documents, a literature review, a review of program and Statistics Canada data, case studies, a survey of clients and interviews with clients and stakeholders.

Findings

Relevance

The economic situation in Northern Ontario and the barriers experienced by small businesses in this region suggest a continued need for the CFP. While the need for services varies by community depending on local capacities and the availability of alternate services, the flexibility of the CFP allows CFDCs to target their services in areas where they are most needed.

Industry Canada has a clear mandate to deliver rural economic development activities in Northern Ontario under the Department of Industry Act and such activities continue to be priorities of the Government. CFP is also aligned with Industry Canada's strategic outcomes and activities related to community economic development and developing competitive Canadian businesses and communities. The province and municipalities also provide rural economic development programs in Northern Ontario and while some of their programs may be similar to those offered under the CFP, their availability is often more limited and their eligibility criteria differ.

Performance

Overall, evidence suggests that CFP is achieving its intended immediate and intermediate outcomes. However, some outcomes are partially attributable to the Northern Ontario Development Program (NODP), which has provided funding to CFDCs to capitalize their Investment Funds and support the implementation of community economic development projects. CFDCs primarily focus on providing access to capital and business services, and, therefore, show the greatest impacts through these activities. Ultimate outcomes are difficult to attribute directly to CFP as a number of factors can influence these outcomes; nonetheless, data collected from Statistics Canada and CFP clients suggest that the CFP is contributing to job creation and economically sustainable local rural economies.

The program also appears to have had an incremental impact. A Statistics Canada comparison of CFP assisted businesses to matched non-assisted businesses showed that CFP-assisted businesses had higher employment growth, sales growth and business survival rates than non-assisted businesses. Further, a high proportion of surveyed loan clients indicated it would have been unlikely that they would have been able to start or expand their business in the absence of the CFP loan.

The delivery of the CFP is efficient in that the program's flexibility allows CFDCs to focus on activities within their communities that will have the greatest impact. While the loan component has been efficient in achieving leveraging, the overall loan loss ratios are low and cash reserves held by some CFDCs are high. There is an opportunity for FedNor to explore why this is occurring and determine whether further action is required.

Recommendations

The evaluation led to the following recommendations:

- FedNor should continue to further develop the CFP Performance Measurement Strategy in concert with its RDA partners (e.g., examine whether to expand data collection to cover all indicators in the Performance Measurement Strategy and add additional outcome indicators).

- FedNor should examine the reason for the overall low loan loss ratios and high cash reserves held by some CFDCs and determine whether further action is required.

1.0 Introduction

This report presents the results of an evaluation of the Community Futures Program (CFP) as delivered by Industry Canada (IC). It should be noted that the national delivery of the CFP is shared with the four Regional Development Agencies (RDAs): the Atlantic Canada Opportunities Agency (ACOA), the Economic Development Agency of Canada for the Regions of Quebec (CED-Q), Western Economic Diversification Canada (WD), and the Federal Economic Development Agency for Southern Ontario (FedDev). The RDAs are conducting their own individual evaluations of CFP. Throughout this document, references to the performance of CFP will relate solely to that of IC unless otherwise specified.

The purpose of the evaluation was to assess the relevance and performance of CFP. The report is organized into four sections:

- Section 1 provides the profile of CFP;

- Section 2 presents the evaluation methodology, along with a discussion of data limitations;

- Section 3 presents the findings pertaining to the evaluation issues of relevance and performance; and,

- Section 4 summarizes the evaluation's conclusions and provides recommendations for future action.

1.1 Program Description

The CFP is a federal government program that supports rural economic development across the country with the ultimate objective of assisting communities to:

- foster economic stability, growth and job creation;

- create diversified and competitive local rural economies; and

- build economically sustainable communities.

The roots of the CFP began in the early 1970's with the establishment of "local employment development" type programs such as the Local Employment Assistance Program (1973) and the Community Employment Strategy (1975) delivered by Employment and Immigration Canada. In the 1980's, assistance to local businesses was provided through two community-based programs: Local Economic Development Assistance (1980), and Local Employment Assistance and Development (1983). These program concepts were expanded in 1985 with the establishment of the Community Futures Program under the Canadian Jobs Strategy. The CFP was targeted to communities with 'chronic' or 'acute' labour market problems and designed to provide a suite of measures to assist communities in planning and developing local solutions to local problems.

In 1995, the program was transferred to IC and the RDAs. IC delivers its portion of the program through the Federal Economic Development Initiative for Northern Ontario (FedNor). In August 2009, responsibility for the CFP in southern Ontario was transferred to the Federal Economic Development Agency for Southern Ontario (FedDev) and consequentially the budget allocation for program delivery was split proportionally between southern and northern Ontario.

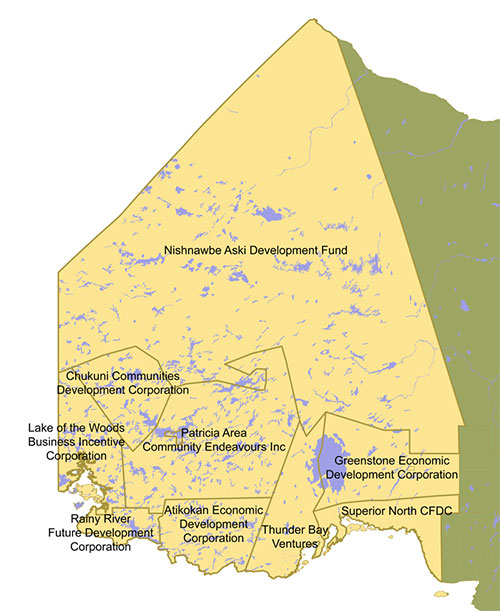

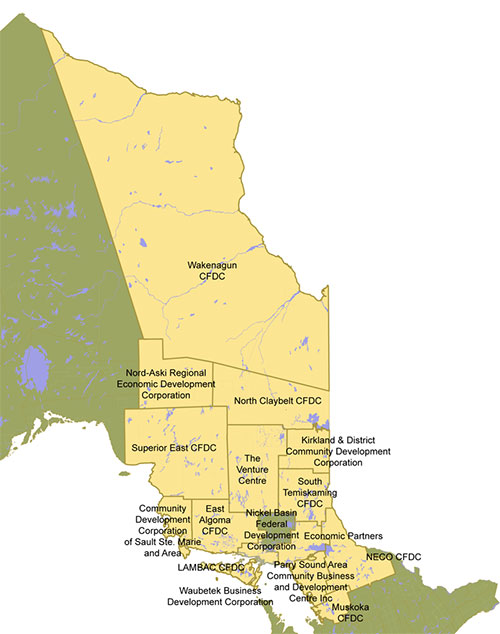

Under the current CFP, FedNor provides financial support through non-repayable contributions to 24 incorporated, non-profit and locally-based Community Futures Development Corporations (CFDCs) across Northern Ontario. These CFDCs are independent, arms-length organizations that employ professional staff and are governed by volunteer local boards of directors. For the distribution of CFDCs across Northern Ontario, please see Figure 1.

Figure 1: Community Futures Development Corporations in Northern Ontario

CFDCs Northeast Region - FedNor

These CFDCs are linked through three levels of networks:

- Community Futures Network of Canada—national organization

- Provincial and Territorial Networks—in Ontario this is the Ontario Association of Community Futures Development Corporations (OACFDC)

- Regional Networks—in Ontario there are four regional networks (i.e., Northwest, Northeast, Eastern and Western) which each provide similar support to their members with a tailored regional approach.

The provincial networks have dedicated offices and staff whereas the national and regional networks are run out of existing CFDC offices. These networks were established to provide regular collaboration among members, such as sharing products and services (e.g., online training), facilitating group purchases to achieve economies of scale, providing an advocacy function and facilitating communication among network members (e.g., newsletters and sharing best practices). They typically host regular meetings where group training is offered and where CFDCs can discuss common problems and share best practices. These network associations receive financial support through the CFP as well as revenue generated by membership dues, annual conferences and other activities.

CFP provides financial support to CFDCs to offset their operating costs (e.g., salaries, rent, utilities). These contributions allow CFDCs to provide support to small and medium-sized enterprises (SMEs), social enterprisesFootnote 1 and their local communities to meet the objectives of the program by engaging in four key activities:

- Fostering strategic community planning and socio-economic development by working with their communities to assess local problems, establish objectives, and plan and implement strategies to develop human capital, institutional and physical infrastructure, entrepreneurship, employment, and the economy;

- Providing business services by delivering a range of business counselling and information services to SMEs and Social Enterprises (e.g., on site libraries providing general business information, counselling on preparing a business plan, how to start or expand a business, marketing, or referral to another organization that can provide the assistance required);

- Providing access to capital for new and existing SMEs and Social Enterprises (e.g., loans, loan guarantees and equity investments)Footnote 2; and

- Supporting community-based projects and special initiatives in areas such as tourism, entrepreneurship, and opportunities for women, youth, and Aboriginals.

In addition to the funds provided by CFP to support operating costs, CFDCs receive funding from other FedNor programs to support activities that are incremental and complementary to those supported by CFP. For example, on an as needed basis, funds are provided to CFDCs by FedNor's Northern Ontario Development Program (NODP) to capitalize local Investment Funds. The investment funds are to be used by the CFDCs to provide access to capital for new and existing SMEs and Social Enterprises. These loans are repayable and provided at a minimum interest rate of two percent above prime. As loans are repaid, CFDCs re-invest the funds as new loans to SMEs and as a result the original funds provided by the Government continuously circulate through local communities.

NODP also provided funding over the evaluation period to CFDCs under other NODP prioritiesFootnote 3. One source of NODP funding for CFDCs was the Local Initiatives Contribution (LIC), which provided funding to undertake projects with community economic development objectives. Specifically, LIC projects support activities related to community economic development objectives that create short to medium-term measurable results for the communities and businesses in the region, such as working with communities to assess local problems, establish objectives, plan and implement strategies to develop human, institutional and physical infrastructure, entrepreneurship, employment and the economy. A breakdown of funding received by CFDCs from NODP is outlined in Table 1.

| NODP Funding Element | Total Value of Contributions to all CFDCs |

|---|---|

| Local Initiatives Contribution (LIC) | $5.6 M |

| Capitalization of CFDC investment funds | $19.8 M |

| Other NODP priorities | $7.1 M |

| Total NODP funding to CFDCs | $32.5M |

In addition to NODP, CFDCs may receive funding from FedNor under the Economic Development Initiative (EDI) to support business and economic development activities that encourage sustainable growth in Northern Ontario's Francophone communities. Over the period of the evaluation, four CFDCs received a total of $0.8 million through EDI.

Finally, CFDCs may receive additional funding from other sources such as the Government of Ontario to deliver provincial programs and municipal governments to provide local support in community planning and development.

1.2 Program Resources

Total funding for FedNor under CFP over the period covered by the evaluation was approximately $72.98 million. This funding includes both contributions to CFDCs for operating costs and the administrative costs for FedNor to deliver the program (e.g., salaries related to federal program officers to monitor the performance and compliance of CFDCs with respect to the terms and conditions of the contribution agreements, travel and other administrative costs). For a breakdown of funding for FedNor's component of the CFP over the 5-year evaluation period, refer to Table 2.

| 2008-09 Table note 1 | 2009-10 Table note 1 | 2010-11 | 2011-12 | 2012-13 | Total | |

|---|---|---|---|---|---|---|

| G&C | 21.56 | 21.96Table note 2 | 8.44 | 8.44 | 8.44 | 68.84 |

| O&MTable note 2 | 1.29 | 1.29 | 0.52 | 0.52 | 0.52 | 4.14 |

| Total | 22.85 | 23.25 | 8.96 | 8.96 | 8.96 | 72.98 |

1.3 Logic Model

A logic model is a visual representation that links a program's activities, outputs and outcomes; provides a systematic and visual method of illustrating the program theory; and shows the logic of how a program is expected to achieve its objectives. It also provides the basis for developing the performance measurement and evaluation strategies, including the evaluation matrix.

A logic model for the program was developed by a national CFP Performance Measurement Strategy Committee representing all of the CFP administering departments. This logic model is represented in Figure 2 and distinguishes between the activities and outputs of the funding departments that administer the program (including IC), and those of the Community Futures Organizations (e.g. CFDCs).

Figure 2: Community Futures Program Logic Model

2.0 Methodology

This section provides information on the evaluation strategy, approach, objectives and scope, the specific evaluation issues and questions that were addressed, the data collection methods, and data limitations for the evaluation.

2.1 Evaluation Strategy

A CFP Performance Measurement (PM) Strategy was developed by a national CFP PM Strategy Committee representing all of the administering departments. This PM Strategy was initially approved by all the CFP administering departments in October 2010 and includes the logic model contained in this document and an evaluation strategy. The committee subsequently approved a revised strategy in January 2013, upon which this evaluation is based.

The CFP evaluation strategy was developed based on the last CFP evaluation (2008) and lessons learned from that process. The administering departments agreed that a common national evaluation framework would be applied across departments, with flexibility to account for regional variations in programming if needed.

2.2 Evaluation Scope and Objectives

The objectives of the evaluation are to address the core issues of relevance and performance in accordance with the Directive on the Evaluation Function. The evaluation covers the period from April 2008 to March 2013.

2.3 Evaluation Questions

As set out in the CFP National Performance Measurement Strategy, all CFP evaluations were required to address the following questions of relevance and performance:

Relevance

- Is there a continued need for the CFP?

- To what extent are the objectives of the CFP aligned with:

- departmental strategic outcomes;

- federal priorities and strategies?

- To what extent are the objectives of the CFP aligned with the federal government's activities, roles and responsibilities? Does the CFP complement, duplicate or overlap other government programs or private services?

Performance

- What impact would the absence of CFP funding have had on the start-up, survival and growth of businesses, and on community strategic planning and development?

- To what extent have the immediate, intermediate and ultimate outcomes of the CFP been achieved?

- What are the barriers to achieving the CFP immediate, intermediate and ultimate outcomes and to what extent are these being mitigated?

- To what extent are the CFP's performance measurement and reporting structures effective in reporting on the achievement of the CFP outcomes?

- To what extent is the CFP efficient in the context of the results achieved? Is there a more cost effective way of achieving expected results?

- Are the loss rates of the CFDC loans acceptable and do the CFDCs carry an acceptable level of risk?

2.4 Evaluation Approach

This evaluation was based on the expected outcomes of the program as stated in the program's foundational documents and logic model. The evaluation was managed by IC's Audit and Evaluation Branch (AEB).

2.5 Data Collection Methods

Both qualitative and quantitative data were collected to provide multiple lines of evidence that were subsequently integrated in a triangulation of findings to support the conclusions and recommendations.

The data collection methods were set out in the CFP National Performance Measurement Strategy and included:

- Document review

- Literature review

- Interviews

- Survey of CFDC clients

- Data analysis

- Case studies

Document Review

The document review was conducted to gain an understanding of the CFP and insight into the performance of the program. Key documents reviewed included departmental reports, Treasury Board submissions, CFP documentation, policy bulletins, forms and templates, CFP reports, CFP audits, FedNor documentation, Speeches from the Throne and Federal Budgets.

Literature Review

The review of academic literature covered evaluation issues of both relevance and performance. In relation to relevance, the literature review focused on the continued need for the program, including: challenges specific to rural communities; the economic situation in Northern Ontario; the capacity for community economic development, business start-up and expansion; access to capital for SMEs; and, similar and complementary programming to CFP that is available.

The literature review also covered evaluation issues related to performance, including: the economic impact of CFP, best practices in fostering rural business development and expansion, and best practices in the support of community strategic planning and development activities.

Interviews

The objective of the interviews was to gather in-depth information for evaluation purposes, including views, explanations and factual information that address the evaluation questions. The interviews were designed to obtain qualitative feedback from a wide range of respondents. The interviews were primarily conducted by telephone.

A total of 72 interviewsFootnote 4 were conducted, including the following types of respondents:

- Program staff (10) ;

- Subject matter experts (3 academics and 1 consultant);

- Regional network and Provincial CF associations' representatives (3);

- Provincial government staff representatives (3);

- Other federal lending program representatives (1);

- CFDCs (24); and,

- Community partners (27)

Survey of CFDC Clients

AEB designed and administered a web-based survey of loan and counselling clients. Clients that had used the services of a CFDC in the past five years were invited to participate in the survey. The objective of the survey was to assess the client perspective on whether the program met their needs, how it assisted them, and what the results were, as well as their perspective on how the program could be improved.

Each CFDC produced a client list, which was to include contact information (e.g., phone numbers and e-mail addresses). The CFDCs identified a total of 4,184 unique clients served over the five year evaluation period. Based on this number of clients, a sample size of 352 was required to provide a confidence level of 95% with a margin of error of ± 5%.

Of the 4,184 unique clients identified, the CFDCs and AEB were able to identify 2,137 email addresses. Email invitations were sent to these clients, which resulted in 434 complete surveysFootnote 5 for a response rate of approximately 20%. This final sample size exceeded what was required for the sought confidence level and margin of error while providing representation from all CFDCs.

Data Analysis – FedNor/CFDC Data

Operational, performance monitoring, and financial data compiled by FedNor, as well as by the CFDCs was reviewed (e.g., CFDC quarterly reports, Annual Performance Reports and financial statement data). The objective of the data analysis was to document costs, activity levels, outputs and outcomes associated with the CFP.

Data Analysis – Statistics Canada Data

The objective of the data analysis was to assess the need for the program through comparisons of the CFDC profiles to the larger population of Ontario and assess the performance of program assisted businesses versus non-assisted businesses.

As part of the CFP National Performance Measurement Strategy, FedNor and the RDAs initiated Statistics Canada data runs to compare the performance of CFP assisted clients to matched non-assisted clients in the areas served by each CFDC. Comparisons were made on metrics such as employment growth, sales growth, and business survival rates. Three data runs were completed covering the years 2004 – 2009, 2005 – 2010, and 2006 – 2011.

Case Studies

The case studies were undertaken to answer evaluation questions pertaining to the achievement of immediate, intermediate and ultimate outcomes. In addition, they also provided:

- information regarding the operational environment of the CFDC sites and the process by which projects are undertaken;

- illustrative examples that support the program theory (i.e., not only whether outcomes have occurred, but how activities and outputs contribute to the intended outcomes); and

- challenges and lessons learned.

To obtain representative results from the cross case analysis, and to have a range of illustrative examples to support other lines of evidence, five CFDCs were selected for case studies. The following criteria were applied for case study selection: geographical representation (representing both regions of Northern Ontario), community economic development activities, First Nation population, level of unemployment, population density, strategic community planning, support to community-based projects and special initiatives, materiality (i.e., the dollar value of projects), and nature and extent of partnerships with other community organizations.

The five CFDCs selected based on these criteria were:

- Nishnawbe Aski Development Fund (main office in Thunder Bay, but CFDC is responsible for many small communities throughout Northwestern Ontario)

- East Algoma Community Futures Development Corporation, Blind River

- North Claybelt Community Futures Development Corporation, Kapuskasing

- Thunder Bay Ventures, Thunder Bay

- Greenstone Economic Development Corporation, Geraldton

In carrying-out the case studies, the following activities were undertaken:

- document review (e.g., community strategic plan);

- review of program data provided by the CFDC (e.g., loan portfolio and community economic development projects);

- review of economic data obtained through Statistics Canada;

- interviews with the staff and board members of the CFDC;

- interviews with community representatives;

- visits with loan and counselling clients; and

- visits with community economic development partners.

2.6 Limitations

The following were limitations of the methodology:

- Socio-economic data on CFDC service areas: Developing socio-economic profiles of CFDC service areas requires custom tabulations. At the time of this study, the custom tabulations using 2011 Census Data for CFDC service areas were not yet available. To mitigate this limitation, the evaluation looked at the data for the 12 Census Divisions that are considered to comprise Northern Ontario.

- Availability of client contact information: Approximately half of the clients identified for the evaluation period had no email address available, thereby limiting potential respondents to the survey. To mitigate for this limitation, for under-represented CFDCs, clients with telephone contact information and no email address were contacted by phone to solicit email addresses and to encourage them to participate in the survey.

- Aboriginal representation in client survey: The representation of identified Aboriginal target group clients in the client survey was significantly lower than the population (8% vs. 14%). The CFDCs with high Aboriginal client bases were also the CFDCs that were under-represented overall. Again to mitigate for this limitation, for under-represented CFDCs, clients with telephone contact information and no email address were contacted by phone to solicit email addresses and to encourage them to participate in the survey.

3.0 Findings

3.1 Relevance

3.1.1 Is there a continued need for the CFP?

Key Finding: The economic situation in Northern Ontario and the barriers faced by SMEs in the region suggests a continued need for a program such as CFP. There appears to be a consistent need for access to capital and business services across CFDCs while the need for federal involvement in community strategic planning and economic development varies among CFDCs.

Northern Ontario covers a land area of over 800,000 square kilometres, which represents nearly 90% of the province's land area, yet only 6% of its total population at 803,866.Footnote 6 Northern Ontario's rural population comprises 31.4% of the total northern population, whereas in Southern Ontario only 14.1% of the population lives in a rural area.Footnote 7 Rural areas face particular challenges related to encouraging entrepreneurial growth as these communities are often located far away from urban centres; thereby increasing transportation and telecommunications-related costs and decreasing access to markets and opportunities to achieve economies of scale. Footnote 8

Many northern communities also remain reliant on primary industry sectors such as mining and forestry, which accounted for close to 6.3% of Northern Ontario's total employment in 2011, compared to only 0.5% for the Province. This dependence leaves these areas particularly vulnerable to slowing market demand or closures.Footnote 9 Between 1988 and 2011, employment in Northern Ontario fluctuated greatly in comparison to Ontario where employment increased steadily between 1993 and 2008.Footnote 10 In the past, on average, Northern Ontario's unemployment rate had been two percentage points higher than Ontario's. In recent years this gap has decreased and in 2012 the rate for Northern Ontario (7.2%) was lower than Ontario's rate of 7.8%.Footnote 11

While the employment situation in Northern Ontario has improved over the last decade, average income levels still lag behind the rest of Ontario and Canada. Table 3 displays the income data for the 12 Census Divisions considered to comprise Northern Ontario. The figures show that the average income of Northern Ontario residents was 10% lower than Ontario and 6% lower than Canada. The situation was more extreme in certain Census Division areas such as Manitoulin where the average income was close to 30% lower than that for Ontario.

| Region | Average Income | % Variance from ON | % Variance from Canada |

|---|---|---|---|

| Algoma | $36,406 | −14% | −10% |

| Cochrane | $39,446 | −7% | −3% |

| Greater Sudbury | $40,874 | −3% | 1% |

| Kenora | $37,515 | −11% | −8% |

| Manitoulin | $29,932 | −29% | −26% |

| Muskoka | $36,965 | −13% | −9% |

| Nipissing | $37,139 | −12% | −9% |

| Parry Sound | $35,024 | −17% | −14% |

| Rainy River | $36,867 | −13% | −9% |

| Sudbury | $36,273 | −14% | −11% |

| Thunder Bay | $38,856 | −8% | −4% |

| Timiskaming | $34,481 | −18% | −15% |

| Northern ON | $38,027 | −10% | −6% |

| Ontario | $42,264 | ||

| Canada | $40,650 | ||

| Source: Statistics Canada, National Household Survey, 2011 | |||

Literature suggests that entrepreneurship can help encourage overall economic growth. Cumming, Johan and Zhang conclude that because entrepreneurship has long been associated with having a positive impact on economic growth, governments have often put policies and programs in place to encourage its growth.Footnote 12 Encouraging entrepreneurial growth is also one way governments can try to improve economic conditions in specific regions of the country that may be facing stagnant or declining economic growth or lower income levels.

Siemens further outlines some of the challenges faced by rural businesses, specifically that they are often required to "operate without standard business infrastructure such as banks, broadband Internet and a fully developed transportation network, resulting in higher costs and time commitments than may be faced by urban enterprises."Footnote 13

Access to capital and business services

Literature suggests that a gap in the debt financing market exists for certain types of businesses in Canada. Specifically, a 2013 Industry Canada study based on surveys conducted in 2000, 2001, 2004, 2007, 2009 and 2010 concludes that, "young businesses experienced greater difficulties accessing debt financing than older firms. This is likely because they have shorter track records, younger and less experienced management teams and higher default risks…these findings support the theory that partial gaps in financing for specific types of businesses exist, namely among Canada's smallest businesses, youngest businesses and most R&D intensive businesses".Footnote 14 The severity of the situation in Northern Ontario is revealed in the 2011 Industry Canada Survey on Financing and Growth of Small and Medium Enterprises. The survey found that 22.5% of Northern Ontario SMEs identified "obtaining financing" as a serious problem for the growth of their business, compared to 17.7% of SMEs in Ontario and 16.8% of those across Canada.

The difficulty accessing loans from traditional lenders was also evidenced in case studies where most loan clients and CFDC staff spoke of the need for the CFP since it was difficult to access capital as banks were rigid in applying their lending criteria. For example, respondents of all types in four of the five case studies indicated that local banks were unwilling to provide loans to certain sectors that were considered to be in a downturn as they were deemed too risky; most notably the forestry sector. In two case studies, CFDC staff and loan clients mentioned that in many cases local banks were interested in helping local businesses with loans, but were unable to provide the assistance required because applications were sent to head office for final approval and subsequently declined. The case studies demonstrated that there was a need for a program in Northern Ontario such as the CFP where loan decisions were made locally by loan officers who understood the community's economic context.

In the evaluation survey of clients, 75% of clients seeking financing from a CFDC to start a business, and 70% of those seeking financing to maintain or expand a business, had previously sought financing through other sources. Of the clients that previously sought financing from other sources, 55% of those starting a business, and 66% of those seeking a loan to maintain or expand a business, were unsuccessful in obtaining financing from another source.

Some interviewees suggested that chartered banks continue to close small rural branches and that access to business credit is extremely tight, particularly in certain industry sectors such as forestry. Furthermore, CFDC managers and board members suggested that the absence of CFP funding would have a devastating impact on business start-ups, survival and growth, with many explicitly stating that a significant number of businesses would not exist without CFP.

Table 4 outlines the perceived community need for the key business services provided by CFDCs from the perspective of clients based on the 2013 evaluation survey of clients. The first four services detailed comprise the business servicesFootnote 15 provided by CFDCs. While the table shows that the key need is for the provision of business financing, 91% of all loan clients believe that their communities have need for each of the business services CFDCs provide.

| Type of Service | Extent to which there a need in the community for CFDC Services | |

|---|---|---|

| Great Extent | Some extent | |

| Provision of business information | 62% | 30% |

| Referral services | 59% | 30% |

| Provision of business counselling | 63% | 27% |

| Provision of training courses or seminars | 62% | 29% |

| Provision of business financing | 74% | 17% |

| Source: 2013 Survey of CFDC clients | ||

It should be noted that IC staff suggested that alternate sources of business services were often available in larger urban communities, lessening the need for CFDCs to provide this type of service in those areas.

Community Economic Development and Strategic Planning

Community partners interviewed all believed in the need for community strategic planning and community economic development and suggested that there is a continued need for the services provided by the CFDCs. A number of them suggested that this is most critical in small/rural communities where the capacity does not exist in the community.

According to interviews with CFDC managers and board members as well as IC staff, the need for CFDC involvement in local community economic development and strategic planning activities varied among CFDCs and was largely dependent on the community's capacity to undertake these activities (e.g., ranging from CFDCs playing no role in strategic planning in certain locations to leading the process in others). In particular, larger populations often had sufficient capacity while smaller rural and remote communities often had little or no capacity. IC staff suggested that the flexibility the CFP provides, allows CFDCs to tailor their activities and resources toward activities that will have the greatest impact on their communities. This was supported in the case studies where one CFDC in an urban area played no role in its community's strategic plan and another CFDC that had historically been very active in its region's strategic planning exercises, was now taking on a secondary role due to resurgence in the municipality's resources and capacity to lead the activity. Due to the flexibility the CFP provides, this particular CFDC was shifting its focus to loan activity and business counselling and outreach activities, such as business seminars, to adapt to the needs of its community.

3.1.2 To what extent are the objectives of the CFP aligned with: i) departmental strategic outcomes; ii) federal priorities and strategies?

Key Finding: The CFP aligns with Government priorities to support community and economic development in rural Canada through a community-based approach to supporting small businesses. It is also aligned with Industry Canada's strategic outcomes and activities related to community economic development and developing competitive Canadian businesses and communities.

The CFP's objectives of fostering economic stability, growth and job creation; creating diversified and competitive local rural economies; and, building economically sustainable communities are consistent with federal priorities. Over the period of the evaluation, the Government has continually stated the priority it places on ensuring competitive local rural economies and building economically sustainable communities through a community-based approach to supporting small businesses. Of note, the 2010 Budget provided additional ongoing funding for CFP, demonstrating the Government's long-term commitment to developing rural economies. Subsequent Budgets continued to reiterate the Government's focus on regional economic development and its support to rural communities. Further, recent statements by the Minister for FedNor show continued focus on supporting small businesses to help further develop communities in Northern Ontario.

Table 5 contains some excerpts from a recent press release and from recent Budgets and Speeches from the Throne that demonstrate the importance the Government places on rural economic development.

| Source | Quotations | Analysis |

|---|---|---|

Press Release November 22, 2013 | "The Honourable Greg Rickford, Minister of State for Science and Technology, and FedNor, and Minister responsible for the Ring of Fire, today announced a Government of Canada investment to support small business, youth initiatives, innovation, and attract private sector investment to Northern Ontario. 'Our government is proud to support initiatives that create jobs and help Northern Ontario communities grow through economic development opportunities,' said Minister Rickford." | Demonstrates Government's current priority to support the small business sector and develop communities in Northern Ontario. |

SFT 2013 | "Creating jobs and securing economic growth is and will remain our Government's top priority….Canadians know that businesses create jobs." "Following our Government's return to balanced budgets, it will look at ways to provide further tax relief to job-creating small businesses". | Show's Government's continued support to small businesses and impact businesses have on job growth. |

Budget 2013 | Economic Action Plan 2013 outlined a priority of "Supporting Families and Communities by expanding opportunities for Canadians to succeed and enjoy a high quality of life." "The Government's number one priority is creating jobs. In recognition of the important role that small businesses play as job creators in the Canadian economy, Economic Action Plan 2013 proposes to expand and extend for one year the temporary Hiring Credit for Small Business." | Shows Government's continued commitment to support communities. Demonstrates importance of small business sector and the impact it has on the Canadian economy. |

Budget 2011 | "The health, vibrancy and diversity of Canada's communities are central to Canada's strength. Supporting urban and rural communities and celebrating our culture will help keep Canada one of the best places in the world to live". | Demonstrates the Government's continued priority to support rural and urban communities. |

SFT 2011 | "Local communities are best placed to overcome their unique challenges, but government can help create the conditions for these communities—and the industries that sustain them—to succeed". | Reiterates the Government's commitment to a community-based approach to addressing local economic challenges. |

Budget 2010 | "Budget 2010 renews funding for a number of programs, including: | The Government's increased funding for CFP shows the Government's continued support of CFP to promote community and economic development in rural Canada. |

Budget 2009 | The Budget established funding for new RDAs in Southern Ontario and the North. | Shows the Government's continued support to regional economic development. |

Support for the CFP also aligns with IC's priorities under the Community Economic Development Program Activity of Industry Canada's Program Alignment Architecture. The main goal of this Program Activity is to strengthen the Northern Ontario economy by providing financial support, through contribution agreements, for economic and community development projects led by the private, not-for-profit and public sectors. This focus is consistent with CFP's objectives of fostering economic stability, growth and job creation; creating diversified and competitive local rural economies; and, building economically sustainable communities. This Program Activity contributes to IC's Strategic Outcome 3: "Canadian businesses and communities are competitive", which is also consistent with CFP's objectives.

3.1.3 To what extent are the objectives of the CFP aligned with the federal government's activities, roles and responsibilities? Does the CFP complement, duplicate or overlap other government programs or private services?

Key Finding: CFP support to CFDCs is consistent with federal roles and responsibilities to support regional economic development in Ontario with a focus on SMEs and the development of entrepreneurial talent. While there are many players in regional economic development in Northern Ontario, most services provided by CFDCs are complementary to those provided by other parties. Where there is potential overlap, CFDCs coordinate with partners to minimize actual duplication.

The literature suggests that the federal, provincial and municipal governments all have roles to play in community economic development. For example, Conteh has concluded that: "In Canada, although the Constitution grants de-jure responsibility for economic development policy to provincial governments, in practice, this responsibility is shared between the federal centre (in Ottawa) and its constituent units in the various provincial capitals. Moreover, although municipalities are "creatures" of the provinces in Canada, in reality, they have been assuming greater policy responsibility and attendant policy autonomy and discretion, including the governance of local economic development"Footnote 16.

Within the federal domain, the objectives of the CFP fall under the Department of Industry Act of 1995. According to this legislation, the powers, duties and functions of the Minister of Industry extend to matters relating to "small businesses"Footnote 17 and the Department has responsibilities related to regional economic development in OntarioFootnote 18. The Act further stipulates that the Minister, in exercising his powers relating to regional economic development, "focus on small and medium sized enterprises and the development of entrepreneurial talentFootnote 19". Finally, the Act states that the Minister may provide and coordinate services promoting regional economic development in Ontario and initiate, recommend, coordinate, direct, promote and implement programs and projects in relation to regional economic development in OntarioFootnote 20.

There are many parties that play a role in regional economic development in rural communities in Northern Ontario or that provide loans to small businesses. This includes federal, provincial and municipal/community level organizations. NODP invested $32.5 million over the evaluation period into CFDCs in order to support the NODP objectives of encouraging economic growth, diversification, job creation and self-reliant communities in Northern Ontario, which is similar to the objectives of the CFP. The NODP has been the main funding source for the capitalization of CFDC Investment Funds and has provided the bulk of funds to CFDCs for community based projects and special initiatives. This is due to the fact that there is no set funding for either activity. Without NODP, it would have been more difficult for CFDCs to deliver their key activities related to community economic development and business financing. NODP funding is complementary to CFP funding in that CFP provides operating funds for CFDCs, but typically does not provide funds for capitalization of the investment fund or for the implementation of community based projects and special initiatives due to program budget constraints.

There are also two key federal sources under which SMEs in Northern Ontario may receive access to capital, namely loans provided by the Business Development Bank of Canada (BDC) and the Canada Small Business Financing Program (CSBFP) delivered by Industry Canada.The BDC offers loans and business consulting services to SMEs, which are two of the four main activities of the CFP. The main difference between the two programs is that the CFP has a visible presence in Northern Ontario, whereas the BDC's presence is limited (there are six business centres in Northern Ontario) especially in rural communities. In terms of counselling services, BDC provides such services on a fee basis, whereas CFDCs provide these services at no charge. In addition, interviewees indicated that BDC tends to deal with larger dollar value loans than the CFDCs and are more risk-averse. Finally, about half of the CFDCs that were interviewed indicated that they had a referral process in place with BDC such that they would refer clients to the BDC that they thought would meet the BDC eligibility criteria. The different eligibility criteria and the referral process would seem to indicate that there is little overlap between BDC and the CFP, and that the two programs are complementary for the most part.

The objective of CSBFP is to facilitate access to asset-based debt financing for the establishment, expansion, modernization and improvement of small businesses. It does this by sharing the financial risk of lending to small businesses among the borrowers, lenders and the government. The Government pays lenders up to 85% of eligible losses incurred, after lenders' cost-recovery efforts, on loans that have defaulted. In return, the borrower pays an up-front registration fee of two percent of the amount financed and an annual fee of 1.25% of the outstanding loan amount. Commercial lenders are responsible for credit decisions, subject to eligibility requirements as specified by the Government of Canada. The objectives of the CFP and the CSBFP are very similar, as both try to increase SME's access to business financing.

Most interviewees indicated that the presence of commercial lenders is limited in Northern Ontario and when they are present, they often do not provide significant business financing. It should be noted that over 70% of CFDC loan recipients reported through the client survey that they had sought financing from another source prior to applying to the CFDC. For these clients, over 85% of them had sought financing through a financial institution. As these financial institutions would have been eligible to offer CSBFP loans, this would seem to indicate that most CFDC loan clients were not able to access a CSBFP loan either because the financial institution was not familiar with the program or the clients did not qualify for a CSBFP loan.

CFDC's may also receive funding from provincial ministries and municipal/community organizations to provide certain services to their local communities. At the municipal level, municipal governments and local chambers of commerce may have some capacity and level of involvement in community strategic planning and development. In other cases, municipalities provide funding to CFDCs to undertake such activities on their behalf. Provincially, there are also a number of programs that complement and potentially overlap with the CFP in serving communities in Northern Ontario. These include:

- The Small Business Enterprise Centres (SBECs) are funded by the Ontario Government and provides entrepreneurs with consulting/counselling services and tools to start or grow a business. While there is overlap with the CFP business line of providing business counselling, SBECs do not provide loans and their visibility and reach is less in some of the smaller remote communities. Specifically, there are nine SBECs located in Northern Ontario compared to twenty-four CFDC offices and in only five cases is there a CFDC and SBEC located in the same community (Bracebridge, Thunder Bay, North Bay, Kenora and Haileybury).

- The Northern Ontario Heritage Fund Corporation (NOHFC), which is a Crown Corporation under the Ontario Government, invests in northern businesses and municipalities through five funding programs that provide conditional contributions, forgivable performance loans, incentive term loans and loan guarantees designed to help municipalities, entrepreneurs and businesses build, expand and grow. Since 2003, NOHFC has committed more than $890 million to about 5,800 projects in Northern OntarioFootnote 21.

- The Rural Economic Development (RED) Program provides funding of $4.5 million per year over three years to help rural communities remove barriers to community development, promote economic growth planning processes and contribute to economic competitiveness. RED projects are cost shared between the province and communities. Since 2003, the Ontario Government has invested more than $167 million in 418 RED projects.Footnote 22

- The Ontario Self-Employment Benefit (OSEB) provides unemployed people who are, or have recently been eligible for Employment Insurance with income and entrepreneurial support while they develop and start their business. A number of CFDCs deliver the OSEB on behalf of the Province.

A large majority of interviewees suggested that CFDCs play a complementary role to other programs with little overlap or duplication of services with other federal and provincial programs. This is partly due to different eligibility criteria of the programs and because CFDCs are the closest resource in many communities. In addition, CFDCs have the flexibility to tailor their offerings to address gaps in the communities they serve. Finally, many respondents indicated that there was a high level of coordination among the programs, suggesting that the CFDCs often work with other service providers to ensure there is no overlap, to agree on roles and to provide mutual referral services to help communities develop and implement local solutions to local problems.

3.2 Performance

3.2.1 What impact would the absence of CFP funding have had on the start-up, survival and growth of businesses, and on community strategic planning and development?

Key finding: Evidence suggests that the absence of CFP funding would have a direct and negative impact on start-up, survival and growth of businesses in Northern Ontario. The impact on community strategic planning and economic development in the absence of CFP funding would be mixed depending on the capacity of the community and the role the CFDC currently plays in this area.

Evidence from the evaluation suggests that the program has an incremental impact on the businesses and communities that they serve. The Statistics Canada custom tabulations comparing CFP-assisted firms to non-assisted firms show that CFP assisted firms were more successful at achieving job growth, had higher rates of business survival and showed greater sales growth as compared to non CFP-assisted firms. See section 3.2.2 for further details.

The evaluation client survey provides an indication that the absence of CFP would have a negative impact on loan clients and their ability to access capital. Specifically, 74% of loan clients who received financing to start a business indicated that it was somewhat or very unlikely that they would have been able to start their business without the CFDC financing they received. In addition, for clients who sought a loan to maintain or expand their business, 71% said it was somewhat or very unlikely that they could have done so without CFDC financing. The impact on businesses is further reflected in the context of the client survey where 54% of applicants who were rejected for a CFDC loan, reported that they were unable to start the business proposed.

In addition, CFDC staff and loan clients at two CFDCs involved in the case studies indicated that the program was having a significant impact on businesses in their communities and what set them apart from traditional lenders was the flexibility that they could offer clients regarding loan repayment schedules. For instance, respondents pointed to examples where CFDCs had worked with seasonal businesses, those waiting for a payment from a large client, or those communities only accessible by winter road to adjust loan repayments accordingly. If action was not taken, respondents suggested that these businesses would have likely had to go out of business. Respondents in these two case studies further suggested that it was this flexibility, coupled with the knowledge of the local economy and challenges within their region that was allowing the CFDC to contribute to the survival of many businesses.

As part of the evaluation, interviewees were asked to consider the impact the absence of CFP funding would have had on businesses and economic development in their communities. There was broad agreement across CFDC representatives and community partners interviewed that the absence of the CFP would negatively affect businesses in their communities at all stages of development, including start-up, growth and survival. The majority of interviewees explicitly stated that a number of businesses would not exist without the CFP. On the other side, experts and provincial representatives were split regarding the impact in the absence of CFP. Of the two experts who offered an opinion, one felt that there are enough other programs operating and that clients would adapt, while the other described the situation as a "disaster" since the absence of CFP would accelerate issues such as out-migration and urbanization. In addition, one provincial government respondent indicated that the absence of CFP would impact the growth of businesses in the region because CFDC's are involved in community planning, while another provincial government respondent believed that the number of provincial Small Business Enterprise Centres would increase if CFP funding was absent.

One method of ensuring incrementality of CFP funding was identified in the case studies whereby, several CFDCs noted that they require refusal letters from commercial banks or other lenders before approving a CFP loan.

The impact that the absence of CFP funding would have on community economic development and community strategic planning was less clear. With respect to the impact on community economic development activities, a few CFDC representatives felt that these activities would be negatively affected, although a similar proportion specifically stated that they did not believe there would be a large negative impact. The discrepancy in responses could be due in large part to the role the CFDC plays in various communities – varying widely from being heavily involved in community economic development and strategic planning initiatives to very limited involvement in municipalities that have the capacity to undertake these roles. However, for their part, all community economic development partner respondents felt that an absence of CFP would negatively impact their community's overall economic development.

3.2.2 To what extent have the immediate, intermediate and ultimate outcomes of the CFP been achieved?

Key Finding: Overall, evidence suggests that the CFP is achieving its intended immediate and intermediate outcomes; however, some outcomes are partially attributable to NODP. CFDCs' primary focus is on providing access to capital and business services, and therefore it shows the greatest impacts through these activities. Ultimate outcomes are difficult to attribute directly to CFP; however, data collected from Statistics Canada and CFP clients suggest that the CFP is contributing to job creation and economically sustainable local rural economies.

This section presents an analysis of the success of CFP in achieving the intended outcomes of the program as depicted in the logic model contained in section 1.3. The analysis is divided into three sections, the first section examines immediate and intermediate outcomes as a result of providing services to SMEs and Social Enterprises (e.g., loans and business counselling), the second section looks at immediate and intermediate outcomes as a result of support for community-level planning and projects, and the third section examines ultimate outcomes resulting from both the provision of services to SMEs and Social Enterprises and from activities in support of community-level planning and projects.

Business Related Services to SMEs and Social Enterprises - Immediate and Intermediate Outcomes

CFDCs provide both financing and business services to SMEs and Social Enterprises under CFP. Over the evaluation period, the 24 CFDCs in Northern Ontario provided 2,200 loans totalling $109 million (roughly $908,000 on average per CFDC per year or $50,000 per loan). Over the same period, they handled 85,931 general inquiries and conducted 12,125 in-depth counselling sessions. FedNor staff, CFDC board members and CFDC staff interviewed all indicated that access to capital and business services were the primary focus of CFDCs.

All five case studies demonstrated that the greatest impact the CFDCs were having was on increasing access to capital. This was substantiated through interviews with loan clients, community partners and CFDC staff, as well as through CFDC prepared reports submitted to FedNor (e.g., Annual Performance Reports). Common responses from loan clients were that "I couldn't have survived without the loan I received" or that the "banks wouldn't touch us", demonstrating an impact on the CFP's immediate outcome – improved access to capital.

In terms of financing, the loans are expected to improve access to capital and leverage additional capitalFootnote 23. The evaluation client survey showed that 41% of clients surveyed who received a loan from a CFDC to start a business and 26% for clients who received a loan to maintain or expand a business, reported that the funding enabled them to obtain additional funding from other sources. Over the evaluation period, CFDCs reported that the $109 million they lent out leveraged $219 million ($59 million in owners' equity and $160 million in third party contributions)Footnote 24.

In terms of business services provided to clients, Table 6 provides details on the distribution of services received and satisfaction levels.

| Type of Business Service Received from CFDC | Proportion of Clients who Received Service | Proportion of Clients who were Very Satisfied with Level of Service | Proportion of Clients who were Somewhat Satisfied with Level of Service |

|---|---|---|---|

| obtained business information | 74% | 71% | 22% |

| received at least one referral to another organization | 49% | 61% | 32% |

| received business counseling | 60% | 70% | 23% |

| received training through a course or seminar | 27% | 59% | 38% |

| Source: 2013 Evaluation Survey of CFDC Clients | |||

The table shows that the majority of CFDC clients received general business information and specific business counselling while close to half received at least one referral to another organization and approximately a quarter received some training from a CFDC. As can be seen, 93-97% of clients were very or somewhat satisfied with the business information, business counseling or training they received. It should be noted that the table includes loan clients who may have only received financing and not obtained any other CFDC service. However, in the case studies, it became evident that many loan clients who initially suggested that they had not received any business services in addition to their financing upon further probing revealed that they had in fact received significant counselling through the loan process. This was further reflected in the interviews of CFDCs where staff indicated that they often provide guidance to loan clients to develop their business plans and strengthen their proposals to the point where the case is strong enough to support a loan.

The immediate outcomes from the provision of business financing and business services are expected to lead to increased entrepreneurship, improved business practices, and strengthened and expanded businesses. The performance indicator in the CFP National Performance Measurement Strategy for increased entrepreneurship is the number of new business start-ups that were created through CFP financing. Over the evaluation period, the 24 CFDCs provided loans to 896 business start-upsFootnote 25.

In terms of strengthened business practices and strengthened businesses, the case studies revealed that certain skill sets were lacking among entrepreneurs in some communities, particularly those related to bookkeeping, accounting and human resources. Through interviews with loan clients, community partners and CFDC staff, it was evident in three of the five case studies that one-on-one counselling and/or training courses and seminars provided by the CFDCs were having an impact on improved business practices and entrepreneurial skills in the community. In addition, Table 7 shows the perceived level of impact on clients who indicated that they received counselling services from a CFDC. The table shows that that 64% of surveyed clients who had received counselling services believed that the CFDC support strengthened their business practices, 44% believed it increased their sales and 45% believed it increased their profitability to at least some extent.

| Perceived Level of Impact %/Cumulative% | ||||

|---|---|---|---|---|

| Type of Impact | Great Extent | Some Extent | Little Extent | No Extent |

| Strengthened business practices | 26% | 38% | 15% | 21% |

| Increased business sales | 13% | 31% | 25% | 31% |

| Increased business profitability | 13% | 32% | 14% | 41% |

| Source: 2013 Evaluation Survey of CFDC Clients | ||||

Further, the Statistics Canada analysis of CFP-assisted clients to a comparable group of non-assisted clients showed that sales for CFP-assisted firms climbed from $224.8 million in 2005 to $376.2 million in 2010Footnote 26. This represents an average increase of 10.8% per year, which is far more than the 3.6% per year from non-assisted firms. Sales for the comparable group increased from $7.1 billion in 2005 to $8.5 billion in 2010Footnote 27.

In relation to business expansion, CFDC data shows that over the evaluation period, CFDCs provided loans to 562 businesses in the expansion phase of the business cycle as well as providing business services to 374 businesses that were seeking to expandFootnote 28. Further, the evaluation client survey showed that for clients who received a CFDC loan to maintain or expand their business, 71% said that it was somewhat or very unlikely that they could have done so without the CFDC financing.

Support for Community-Level Planning and Projects - Immediate and Intermediate Outcomes

Support of community-level planning and economic development projects is expected to lead to the immediate outcomes of strengthened community planning and more effective implementation of community economic development through projects, partnerships and other community development initiatives.

Data on CFDC community-level activities was available through the Annual Performance Reports (APRs), covering the calendar years 2008 through 2012. During this period, the 24 CFDCs in Northern Ontario worked with 304 partners in developing or updating 56 strategic development plans.

Several CFDCs interviewed suggested that strategic planning was the activity they focused on least, which would be consistent with the limited number of plans in which CFDCs participated. This was also highlighted in the case studies where the impact the five CFDCs were having on strategic planning varied from acting as a resource at the table to not having any impact on the community's strategic plan. One CFDC, located in an urban centre noted that it was not influential in the city's strategic planning process and it was limited to playing a role in the development of specific organizational strategic plans (most often those with limited capacity such as local non-profit organizations). Three other CFDCs were used mainly as a resource to link stakeholders and provide a broader regional perspective to the strategic planning process.

Finally, one CFDC responsible for a large geographical area made up of a large number of small remote communities was not able to be directly involved in strategic planning due to proximity, remoteness and number of communities, but was having an impact by providing communities with a strategic planning toolkit. Providing the tools to these communities could also be viewed as building community capacity and empowering these communities to take ownership of the strategic planning process, their plans and their implementation.

Over the calendar years from 2008 to 2012, the CFDCs reported that they worked with 10,490 partners on 3,372 community economic development projects with a value of $198 million. CFDCs reported that they contributed $9.4 million to these projects. Interviews of CFDC board and staff members corroborated that community economic development activities were largely funded by the NODP's LIC under which the CFDCs received $5.6 million over the evaluation period. LIC projects support activities related to community economic development objectives that create short to medium-term measurable results for the communities and businesses in the region, such as working with communities to assess local problems, establish objectives, plan and implement strategies to develop human, institutional and physical infrastructure, entrepreneurship, employment and the economy.

The immediate community level outcomes are expected to lead to strengthened community capacity for socio-economic development. Of the CFDC clients surveyed, 93% believed that the CFDC had an impact on the community capacity with 46% of them suggesting the extent of the impact was great. While most community economic development partners and subject matter experts interviewed did not comment on the impact on community capacity, all those that did suggested that the program had a positive impact. In addition, three of the five CFDCs involved in the case studies demonstrated that they were having an impact on business practices and entrepreneurial skills by delivering workshops or information sessions related to book keeping and financial statements. One CFDC also worked in partnership with the local college to deliver a 6-week workshop to entrepreneurs on website design.

Ultimate Outcomes

The intermediate outcomes of CFP are expected to lead to the ultimate outcomes of: 1) economic stability, growth and job creation; 2) diversified and competitive local rural economies; and, 3) economically sustainable communities. Ultimate outcomes are difficult to attribute directly to CFP, as a number of additional factors can influence these outcomes. Nonetheless, data collected from Statistics Canada and CFP clients suggest that the CFP is contributing to these outcomes.

Consistent with the PMS, Statistics Canada data is used to demonstrate how the CFP is contributing to all of the ultimate outcomes. Specifically, Statistics Canada data analysis of CFP-assisted firms to a comparison group of non CFP-assisted firms showed employment growth in CFP assisted firms grew by an average of 7.7% per year over the five-year period (2005-2010) compared to 3.1% for the comparable group. The analysis also showed a favourable comparison of business survival rates which represents the number of firms that have entered the market and are still in business over a given period of time. The business survival rate for all CFP-assisted firms born between 2000 and 2005 was 84% after the crucial fifth year following start-up, compared with 64% for comparable firms started in the same time period. This represents a variation in the five-year business survival rate of 20 percentage points between CFP-assisted firms and the comparable groupFootnote 29.

Data from the client survey, displayed in Table 8, shows that CFDC clients perceive that the CFDCs have a significant impact on all of the CFP ultimate outcomes. Specifically, over 80% of those surveyed believed that the CFDC activities had an impact on their community's economic growth, job creation, diversification and competitiveness, economic sustainability and business survival to a great or some extent.

| Perceived Level of Impact %/Cumulative% | ||||

|---|---|---|---|---|

| Type of Impact | Great Extent | Some Extent | Little Extent | No Extent |

| Economic growth | 45% | 40% | 9% | 6% |

| Job creation | 42% | 41% | 11% | 6% |

| Diversification and competitiveness | 40% | 41% | 10% | 9% |

| Economic sustainability | 42% | 40% | 11% | 7% |

| Survival of businesses | 51% | 30% | 11% | 8% |

| Source: 2013 Evaluation Survey of CFDC Clients | ||||

3.2.3 What are the barriers to achieving the CFP immediate, intermediate and ultimate outcomes and to what extent are these being mitigated?

Key Finding: While the CFP is largely achieving its expected outcomes, a number of barriers to its success were identified by interviewees, including the increased pressure on CFDC operating budgets and large CFDC service areas.

CFDC staff, IC program staff and community partners all suggested that the biggest obstacle hindering the success of the CFP is that funding to CFDCs has not increased at the same rate as their costs. Specifically, interviewees indicated that operating costs to maintain CFDC offices have increased over timeFootnote 30 without a corresponding contribution increase to CFDCs. CFDCs indicate that with costs rising (e.g., salaries, rent, utilities, and travel costs), there is less discretionary funds to contribute to the community economic development and strategic initiatives business lines.

The large geographical area that many CFDCs serve was also identified as a barrier to achieving CFP outcomes. In particular, large geographic areas put a strain on CFDC operating budgets due to rising travel costs; leaving less discretionary funding for CFDC investments toward strategic initiatives and community economic development activities. FedNor does provide additional funding for five CFDCs to compensate for remote service areas and corresponding travel costs, but this continues to be a challenge for many CFDCs. In addition, large geographic areas comprised of many small communities pose challenges for CFDCs in terms of having a local presence and becoming an integral part of the community, which can be particularly challenging with staff of two to four employees. To mitigate, CFDCs are taking advantage of teleconferencing software when possible and bundling trips to reduce travel costs. A CFDC that was examined in the context of the case studies also identified a recent costing exercise, which resulted in the CFDC leasing a car for travel as opposed to paying staff mileage rates as one strategy to reduce travel costs.

3.2.4 To what extent are the CFP's performance measurement and reporting structures effective in reporting on the achievement of the CFP outcomes?

Key Finding: CFP performance measurement has improved significantly since the last evaluation. The development and implementation of the National CFP Performance Measurement Strategy is assisting FedNor in assessing and reporting on the achievement of program outcomes. As well, the introduction of the CFDC Performance Report should improve the reporting of results on all four CFDC business lines. However, there are still improvements that could be made to performance measurement for the CFP.

Historically, CFDCs reporting tools have included quarterly reports, annual performance reports and business plans. The quarterly reports were designed to capture statistical information related to investment and business counselling activities. The annual performance reports provided a qualitative assessment of CFDC activities, outcomes and impacts, related to access to capital, and business services; as well as quantitative and qualitative information related to strategic planning and community economic development projects. These reports made it possible for FedNor to monitor CFDC activities, outcomes and impacts, identify where best practices exist, and collect data for potential benchmarking exercises. Finally, CFDC business plans are submitted to FedNor on either a one-year or a three-year cycle, depending on FedNor's assessment of risk and performance level of the CFDC. The business plans outline the CFDC's future goals, objectives, and planned activities as well as performance targets for the duration of the plan. In addition, CFDCs are contractually obligated to submit an Audited Financial Statement and Investment Fund Report to FedNor annually. The Investment Fund Report provides performance information with respect to CFDC investment fund activity and enables an assessment of the historical and current financial information of individual CFDC investment portfolios.

The 2008 Evaluation of the Community Futures Program in Ontario recommended that FedNor complete a review of the performance data collected to ensure reliable and meaningful reporting and establish additional indicators to provide information for assessing the longer-term impacts of the program. As a result of the Evaluation, an interdepartmental CFP National Program Performance Measurement (PM) Strategy Committee was established with the RDAs and Industry Canada (FedNor) to develop and implement a National PM Strategy for the program (initially completed in August 2010, and revised January 2013). This strategy was to ensure consistency in collecting, analysing and reporting on program performance data. In particular, there are new indicators that rely on Statistics Canada data that are helping to better assess longer-term impacts. The CFP PM Strategy also includes common indicators across departments to facilitate a comparison of program results at the national level.

FedNor has been diligent in the implementation of the National PM Strategy and this has served to strengthen accountability, transparency, and performance reporting to the government. Their approach included the following activities: