Final Report

February 2011

Tabled and approved at the Departmental Evaluation Committee on February 23, 2011

Table of Contents

- List of Acronyms

- Executive Summary

- 1. 0 Introduction

- 2.0 Methodology and Approach

- 3.0 Findings

- 4.0 Conclusions and Lessons Learned

Annexes (separate document)

(Note: Annexes are available via an Access to Information Request)

- Appendix A—SFF Funded Projects Since 2007

- Appendix B—Evaluation Matrix

- Appendix C—Interview Guides

- Appendix D—File Review Grid

- Appendix E—Evaluation Advisory Committee

- Appendix F—Bibliography/List of Documents Reviewed

- Annex—Previous Evaluation Findings

List of Acronyms

ACCA: Accelerated Capital Cost Allowance

OECD: Organization for Economic Cooperation and Development

NSPS: National Shipbuilding Procurement Strategy

PSF: Project Summary Form

RMAF: Results-based Management and Accountability Framework

RBAF: Risk-Based Audit Framework

SFF: Structured Financing Facility Program

Executive Summary

Program overview

The objective of the Structured Financing Facility (SFF) is to help ensure that shipyard capability exists for federal marine procurement and maintenance requirements. The program provides contributions to reduce the interest or leasing costs to customers of Canadian shipyards when building or modifying vessels or offshore marine structures.

The program began in 2001. It was renewed in 2007 with funding to March 31, 2011 and program authority until March 31, 2013. In June 2010, the Government of Canada announced a new National Shipbuilding Procurement Strategy (NSPS) to develop and implement a long-term approach to shipbuilding procurement to meet federal government needs. In this current context, the SFF is intended to act as a "bridge" to help ensure that Canadian shipyard capability exists in advance of the implementation of the NSPS.

Purpose of Evaluation and Methodology

The overall purpose of this evaluation was to assess the relevance and performance of the SFF; provide evidence-based information for decision making; and fulfill the Treasury Board Policy on Evaluation requirements. The evaluation covers the period from July 2007 to March 2011 for projects that were approved under the renewed terms and conditions. During this period, eight projects were funded.

The evaluation was based on multiple lines of evidence. Interviews were conducted to gather in-depth qualitative information. Five case studies were conducted covering buyers (including one foreign buyer) and builders on both coasts. The purpose of the case studies was to obtain an overall understanding of funded projects and to understand the impacts at the local level. Program documentation, files and data were also analyzed for the evaluation.

The evaluation encountered a number of challenges that limited the extent to which the relevance and performance of the SFF could be assessed:

- First, a baseline of Canadian shipyard performance and capacity was not established. This made it difficult to assess the impact of the SFF on revenues, exports, employment levels, skill levels, tonnage capacity, and capacity utilization levels.

- Second, post-project reporting was often incomplete and inadequate. This limited the ability to measure the impact of the SFF.

- Finally, the absence of a comparison group made it difficult to identify what the results would have been had the SFF not existed.

Conclusions

Relevance

In the 2010 Speech from the Throne, the federal government noted its commitment to support the sustainable development of the domestic shipbuilding industry through a long-term approach to federal procurement. From this perspective, the SFF supports the government priority and helps meet the need to help maintain capacity and ensure the presence of a competitive shipbuilding industry prior to the implementation of the NSPS. The SFF is also consistent with federal roles and responsibilities.

Performance

The SFF contributed to the creation of demand in Canadian shipyards. It played a role in reducing the price disadvantage relative to foreign bids to a point where the residual was small enough to tip the balance in favour of Canadian shipyards. For the period between 2007 and 2009, the $18 million invested by the SFF helped Canadian shipyards win $134 million in contracts. In total, SFF-funded projects made up 38% of total industry revenue.

It is difficult at this stage to determine whether these investments will contribute to ongoing demand because the current iteration of the program is fairly new and shipbuilding activities are fairly long term. However, Canadian shipyards have developed and strengthened niche markets in areas such as cruise ship refitting, tugboat building and electronic control systems, in part because of the SFF.

The success of Canadian shipyards in winning these projects contributed to the maintenance of shipyard capabilities that will be necessary to meet the future procurement and maintenance needs of the federal government. More specifically, SFF-funded work supported the retention of skilled staff in both large and medium-sized shipyards and the implementation of innovation and productivity improvements. The program had its greatest impact on medium-sized yards. There is also evidence to suggest that, without the program, at least one shipyard might have closed.

Overall, the ratio of administrative costs to total program costs and the funding level contribution were reasonable.

In terms of areas for improvement, the evaluation found that potential projects may be lost due to an inability to receive SFF approval early in the bid preparation process. The evaluation also found that smaller projects which could potentially contribute to meeting future federal procurement needs do not qualify under the SFF eligibility criteria.

Lessons Learned

The SFF has approved funding until March 31, 2011. Given this, there are no recommendations. Instead, the following lessons learned are presented in the event that the Government allocates new resources to the program or establishes a similar program in the future.

Lesson Learned 1: At the outset of a program, baseline data should be established. This will assist in measuring progress towards the achievement of outcomes.

Lesson Learned 2: The eligibility criteria of a program should consider allowing for the full range of projects that would support policy objectives to be eligible for funding.

Lesson Learned 3: The project approval process should be timely to ensure that bids are not lost due to approval delays.

1.0 Introduction

This report presents the findings and conclusions of an evaluation of the Structured Financing Facility program. This section provides an overview of the context within which the Canadian shipbuilding industry is situated, a profile of the program, the purpose and scope of the evaluation, and challenges and limitations for the evaluation. Section 2 provides an overview of the methodological approach. Section 3 discusses evaluation findings by evaluation issue. Finally, conclusions and lessons learned are presented in Section 4.

1.1 Context

1.1.1 Overview

The Canadian shipbuilding industry is composed of shipbuilding, ship repair, small ship conversion, professional services and equipment suppliers. Shipyard activities include the construction, repair and conversion of ships; the production of prefabricated ship and barge sections; the manufacture of offshore oil and gas well drilling and production platforms and various heavy industrial steel fabrications; and specialized services performed in a shipyard.

The shipbuilding sector in Canada is subject to cyclical growth and decline in activity because of various factors, including the declining competitiveness of the Canadian marine industry, growing international competition in shipbuilding, and fluctuations in government procurement activity.

During the early 1980s, the industry was characterized by overcapacity, poor productivity and low capital expenditures. This resulted in an industry-led rationalization from 1986 through to 1993, to which the federal government provided assistance totaling $197.9 million for expenditures related to capacity reduction, diversification, and employee adjustment and financing costs.1

Rationalization initiatives resulted in capacity shrinkage of some 30% in Ontario, Quebec and British Columbia, a reduction of some 5,480 employees, and improved competitiveness in most of the yards in those provinces. The major Atlantic shipyards did not participate in the rationalization because of a commitment by the Department of National Defence for the construction of frigates2. The smaller Atlantic yards were occupied with new construction, repair and overhaul, and building niche vessels.

The Canadian shipbuilding industry continued to decline though the balance of the 1990s, with an overall trend of lower revenues and employment. Employment from shipbuilding declined by more than 50 % from 1990 to 2000, and began levelling off as of 2003. Employment stood at less than 4,000 in 2005; the industry generated revenues of about $525 million annually from about 30 shipyards across Canada.3

Footnotes

1 36th Parliament, 1st Session, Edited Hansard—Number 220, Monday, May 3, 1999. Return to reference 1

2 Standing Committee On Finance, Evidence, Thursday, June 8, 2000. Return to reference 2

3 Statistics Canada, Annual Survey of Manufacturers. Return to reference 3

1.0 Introduction (continued)

1.1 Context (continued)

1.1.2 Latest Industry Trends

The overcapacity challenge facing the Canadian shipbuilding industry continues to this day. The slow overall decline in revenues and employment can be seen below (Exhibit 1.1).

| Year | Manufacturing Revenue (in $M) | Production workers (direct labour) | Administrative Employees |

|---|---|---|---|

Source: Statistics Canada. Table 301-0006—Principal statistics for manufacturing industries, by North American Industry Classification System (NAICS), annual (dollars unless otherwise noted), CANSIM (database). The figures from 2008 are the latest available. | |||

| 2000 | 823.0 | 4,954 | 873 |

| 2001 | 546.2 | 3,753 | 531 |

| 2002 | 662.0 | 3,374 | 670 |

| 2003 | 535.5 | 3,235 | 562 |

| 2004 | 577.5 | 3,452 | 457 |

| 2005 | 531.1 | 3,249 | 451 |

| 2006 | 530.3 | 2,737 | 533 |

| 2007 | 536.7 | 2,968 | 485 |

| 2008 | 514.9 | 3,045 | 521 |

From 2000 to 2008, manufacturing shipments fell by 37.4% and domestic demand for shipbuilding and repair decreased by 45.4% (Exhibit 1.2). During this period, employment, wages and salaries demonstrated similar trends and rates of change.

| 2000 | 2008 | % Change | |

|---|---|---|---|

Source: Statistics Canada—Canadian Industry Statistics. | |||

| Manufacturing Shipments | $823.0M | $514.9M | -37.4% |

| Apparent Domestic Market1 | $1,461.1M | 798.3M | -45.4% |

| 2000 | 2007 | % Change | |

| Total Employees | 5,827 | 3,425 | -41.2% |

| Wages and Salaries | $293.6M | $171.6M | -41.6% |

Suppliers often look to overseas markets to generate revenue when domestic demand contracts. The Canadian shipbuilding industry has had limited success selling to foreign customers, and faces stiff competition from foreign shipyards. Since 2000, the value of imports to Canada has outpaced exports by at least 4 to 1 (see Exhibit 1.3). This is despite a 25% import duty on foreign-built ships. The largest export destination for Canada has been the United States ($490.7 million). The U.S. has also been the greatest source of imports into Canada ($875.7 million), followed closely by Korea ($857.7 million) and Germany ($522.7 million).

Exhibit 1.3: Exports and Imports (2000–2009)—Ship Building and Repairing (NAICS 336611)

| Exports | Total ('00-'09) |

|---|---|

Source: Statistics Canada—Canadian Industry Statistics | |

| United States (U.S.) | $490,700,328 |

| United Arab Emirates | $55,467,467 |

| United Kingdom (U.K.) | $10,291,300 |

| Jordan | $7,151,506 |

| Japan | $4,395,178 |

| Saudi Arabia | $3,514,033 |

| New Caledonia | $1,345,268 |

| Nigeria | $818,512 |

| Honduras | $587,000 |

| Ecuador | $397,665 |

| Sub-total | $574,668,257 |

| Others | $338,210,647 |

| Total (all countries) | $912,878,904 |

| Imports | Total ('00-'09) |

|---|---|

Source: Statistics Canada—Canadian Industry Statistics | |

| United States (U.S.) | $875,685,334 |

| Korea, South | $857,658,940 |

| Germany | $522,670,426 |

| Chile | $158,852,321 |

| Norway | $149,608,302 |

| China | $142,026,905 |

| Turkey | $61,231,700 |

| Re-Imports (Canada) | $33,117,696 |

| Australia | $2,886,573 |

| France | $1,425,321 |

| Sub-total | $2,805,163,518 |

| Others | $1,042,430,600 |

| Total (all countries) | $3,847,594,118 |

There have been some positive signs in recent years for the domestic shipbuilding and repair industry. Export intensity (domestic exports as a percentage of shipments) and the relative size of Canada's trade balance (exports minus imports divided by exports plus imports) improved steadily from 2000 to 2007 (see Exhibit 1.4). In 2000, Canada's shipbuilding export intensity was just 5%. Over time, the industry gradually moved toward higher export intensity and an improving relative balance of trade. The exception was 2008, which was characterized by lower global demand for shipping services and only $62 million in exports.

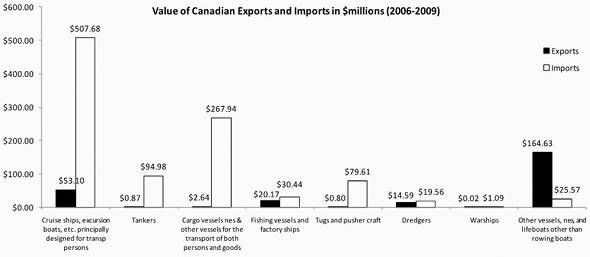

Despite a general movement toward increased export intensity, a closer look at the exporting and importing in recent years of specific goods produced by Canada's major shipyards reveals how exports are relatively minor in terms of value compared to imports. For example, the value of tankers, cargo vessels, and tugboats imported from 2006 to 2009 exceeds the value exported by approximately 100 to 1. The largest vessels imported (e.g., cruise ships, excursion boats, and ferries) were approximately ten times the value of similar exports. Fishing vessels and dredgers have a more attractive ratio. However, the value of these vessels suggests they are a small market compared with cruise ships, excursion boats, and cargo vessels (see Exhibit 1.5).

1.0 Introduction (continued)

1.1 Context (continued)

1.1.3 Shipbuilding and Government Procurement

The federal government has played a key role in the industry through procurement processes since WWII. Since the 1950s, the vast majority of Canadian government-owned ships have been designed and built in Canadian shipyards.4 The steady stream of work created solid industry capability within Canada that has survived until today. Government fleet procurement, however, mirrors the cyclical nature of the sector as a whole. The last shipbuilding project, the Maritime Coastal Defence Vessel, was completed in 1998 by Halifax Shipyards (now a part of Irving Shipbuilding). The last time a Coast Guard vessel was built and delivered was in 1983. Most Canadian shipyards have not received any government orders for new construction since the 1980s, and several yards have since shut down or converted to more general industrial pursuits.5

The National Shipbuilding Procurement Strategy (NSPS)

The Government of Canada is now looking at replacing some of its aging Department of National Defence (DND) and Canadian Coast Guard (CCG) vessels. Under the Canada First Defence Strategy, the government has committed to renewing the Canadian Forces' core equipment platforms, and starting in 2015, the navy will need 15 ships to replace its destroyers and frigates. These new ships will ensure that the military can continue to monitor and defend Canadian waters and make significant contributions to international naval operations.6 In total, the Government of Canada will require approximately 28 large ships and more than 100 smaller ships to be procured over the next 30 years.7

The Government of Canada outlined its fleet procurement renewal plans with the announcement in 2010 of the National Shipbuilding Procurement Strategy (NSPS).8 Canada plans to establish a strategic relationship with two Canadian shipyards for large ship construction through an open and fair process. The selected yards will also be designated as sources of supply. One shipyard will be for combat vessels and the other for non-combat vessels. The large ships currently expected to be required include:

- Arctic/Offshore Patrol Ships

- Joint Support Ships

- Canadian Surface Combatants

- Offshore Oceanographic Science Vessel

- Offshore Fisheries Science Vessels, and

- Polar Icebreakers.

Smaller vessels have less than 1000 tonnes of displacement. For DND, the smaller vessels will include large and small tugboats. For the CCG, they will include a variety of vessels: search and rescue lifeboats; mid-shore science vessels; channel survey and sounding vessels; near-shore fishery research vessels; specialty vessels; and special navaid vessels.

Shipyards selected to build the large vessels and their affiliates will be precluded from participating in the procurement process for the smaller vessels. Shipyards will also have the opportunity to compete for the repair, refit and maintenance of vessels as per the current practice of publicly announced requests for proposals. Small and medium-sized enterprises will have the opportunity to provide goods and services to shipyards and other suppliers involved in building and servicing the ships. These orders by the government are expected to sustain the Canadian shipbuilding industry for some time. To participate, yards must first have in place the capability to deliver the products and services necessary for Canadian fleet renewal.

Footnotes

4 Canadian Association of Defense and Security Industries, The Report of the CADSI Marine Industries Working Group, Sovereignty, Security and Prosperity (May 2009). Return to reference 4

5 Ibid., p. 11. Return to reference 5

6 National Defence. Canada First Defence Strategy. June 18, 2010. Return to reference 6

7 www.cbc.ca/canada/story/2010/07/14/government-shipbuilding-strategy.html. Return to reference 7

8 National Shipbuilding Procurement Strategy. Return to reference 8

1.0 Introduction (continued)

1.2 Description of the Structured Financing Facility

The Structured Financing Facility (SFF) was first announced in June 2001 and was a key component of the overall policy framework for the Shipbuilding and Industrial Marine sector. This policy focused on taking advantage of market opportunities, promoting investments to complement Canadian competencies in marine industries in areas of market opportunity, and assisting innovation in key technologies.9 The SFF was a response to requests from industry to modify tax regulations to permit the use of specific tax provisions in situations where Canadian vessels are sold to leasing companies rather than operators. By providing financial assistance to Canadian and foreign buyers and lessees through the SFF, it was anticipated that demand would be stimulated for new-builds, conversions, refits and modifications in existing Canadian shipyards. This, in turn, would help address some of the competitive gaps between Canadian and foreign shipyards.10

The initial budget for the SFF in 2001 was $150 million over a five-year period, with $5 million reserved for operating costs. In January 2003, the SFF budget was reduced by $20 million in 2003–2004 and $24 million in 2004–2005 as part of the government-wide resource reallocation exercise. Budget reductions for the SFF continued over time. As a result, the budget stood at $68 million as of March 31, 2007 when the SFF budget commitment terminated.11

In June 2007, Industry Canada (IC) received $45 million in contribution funding and $5 million in operating funds for a renewed Structured Financing Facility Program. This funding was approved until March 2011.12

Three of the roughly thirty Canadian shipyards (large to medium size) have benefited from the SFF under the renewed terms and conditions.13 As shown in Exhibit 1.6, two of the shipyards are in British Columbia and one is in Prince Edward Island.

| Year | Shipyard | Province | SFF Contribution |

|---|---|---|---|

| Source: SFF program files | |||

| 2007–2010 | Deas Pacific Marine | BC | $1,012,092 |

| Vancouver Drydock | BC | $4,984,000 | |

| Irving—East Isle | PEI | $12,110,400 | |

1.2.1 Objectives and Activities

Whereas the original SFF program was intended to stimulate economic activity in the Canadian shipbuilding and industrial marine industry, the renewed SFF is intended to maintain shipbuilding capacity in Canada until there is sufficient government procurement to provide the activity base to make the industry self-sustaining.14

Under the program, a non-repayable contribution is provided to lending and leasing institutions to buy down the interest rate of the loan or lease that is used to acquire a new or converted vessel built in Canada.15 The federal contribution can be up to 15 percent of the purchase price paid to the Canadian shipyard for the construction or modification of an eligible vessel or offshore marine structure.

Eligible projects include the purchase, conversion, refurbishment or modification in a Canadian shipyard of a vessel that is solely intended for use in a commercial operation, service or venture. The shipyard must be in Canada on a water way accessible to ocean-going traffic. The purchase price must be at least $5 million.

top of page1.2.2 Planned and Actual SFF Expenditures

The total program budget was $50 million over four years (2007–2008 to 2010–2011), of which $5 million was intended for operating and maintenance and $45 million for grants and contributions. The renewed program went through a startup phase the first year, during which operating and maintenance expenditures were not budgeted, although projects began to be approved. Exhibit 1.7 provides planned and actual expenditures for the program.

Expenditures between 2008 and 2010 were lower than expected. In this period, there was a downturn in the global economy while the Canadian dollar was relatively high. This reduction in demand in Canada was consistent with world-wide shipbuilding activity. The OECD reported that, globally, new orders fell from 22.2 million Compensated Gross Tons (cgt) in the third quarter of 2007 to 12.3 million cgt in the third quarter of 2008, and to just over 1 million cgt in the last quarter of 2008 and first quarter of 2009. This represents a decrease of approximately 90% from the peak level.16

| 2007–2008 | 2008–2009 | 2009–2010 | 2010–2011 | Total | |||||

|---|---|---|---|---|---|---|---|---|---|

| Planned | Actual | Planned | Actual | Planned | Actual | Planned | Planned | Actual | |

| Source: SFF Program Files | |||||||||

| O&M | $ - | $0.51 | $1.16 | $0.78 | $1.16 | $0.43 | $1.19 | $3.51 | $1.72 |

| G&C | $21.51 | $4.97 | $15.51 | $15.15 | $18.13 | $5.96 | $18.13 | $73.28 | $26.08 |

| Total | $21.51 | $5.48 | $16.67 | $15.92 | $19.28 | $6.39 | $19.32 | $76.78 17 | $27.79 |

1.2.3 Expected Outcomes and Logic Model

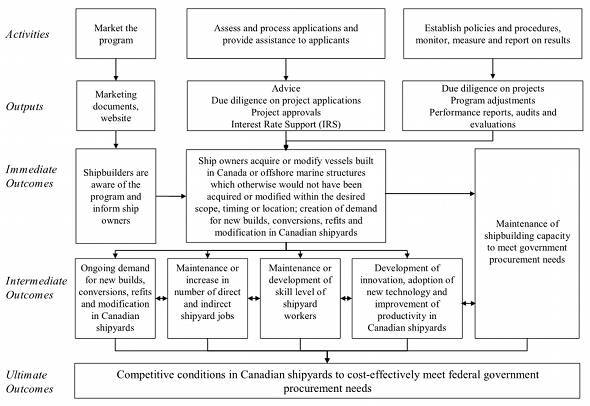

The SFF Program logic model, developed as part of the RMAF/RBAF (2007), is as follows.

The SFF logic model illustrates the expected impact of the program by linking program activities to outputs, and outputs to outcomes. The key program activities (market the program; assess and process applications and provide assistance to applicants; and establish policies and procedures, monitor, measure and report on results) are expected to lead to the outputs described in the model. These in turn are expected to lead the following outcomes:

Immediate outcomes

- Shipbuilders are aware of the program and inform potential owners

- Ship owners acquire/modify vessels or offshore marine structures in Canadian shipyards where, without the SFF, they may not otherwise have done so

- Maintenance of shipbuilding capacity to meet government procurement needs

- Creation of demand for new-builds, conversions, refits and modifications in Canadian shipyards.

Intermediate outcomes

- Ongoing demand for new-builds, conversions, refits and modifications in Canadian shipyards

- Maintenance or increase in number of direct and indirect shipyard jobs

- Maintenance or development in skill level of shipyard workers

- Development of innovation, adoption of new technology and improvement of productivity in Canadian shipyards.

Ultimate outcomes

- Competitive conditions in Canadian shipyards to cost-effectively meet federal government procurement needs.

Footnotes

9 Integrated Results-based Management and Accountability Framework (RMAF) and Risk-Based Audit Framework (RBAF) for the Structured Financing Facility (SFF) Program, 2007, p. 1. Return to reference 9

10 Ibid. Return to reference 10

11 Final Evaluation of the Structured Financing Facility Program, Final Report, Feb. 8, 2008. Raymond Chabot Grant Thornton Consulting Inc., p. 4. Return to reference 11

12 Canada's New Government Announces Renewed Federal Shipbuilding Approach. Return to reference 12

13 SFF Program Database. Return to reference 13

14 Integrated Results-based Management and Accountability Framework (RMAF) and Risk Based Audit Framework (RBAF) for the Structured Financing Facility (SFF) Program, 2007, p. 3. Return to reference 14

15 www.ic.gc.ca/eic/site/sim-cnmi.nsf/eng/h_uv00002.html#description. Return to reference 15

16 www.oecd.org/document/6/0,3343,en_2649_34211_43319760_1_1_1_1,00.html. Return to reference 16

17 Total planned expenditures exceed the $50M provided for the program for a number of reasons, namely reprofiling of funds, transfers to/from a reserve, and reallocation within the department. Total actual expenditures reflect spending under previous and current terms and conditions. Return to reference 17

1.0 Introduction (continued)

1.3 Purpose and Scope of the Evaluation

The overall purpose of this evaluation was to examine issues of relevance and performance. In terms of relevance, need and alignment directed the evaluation. The extent to which the program continues to address a demonstrable need and is responsive to the needs of Canadians was assessed. In terms of alignment, the purpose was to assess the linkages between program objectives and federal government priorities as well as departmental strategic outcomes, and to assess the role and responsibilities of the federal government in delivering the program.

In terms of performance, the purpose of the evaluation was to examine issues of effectiveness (progress toward expected outcomes) and efficiency and economy. Effectiveness was assessed with reference to performance targets, program reach, and program design, including the linkage and contribution of outputs to outcomes. Efficiency and economy were assessed with reference to resource use in relation to the production of outputs and progress toward expected outcomes.

This evaluation was also intended to provide evidence-based information for decision making as well as fulfill Treasury Board Policy on Evaluation requirements. The evaluation issues were assessed with reference to the following questions:

Relevance

- Does the SFF continue to be consistent with departmental and government-wide priorities?

- Is the SFF an appropriate role for the federal government?

- Is there a continued need for the SFF program?

Performance (effectiveness, efficiency and economy)

- Has the SFF helped ensure that shipyard capability exists for federal procurement and maintenance needs in 2009 and beyond?

- Were the shipbuilders and ship owners targeted by the program appropriately aware of the SFF and its potential benefits?

- To what extent and in what way has the program contributed to the creation of demand for new-builds, conversions, refits and modifications in Canadian shipyards?

- To what extent and in what way has the program contributed to ongoing demand for new-builds, conversions, refits and modifications in Canadian shipyards?

- What impact has the program had on direct and indirect shipyard jobs?

- What impact has the program had on the skill level of shipyard workers?

- What impact has the program had on the development of innovation, adoption of new technology and improvement of productivity in shipyards?

- If the program is renewed, what changes should be made to improve its likelihood of success?

- Could the results have been achieved for a lesser cost?

In 2007, the terms and conditions of the program were revised substantially. As a result, a decision was made to examine the impacts of only the projects funded under the revised terms and conditions from July 2007 to March 2011. During this period, eight projects were funded under the revised terms and conditions; the impacts of these projects are assessed in this report. Five additional projects were funded in this period under the previous terms and conditions; their impacts are not assessed in this evaluation. For further details, please see Appendix A.

top of page1.4 Challenges and Limitations

This evaluation faced a number of significant challenges that limited the extent to which the impact of the SFF could be measured.

Absence of a Baseline for the Target Population

The most significant challenge was the absence of a performance baseline for the target population. A survey of Canadian shipyards prior to the new funding period would have established a baseline for comparison. Ideally, the information gathered would have included revenues, exports, employment levels, skill levels, tonnage capacity, capacity utilization levels, etc. This information would have provided a deeper understanding of the impact of the SFF on Canadian shipyards.

Lack of Rigorous Project Reporting

Project reporting also limited the ability to measure the impact of the SFF. An examination of reports for the eight SFF projects examined revealed several weaknesses. In particular:

- Quantitative information (e.g., actual number of person years employed on projects) was not completed for any completed projects

- Project impact assessment reporting form was not used consistently nor comprehensively in terms of information capture

- Site visits were conducted one to two months after the project began, which was far too early to capture useful performance information

- Several impact assessment reports simply used the ones created during the application process, with some handwritten notes taken during the shipyard visit, and no quantitative figures collected and

- An electronic program file exists that claims to show actual shipyard person years (PYs). However, the evaluation found these are simply the original PY estimates found in the project applications.

The current design of the impact assessment reports also lacks some important data that should be captured, namely total employment levels (PYs), non-SFF revenue at the shipyard during the months of the SFF project, and capacity utilization rates.

Lack of a Comparison Group/Comparable Program

Without a comparison group, it is difficult to identify what the results would have been had the SFF not existed. The creation of a comparison group was not possible because the program does not have a record of purchases of vessels by Canadian or foreign buyers who did not apply for SFF funding. In addition, no applications that met all of the program criteria were rejected. Nonetheless, the methodology featured a number of strengths to ensure robust findings:

- The evaluation team conducted a representative group of case studies (further discussed in the next section), covering five of the eight contributions.

- The program file information included detailed quantitative impact information on all projects and was deemed of high quality.

- The evaluators conducted in-depth interviews, which are considered highly effective in getting rich information of high quality.

These multiple lines of evidence provided converging information for assessments of relevance and performance and provided sufficient mitigation against the challenges.

2.0 Methodology and Approach

This evaluation study was undertaken by Goss Gilroy Inc., on behalf of Industry Canada. The evaluation was based on four lines of evidence (methods): secondary data analysis; document and file review; interviews; and case studies.

Secondary Data Analysis

The evaluation used a number of sources to obtain data on Canada's shipbuilding industry. By sourcing Statistics Canada data, Industry Canada's website offers robust data on Canada's shipbuilding and repair industry (NAICS 366611). The evaluation used data such as employment, manufacturing revenues, exports, and imports for the 2000–2009 periods. In addition, Statistics Canada data was used to identify exports and imports at a more disaggregated level for cruise ships, tankers, tugs, and other products.

Trade data from the International Trade Centre UNCTAD/WTO (ITC) were also used to identify the top countries to which Canada's shipbuilding industry exports and the top countries for Canadian imports.

Document Review

Program documentation, files and data were reviewed as part of the evaluation. Project summaries completed by Industry Canada at the application stage provided excellent information on buyers, shipyards, competitive bids, innovative aspects of the project, and the impact on the projects if SFF funding were not secured. The program also keeps a database of projects that contains a great deal of useful information. Additional documents analyzed included previous evaluations, papers on Canada's shipbuilding industry, the program's RMAF/RBAF, and interim and final project impact assessment reports.

Interviews

Interviews were conducted to gather in-depth qualitative information. The interviewees represented a cross-section of stakeholders including shipyard representatives, domestic and foreign buyers, program management, and industry and labour representatives. The interviews allowed evaluators to gain insight into the relevance and performance of the program from the perspective of many different stakeholders. These interviews were conducted by phone, on location in Ottawa, and by site visits to shipyards. A total of 22 individuals were interviewed, as indicated below:

- Program management and staff (3)

- Representatives of other government programs (3)

- Shipbuilders (8)

- Ship owners (purchasers) (4)

- Ship owners (non-participant) (1)

- Subcontractor (1)

- Labour representative (1), and

- Industry association representative (1).

Case Studies

Five case studies were conducted out of the eight projects funded since 2007. The selected projects were undertaken by the Irving (East Isle), and Washington Marine Group (Victoria Shipyard) shipyards, while the buyers were Groupe Ocean, Nordane, and BC Ferries.

The interviewees for the case studies consisted of buyers and builders on both coasts and one foreign buyer. The purpose of the case studies was to provide an overall understanding of SFF projects, and to understand the impacts at the local level.

3.0 Findings

3.1 Relevance

Issue 1. Does the SFF continue to be consistent with departmental and government-wide priorities?

Finding: The SFF continues to be consistent with departmental and federal government priorities concerning the retention of capacity in the shipbuilding industry.

Although the 2010 Throne Speech did not mention the SFF explicitly, it recognized the strategic importance of having a strong domestic shipbuilding industry and noted the government's intention to continue to support the industry through federal procurement.18 According to the 2007 RMAF/RBAF, the renewed SFF is intended to maintain shipbuilding capacity in Canada until there is sufficient government procurement to provide the activity base to make the industry self-sustaining.19 This suggests that the SFF remains a government priority until the implementation of the NSPS. It is anticipated that this will occur within the next few years.

Within Industry Canada's 2010–11 Program Activity Architecture, the SFF program falls under the strategic outcome "Competitive Businesses are Drivers of Sustainable Wealth Creation." It is a sub-activity of the "Global Reach and Agility in Targeted Canadian Industries" activity area. The SFF supports competitiveness and is expected to lead to sustainable economic development.

Issue 2. Is the SFF an appropriate role for the federal government?

Finding: The issues addressed by the SFF program fall under the responsibility of the federal domain.

The issues addressed by the SFF program fall under the overall responsibility of the federal domain, including areas of national security, economic development, and international competitiveness.

There is no overlap of the SFF with provincial jurisdiction and programming. Individual provinces offer broad programs in support of manufacturing, innovation, and research and development. Shipyards that have benefited from the SFF have taken advantage of these general programs. In particular, provincial apprenticeship programs have proven beneficial for the Canadian shipbuilding industry. However, the SFF is the only program in Canada that is aimed specifically at supporting the shipbuilding industry.

From a taxation perspective, Canadian ship owners can choose to take advantage of the Accelerated Capital Cost Allowance (ACCA) or the SFF, but not both. Canadian income tax regulations remove the right to the ACCA for vessels whose construction or modification was supported by the SFF. The 15% maximum contribution provided under the program is the estimated amount of support needed to equal the value of the ACCA.

Issue 3. Is there a continued need for the SFF program?

Finding: There is a continued need for this program to help maintain industry capacity until the NSPS is implemented. Canadian shipyards have had limited success in penetrating international markets and rely heavily on the SFF to be price competitive on both domestic and foreign bids.

Various lines of evidence indicate that there is a need for the SFF to help support the Canadian shipbuilding industry until the NSPS is implemented. Statistics Canada figures indicate that the Canadian shipbuilding industry faces fierce competition from abroad. Canadian demand for shipbuilding and repair averages more than $500 million per year. Canadian shipbuilding demand from 2005–2008 was satisfied through imports, at 37.4%. Over the last ten years, imports have exceeded exports on average by a factor of 4 to 1.20

Stakeholder interviews and case study findings also support the need for the program. Several Canadian shipyards have closed over the last 20 years. Some ship buyers are concerned that Canadian shipyards no longer have the necessary know-how to build large ships. For example, the decision by BC Ferries in 2004 to award a contract to a German shipyard to build three new ferries was perceived by some as indicative of a lack of expertise in the BC shipyard industry. The President of BC Ferries argued that "the provincial industry no longer has the infrastructure or the competitive edge to build BC's big ferries."21 BC has one of the largest ferry fleets in the world, representing a potential source of business for Canadian yards.

The United States market (the most natural and largest potential market for Canadian shipbuilders) is essentially inaccessible due to the Jones Act. This Act prevents US buyers from purchasing foreign-built ships for commercial shipping within the US. Stakeholders also noted that the large ship market in Canada has recently become more competitive with the elimination of the 25% import duty on ships over 129m in length.

Analysis of program files reveals that Canadian suppliers face a price disadvantage versus foreign competitors. Based on the four SFF projects for which foreign shipyard bid information was available, Canadian bids were on average 20% higher than comparable foreign bids (see Exhibit 3.1). The SFF effectively reduced the overall price of a ship by 11-14%, and closed the competitive disadvantage to between 4.3% and 13.5%.

| Project | Canadian Bid ($M) | Best Foreign Bid ($M) | Initial Price Disadvantage | SFF Contribution ($M) | Remaining Difference |

|---|---|---|---|---|---|

| Source: SFF Program Files | |||||

| #1 | $44.500 | $37.825 | 15.0% | $4.984 | 4.3% |

| #2 | $47.800 | $37.600 | 21.3% | $7.170 | 7.5% |

| #3 | $10.000 | $7.353 | 26.5% | $1.500 | 13.5% |

| #4 | $22.936 | $18.666 | 18.6% | $3.440 | 4.3% |

| Average | 20.4% | 7.4% | |||

Stakeholders maintained that without the financial assistance of the SFF, Canadian bids would not have been price competitive with foreign shipyards. They also believed that the relatively high Canadian dollar in recent years has not led to a reduction in costs.

It is anticipated that the launch of the NSPS will necessitate a review of the continued need for the SFF. As federal procurement efforts are initiated and the industry revitalizes core shipbuilding capabilities, the need for "bridge" mechanisms like the SFF is expected to decline.

Footnotes

18 "It [the Government of Canada] will take further steps to support the competitiveness of Canadian manufacturers. And recognizing the strategic importance of a strong domestic shipbuilding industry, it will continue to support the industry's sustainable development through a long-term approach to federal procurement." 2010 Speech from the Throne. Return to reference 18

19 Integrated Results-based Management and Accountability Framework (RMAF) and Risk-Based Audit Framework (RBAF) for the Structured Financing Facility (SFF) Program, 2007, p. 3. Return to reference 19

20 Statistics Canada, Canadian Industry Statistics, NAICS 336611, 2000–2009. Return to reference 20

21 Douglas, "Only the Strong Survive", Nov/Dec 2008, p. 37. Return to reference 21

3.0 Findings (continued)

3.2 Performance

Issue 4. Has the SFF helped ensure that shipyard capability exists for federal procurement and maintenance needs in 2009 and beyond?

Finding: The SFF has played a role in ensuring that shipyard capability exists in Canada for federal procurement and maintenance needs. The program helps maintain skilled staff at both medium and large-sized shipyards.

The objective of the Structured Financing Facility is to help ensure that shipyard capability exists until there is sufficient government procurement to provide the activity base to make the industry self-sustaining. The SFF is currently envisioned as an interim measure to maintain shipyard capability until such time as the NSPS is implemented. (The exact implementation date for the NSPS is unknown but is expected within three years.) In order to meet the expected procurement requirements of the NSPS, Canadian shipyards must maintain and enhance the following capabilities:

- Project management expertise and development

- Development of partnerships (provinces, other enterprises)

- Business practices demonstrating continuous improvement ,and

- Infrastructure investment.

The contribution of SFF-funded projects to developing each of these capabilities is as follows:

- Project management—Project management practices (e.g., the Earned Value Management System) are used in all the recipient yards. The Earned Value Management System is an established practice recognized as a value-added feature of operations.

- Development of partnerships—Relationships are fostered between the large yards and neighbouring post-secondary institutions to foster skills and training relevant to the industry (more below). The supply chain for marine industries is such that many component parts are sourced from small and medium-sized enterprises. Specifically, 65% to 85% of total project costs (equipment or work elements) are Canadian-sourced, implicating other businesses generally in the shipbuilding delivery process that takes place in a yard. As well, sub-contracting is a common and growing practice in yards, necessitating the establishment of a network of partners in some form or other to deliver a ship.

- Business practices—A range of business practices in support of continuous improvement were identified in project profiles. One yard is applying Lean manufacturing principles, on more than one project. Another yard is using asset betterment approaches. Mobilization, maintain, and demobilization (MMD) practices are occurring in recipient yards alongside other types of occupational health and safety training. Where feasible, yards are seeking ISO certification, recognizing the value to the business enterprise of doing so.

- Infrastructure investment—One of the large yards noted that it has an infrastructure investment plan in place that assigns a percentage of profits to ongoing infrastructure development. However, this process is likely independent of whether or not SFF funding was received. Other yards reported that the challenging circumstances facing the marine industry create challenges to the development and enhancement of infrastructure.

Evidence shows that the SFF helps to maintain skilled staff at both medium and large-sized shipyards. By helping bring work to medium-sized shipyards, SFF funding has increased the likelihood that the shipyards will be able to bid on the smaller vessels under the NSPS. Furthermore, interviewees indicated that East Isle would likely have closed without SFF-funded projects.

As for large-sized shipyards, both WMG's Vancouver Drydock and the Irving Halifax Shipyard (both of which received SFF funding) were recently short-listed as potential suppliers (among the five) to build the larger ships under the NSPS. Interviewees at these yards indicated that SFF-funded projects helped the shipyards maintain capacity. The conclusion that can be drawn is that SFF funding has aided these yards in developing their capabilities and consequently their potential to be short-listed as potential NSPS suppliers. However, although the program augmented activity in Western Canada shipyards, these yards reported that it was not essential, to their survival as refit and life extension for Canadian Navy and Coast Guard ships provided a source of relatively steady work.

It must be noted that although the SFF is not the sole cause for the shipyard capabilities evident in recipient yards, SFF funding nonetheless played an instrumental role in facilitating projects where these capability enhancements were being implemented.

Issue 5. Were the shipbuilders and ship owners targeted by the program appropriately aware of the SFF and its potential benefits?

Finding: Industry Canada promotes the program and its potential benefits to Canadian shipbuilders. Promotion of the program on the international stage is more limited.

A portion of the program budget is targeted to promotions and advertising. Communications material is available for distribution via print and electronic media. Within Canada, program officers use shipyard site visits for outreach and program promotion as well as to fulfill program requirements.

On the domestic front, roughly 30 shipyards in Canada are of sufficient size to undertake work that meets current SFF criteria. Industry Canada contacted these shipyards at the start of the renewed program to ensure they were aware of the SFF, and the program continues to communicate with shipyard representatives. Most shipyard representatives interviewed actively encourage and assist customers in their applications for SFF funding if the project is eligible for funding.

On the international front, promotion is largely limited to attending marine industry conferences. Representatives from Industry Canada attend international tradeshows in New Orleans, Hamburg, and Oslo and have created communications material to support these efforts. The program does not collect data that would enable an assessment of the awareness levels of potential buyers (domestic or foreign).

3.0 Findings (continued)

3.2 Performance (continued)

Issue 6. To what extent and in what way has the program contributed to

the creation of demand for new-builds, conversions, refits and modifications in Canadian shipyards?

Finding: The program supported the creation of domestic and foreign demand for new-builds, conversions, refits and modifications in Canadian shipyards. The SFF-funded projects provided 38% of Canadian industry revenues between 2007 and 2009. In addition, the program helped Canadian shipyards remain competitive in international markets, and, in some cases, was a determining factor in whether projects would proceed in Canadian shipyards.

The SFF supported purchases from both domestic and foreign buyers. Of the eight projects that received SFF funding since 2007, four were with domestic buyers for a total of approximately $11 million and four were with foreign buyers, totaling approximately $7 million.

The SFF also contributed to the creation of demand by helping Canadian shipyards remain competitive in international markets. An analysis of four SFF project files (for which foreign bid information is available) demonstrates how the SFF helped reduce the gap between domestic and foreign supplier pricing (see Exhibit 3.2 below).

| Project | Canadian Bid ($M) | SFF Savings ($M) | Canadian Bid Net of SFF ($M) | Best Foreign Bid ($M) | Import Duty ($M) | Foreign Bid With Duty ($M) | Relative Cost: Foreign vs. Canadian |

|---|---|---|---|---|---|---|---|

| Source: SFF project data files | |||||||

| #1 | $44.500 | $4.984 | $39.516 | $37.825 | N/A | $37.825 | -4.3% |

| #2 | $47.800 | $7.170 | $40.630 | $37.600 | N/A | $37.600 | -7.5% |

| #3 | $10.000 | $1.500 | $8.500 | $7.353 | $1.838 | $9.191 | 8.1% |

| #4 | $22.936 | $3.440 | $19.496 | $18.666 | $4.667 | $23.333 | 19.7% |

| Total | $125.236 | $17.094 | $108.142 | $101.444 | $6.505 | $107.949 | -0.2% |

Not considering the SFF or duty costs, the Canadian bids were higher than the foreign bids. Taking into account the SFF support and import duty, the gap was closed considerably. In two cases, net prices were lower with Canadian suppliers than with foreign suppliers. Import duty was a major factor in keeping the Canadian bids competitive (see box below). For the other two projects, the foreign bids were lower by 4.3% and 7.5%. Nevertheless, the projects were awarded to Canadian shipyards. This suggests that the price gap does not need to be closed entirely for Canadian shipyards to win bids. In one case, the need for local ongoing fleet support motivated the buyer to pay a premium to keep some shipyard work within Canada.

2010 Tariff Changes

In October 2010 the federal government announced a tariff reduction measure. The new duty remission framework lowers costs for the Canadian shipping industry by waiving the 25 percent tariff on imports of all general cargo vessels and tankers, as well as ferries longer than 129 meters. The measure contributes to Canada's Economic Action Plan objectives of lowering taxes and promoting a more competitive economy.

Source: "Government of Canada Announces New Tariff Measures for Ships for a More Competitive Canadian Economy", Department of Finance News release, October 1, 2010.

A review of available project summaries revealed that SFF support was a determining factor in whether work would proceed in Canadian shipyards for the following projects: Traverse d'Oka, Neptune Seismic, BC Ferries (Quinsam and New Westminster), Nordane, and Groupe Océan.

Work supported by the SFF also represents a significant share of total Canadian industry activity. A comparison of SFF supported work with industry statistics from Statistics Canada revealed that between 2007 and 2009, the SFF-supported projects accounted for 38.0% of industry revenues (NAICS 336611) and 21.0% of industry exports.

In terms of the type of work supported by SFF-funded projects, East Isle constructed four new ocean-going tugs with ice-class hulls and state of the art z-drives. Both purchasers noted that in the absence of the SFF, they would have purchased these tugs elsewhere (likely Chile). The yard's previous experience in constructing of such vessels would not have been sufficient to offset the price differential. Importantly, with the purchase of multiples models of a ship type, the yard is able to take advantage of the learning curve effect (the first ship is the biggest challenge, with less return on investment, than for the last one built).

Two SFF-funded projects during the period of review involved refits and modifications of BC tugs. The refits were undertaken to meet stricter regulatory requirements (fire protection, life saving requirements), upgrade accommodations, upgrade accessibility, and, perform extraordinary maintenance on steel, electronics and mechanical systems. Numerous innovations were introduced throughout the refit process, including project management innovations.

There were two SFF-funded conversion projects during the period of review. One project involved the conversion of two barges into self-propelled ferries; the other was for the conversion of a trawler into a seismic survey vessel. The former project reported design innovations that will improve access for inspection and maintenance, reduce assembly time and reduce the risk of work accidents.

Issue 7. To what extent and in what way has the program contributed to ongoing demand for new-builds, conversions, refits and modifications in Canadian shipyards?

Finding: Given that the renewed program is fairly recent and shipbuilding projects are typically longer term, it is difficult to conclude if the current program is contributing to ongoing demand. However, there is some evidence that the SFF has been successful in this regard.

The extent to which the SFF has contributed to ongoing demand in terms of new-builds, conversions, refits and modifications can be measured with reference to yards that had projects previously funded, essentially a comparison over time.

Two groups may be distinguished in taking this time-comparison approach. The first group would be those yards that through previous SFF support are now self-sustaining, having established key capabilities and a competitive advantage. The second group is yards that were previous recipients of SFF support that continue to participate in the SFF program.

Previous SFF Recipients

In 2005, with the aid of SFF contributions (under previous SFF terms and conditions), Victoria Shipyards (VSL) obtained a contract with the Holland America Line to undertake a major dry dock refit of four cruise ships. Through successful completion of these projects, VSL has now become known as a shipyard of choice for major upgrades and modifications to cruise ships. VSL subsequently has undertaken similar projects.

The SFF contributions were critical in helping VSL win foreign flag cruise ship contracts. The expansion of VSL's client base is a reflection of its established reputation as a high quality, competitive North American shipbuilder and repairer of sophisticated vessels. VSL continues to secure bids in this market that would not have been possible without the SFF support. The company has also secured navy and coast guard contracts, which can capitalize on infrastructure and training investments. Thus, a successful niche market was created and maintained.

Ongoing recipients of the SFF

Two shipyards (one large, one medium) have built a number of tugboats for both domestic and foreign buyers with help from the SFF under previous and current terms and conditions of the program. They have established solid reputations for delivering quality work on advanced technological products on time (modern tugboats incorporate extremely complex technology). Without the expertise developed from previous SFF-supported work on tugboats, buyers indicate that such projects would not have been awarded to those Canadian shipyards.

3.0 Findings (continued)

3.2 Performance (continued)

Issue 8. What impact has the program had on direct and indirect shipyard jobs?

Finding: Because of insufficient reporting, there are no reliable figures on actual direct and indirect job creation from the SFF. However, funding applications for SFF projects approved since 2007 estimated that 1,410 person years of direct and indirect work would be created by these projects. Furthermore, the proportion of industry revenue accounted for by SFF-funded projects (38% for 2007 to 2009) may serve as a proxy measure of the SFF-funded share of industry employment.

The SFF Impact Assessment form is the primary document used by the program to collect program impact information. However, the form does not collect total shipyard employment levels and several projects did not provide a completed form. Furthermore, assessments are not completed annually, and instead provide "snapshots" that can yield misleading data as shipyards will frequently lay off employees when there is no work available and will re-hire the same workers when a new contract is won.

Although accurate actual SFF employment data are not available, funding applications do provide employment projections. For SFF-funded projects approved since 2007, an estimated 1,410 person years were supported. Furthermore, although accurate actual SFF employment figures are not available, actual revenue figures are. Between 2007 and 2009, SFF-funded projects accounted for 38% of industry revenues. Though employment distribution would vary across projects, it is likely that the share of employment accounted for by SFF-funded projects would be of a similar magnitude.

The SFF projects had additional impacts on the Canadian economy beyond the shipyard labour (salaries). Information gathered from the file review shows that whereas labour costs represent approximately 30% of total purchase value or total ship cost, materials purchased from Canadian suppliers account for an additional 40% or so, with the remaining 30% going to foreign firms for equipment unavailable in Canada. Several SFF projects involved the purchase of components from a Canadian firm specialized in electronic control systems allowing the firm to gain experience and build its reputation. The firm now has foreign clients and has expanded its work force from 15 to 80 full-time employees and increased its sales from $3 million to $18 million in the last five years.

Issue 9. What impact has the program had on the skill level of shipyard workers?

Finding: SFF projects are partially selected on the basis of their potential to improve the skills of shipyard workers. There is some direct evidence that SFF-funded projects have contributed to maintaining or developing shipyard skill levels, as well as provided ongoing apprenticeship/development opportunities.

Although the objectives of the SFF do not specifically include the development of the skill levels of shipyard workers, the terms and conditions of the program require that projects be partially assessed on this expected outcome. Evidence shows that the SFF helps both medium and large-sized shipyards to retain skilled staff and to maintain and enhance skills.

A significant percentage of shipyard work is carried out by skilled trades, including welders, electricians and pipefitters. By helping maintain a certain level of activity in shipyards, SFF helps maintain the employment of skilled workers and develop new skilled workers. Shipyard interviewees and the file review indicated that SFF contributions support training activities related to new technologies, and support skills upgrading, including the development of apprentices and other workers (e.g., training related to safety, carpentry, AutoCAD, crane operation, project management, and specialized equipment installation).

All the shipyards interviewed reported that they hire apprentices, which account for approximately 25% of the workforce at some shipyards. Apprenticeship programs are generally for welders, electricians, and pipe fitters. Many shipyards have strong linkages with local colleges, providing apprenticeship and employment opportunities. For example, East Isle and Holland College have apprenticeship training programs.

In addition, the increasing use of technology in ships is leading to a demand at the shipyard level for specialized training from manufacturers of advanced systems. In some cases, manufacturers require shipyards to undertake training and obtain certifications in order to install or maintain certain drive units, life rafts, and fire suppression systems to ensure that the work is done safely and correctly. For example, Deas Pacific Marine has attained Safety of Life at Sea certification for installers. By attaining this certification, Deas Pacific Marine has further opportunities for work.

3.0 Findings (continued)

3.2 Performance (continued)

Issue 10. What impact has the program had on the development of innovation, adoption of new technology and improvement of

productivity in shipyards?

Finding: SFF is not a direct driver of innovation, technology adoption, or productivity. However, SFF contributes to maintain work volume, which allows shipyards to implement innovation and productivity improvements. Without SFF, the pace of these improvements would have been reduced.

The contribution that the SFF makes toward innovation, technology adoption, and productivity is indirect. The SFF helps shipyards win business, which places shipyards in a better financial position to make the required investments. The gains accrue to subcontracted firms as well as the yards.

Modern shipbuilding is a complex exercise, involving processes much more involved than simply cutting steel. Shipyards are involved in project management, ship design, and systems integration and equipment supply, and an array of small and medium-sized enterprises provide support—human or material resources, knowledge and skill.

Although interviews and case studies indicate that shipyards have been reluctant to invest in technological upgrades that yield efficiency gains because of market uncertainty, some innovation is taking place. Areas of innovation associated with SFF-funded projects include:

- improvement in process and project management processes

- improvement in safety and operational efficiency procedures

- increased use of AutoCAD for design

- increased modularization

- advancement in applied electronics technology (use of templates and cable trays for electrical wiring, new control systems)

- innovation in design for ice daggers and deflectors, and

- advancement in training and certification (e.g. for installation and maintenance of equipment).

Support from the SFF assists in improving processes. For example, innovative techniques for installing, wiring in one ship will be applied and enhanced in subsequent projects where suitable. Gains made in adopting project management practices (e.g. electronic data capture using personal hand-held devices to record real-time labour activity) will devolve to all shipyard work—in effect a diffuse impact of the SFF program.

In the same vein, the SFF creates new demand and leads to spin-off work that often leads to productivity improvements. For example, producing tugs previously at East Isle resulted in a 5.3% reduction in person-hours per vessel.

Issue 11. If the program is renewed, what changes should be made to improve its likelihood of success?

Finding: To improve the program's likelihood of success, two changes should be considered. First, the program should consider ways to make the project approval process timelier to avoid the loss of potential projects because of approval delays. This could include an "approved in principle" mechanism. Second, the eligibility criteria should be reviewed to ensure that the full range of projects likely to support future NSPS needs are eligible now for funding.

Approval Process

Approval for SFF funding is currently provided only after a project has obtained loan approval from a financial institution. However, shipyards often need SFF approval prior to loan approval to ensure they can provide a competitive proposal to prospective buyers.

Shipyard and buyer respondents indicated high degrees of satisfaction with program officers in terms of knowledge shared and overall responsiveness to the needs of participants (buyers and yards). However, some respondents expressed dissatisfaction with the timeliness of project approval. SFF program officers report that it can take one to two months from the initial request for SFF funding to the receipt of the SFF approval. In comparison, Quebec offers a tax credit program for purchasers that can often provide pre-approval (subject to verification) within 24 hours. This is useful because some Requests-for-Proposals require 5-day turnaround times.

These findings echo similar findings from the 2007 evaluation of the SFF. At that time, shipyard and buyer stakeholders also expressed concerns about the approvals process. They noted that the period from bid process to launch in the shipbuilding industry could be up to four years. Some stakeholders believed the slowness of the SFF approval process had a negative impact on the ability of some shipyards to secure contracts.

It is likely that faster turnaround times and earlier interaction in the bid preparation process by the program could facilitate financial calculations and assessments by potential customers. SFF approval prior to loan approval by the financial institution could contribute to more successful bids by Canadian shipyards. This is particularly important because, to date, all projects that have met SFF criteria have received funding.

Revision of Eligibility Criteria

The original terms and conditions for the SFF (2001) had three distinct elements: Interest Rate Support (IRS), Credit Insurance Contribution, and Credit Insurance Support. With respect to the IRS, the maximum non-repayable contribution against overall interest costs on a present value basis was up to 15% of the purchase price of a vessel, with no minimum price required for the shipyard work. When the SFF was renewed in 2007, a requirement for a minimum expenditure of at least $5 million per project funded was introduced.

Five million dollars may be an appropriate figure for a new-build or a significant conversion or refit. However, SFF program staff and other stakeholders suggest the minimum project eligibility amount likely excludes smaller projects that could potentially help maintain capability to meet federal procurement needs. Many of the skill sets and capabilities developed and maintained in smaller projects (i.e., less than $5 million) would likely be relevant in meeting these future needs. In this context, it is worth noting that, among the 30 medium to large-sized shipyards in Canada, only 6 have undertaken projects with SFF funding.

The SFF is designed to act as a bridge to help ensure that Canadian shipyard capability exists to support future NSPS needs. As the requirements for the NSPS become clearer, it will be important to continually update the SFF criteria to ensure that the right kinds of projects are funded.

Issue 12. Could the results have been achieved for a lesser cost?

Finding: The evaluation found that the ratio of administrative costs to total costs, and the project-specific funding contribution level, are reasonable.

The program appears to be effective in leveraging capital for the shipbuilding market. The $18 million in SFF contributions helped shipyards win $134 million in contracts, which represents a 7:1 leveraging ratio.

With respect to overhead costs, the SFF program is managed by a staff of 2.5 FTEs. Operating and maintenance costs represent approximately 6% of total program expenditures. Generally, grant and contribution programs have administrative costs of approximately 8 to 15%, so the SFF O&M costs are quite good. This performance is due in part to the fact that the claims process is fairly simple, as funds are sent to financial institutions to apply to loan/lease interest.

At the current maximum funding level of 15%, there has not been full program take-up. Therefore, it would not seem feasible to consider a lower maximum funding level as program demand would likely drop even further. This assessment is supported by the case studies. For example, Nordane Shipping, a foreign buyer, indicated that the SFF funding level of 15% is the minimum amount of assistance needed to make Canadian shipyards competitive.

4.0 Conclusions and Lessons Learned

The following conclusions and lessons learned are derived from the evidence gathered as part of the evaluation. The lessons learned are presented in the event that the Government allocates new resources to the program or establishes a similar program in the future.

4.1 Relevance

Conclusion:

The SFF is an appropriate role for the federal government and is consistent with departmental and government-wide priorities. There is a continued need for the program to support the shipbuilding industry in Canada until the NSPS is implemented.

In June 2010, the federal government announced a National Shipbuilding Procurement Strategy to develop and implement a long-term approach to shipbuilding procurement to meet federal government needs. In the 2010 Speech from the Throne, the government noted its commitment to support the sustainable development of the domestic shipbuilding industry through a longterm approach to federal procurement. In this context, the SFF is intended to act as a "bridge" to help ensure that Canadian shipbuilding capability exists prior to the implementation of the NSPS.

The issues addressed by the SFF program fall under the overall responsibility of the federal domain, including areas of national security, economic development, and international competitiveness. There is no overlap with provincial jurisdiction and programming.

Evidence suggests that there is a need for the SFF. Canadian shipyards have had limited success in penetrating international markets largely because of price disadvantage. Without SFF funding, Canadian commercial bids would not have been price competitive with foreign shipyards. It is likely that the launch of the NSPS will necessitate a review of the continued need for the SFF.

top of page4.2 Performance

Conclusion:

The SFF contributed to the creation of demand in Canadian shipyards. Whether investments will contribute to ongoing demand is more difficult to assess given that the renewed program has only been in place since 2007. The program helped maintain skilled staff at both medium and large-sized shipyards, and contributed to maintaining and developing shipyard skill levels.

To improve overall performance, the program should consider reviewing the eligibility criteria to ensure that the full range of projects likely to support future needs are eligible for funding. The program should also consider ways to make the project approval process timelier.

The SFF was a key contributor to the current level of shipyard capabilities in Canada. In particular, SFF-funded work supported the retention of skilled staff in both medium and large-sized shipyards.

Evidence suggests that the SFF contributed to the creation of domestic and foreign demand for new-builds, conversions, refits and modifications of ships in Canadian shipyards. The program helped Canadian shipyards remain competitive in international markets, provided significant industry revenues, and, in some cases, was a determining factor in whether projects would proceed in Canadian shipyards.

Given that the program was renewed in 2007 and shipbuilding projects span several years, it is difficult at this stage to determine whether the program has contributed to ongoing demand. However, there is some evidence that the SFF has been successful in this regard. Niche markets have been developed and strengthened in several areas (including cruise ship refitting and tugboat building) in part because of the SFF.

In terms of the program's specific impact on the labour force, project proposals estimated that 1,410 person years of work would be created during this period. Unfortunately, PYs employed and other shipyard data were not systematically collected by the program. As a result, the actual numbers of PYs supported by SFF projects could not be determined. However, there is direct evidence that SFF-funded projects contributed to maintaining and developing new skill levels among workers.

The SFF helped to maintain work volume, which allowed shipyards to implement innovation and productivity improvements. Without the SFF, the pace of these improvements would likely have been reduced.

With respect to program administration, Industry Canada appears to have done an adequate job of promoting the SFF to Canadian shipyards and potential buyers. Overall, the evaluation found that administrative costs for the program and the funding contribution level were reasonable.

In terms of areas for improvement, the evaluation found that potential projects may be lost because SFF approval is not available early in the bid preparation process. The evaluation also found that smaller projects that could potentially contribute to meeting future federal procurement needs do not qualify under the SFF eligibility criteria.

Given these findings, the following lessons learned are presented.

Lesson Learned 1: At the outset of a program, baseline data should be established. This will assist in measuring progress towards the achievement of outcomes.

Lesson Learned 2: The eligibility criteria of a program should consider allowing for the full range of projects that would support policy objectives to be eligible for funding.

Lesson Learned 3: The project approval process should be timely to ensure that bids are not lost due to approval delays.

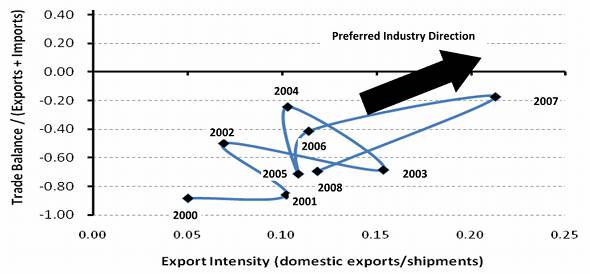

Description of Exhibit 1.4

This figure shows the relationship between Canada's trade balance and the export intensity (domestic exports as a percentage of shipments) for the shipbuilding industry (NAICS 336611) from 2000 to 2008. Overall, it shows that both the trade balance and export intensity increased over the time period. Specifically, the figure shows that in 2000, the trade deficit was approximately 90% while the shipbuilding export intensity was 5%. For 2001, the figures were approximately 90% and 10%. For 2002, the figures were approximately 50% and 7%. For 2003, the figures were approximately 70% and 15%. For 2004, the figures were approximately 22% and 10%. For 2005, the figures were approximately 75% and 11%. For 2006, the figures were approximately 40% and 11%. For 2007, the figures were approximately 20% and 22%. Finally, for 2008, the figures were approximately 70% and 12%.

Description of Exhibit 1.5

This figure shows the value of Canadian exports and imports for the period 2006 to 2009 for various shipbuilding related goods. It demonstrates that exports are relatively minor in terms of value compared to imports with the exception of "other vessels." Specifically for cruise ships, excursion boats, etc. principally designed for the transportation of persons, exports were valued at $53 million while imports were valued at $507 million. For tankers, exports were $1 million and imports were $95 million. For cargo vessels not elsewhere specified and other vessels for the transport of both persons and goods, exports were $3 million and imports were $268 million. For fishing vessels and factory ships, exports were $20 million and imports were $30 million. For tugs and pusher craft, exports were $1 million and imports were $80 million. For dredgers, exports were $15 million and imports were $20 million. For warships, exports were almost non-existent and imports were $1 million. Finally, for other vessels, not elsewhere specified and lifeboats other than rowing boats, exports were $165 million and imports were $26 million.

Description of Exhibit 1.8

This exhibit is a graphical representation of the SFF program logic model. The SFF logic model demonstrates how the program activities are expected to lead to outputs and outcomes.

There are three key activities of the program: market the program; assess and process applications and provide assistance to applicants; and, establish policies and procedures, monitor, measure and report on results. The activity, market the program, is expected to lead to the outputs of marketing documents and a website. These outputs are expected to lead to the immediate outcome that shipbuilders are aware of the program and inform potential owners. This immediate outcome, in turn, is expected to lead to other immediate outcomes that ship owners acquire/modify vessels or offshore marine structures in Canadian shipyards where, without the SFF, they may not otherwise have done so and to the creation of demand for new builds, conversions, refits and modifications in Canadian shipyards. These outcomes are then expected to lead to five intermediate outcomes:

- ongoing demand for new builds, conversions, refits and modifications in Canadian shipyards;

- maintenance or increase in number of direct and indirect shipyard jobs;

- maintenance or development in skill level of shipyard workers;

- development of innovation, adoption of new technology and improvement of productivity in Canadian shipyards; and,

- maintenance of shipbuilding capacity to meet government procurement needs.

Finally, these intermediate outcomes are expected to lead to the ultimate outcome that competitive conditions in Canadian shipyards to cost-effectively meet federal government procurement needs.