Overview

The Canada Small Business Financing Program (CSBFP) is a program that facilitates access to financing to small businesses to start-up, expand and modernize. The CSBFP partners with private sector lenders to provide financing that would not otherwise be available or would only be available under less favourable conditions. Small businesses can obtain term loans of up to $1 million to purchase or improve real property, leasehold improvements and equipment, as well as intangible assets (e.g., copyrights, patents, trademarks) and working capital (e.g., start-up costs). They can also obtain a flexible line of credit of up to $150,000 to help with day-to-day operating costs (e.g., rent, payroll, inventory). Borrowers in all industry sectors (except farming) are eligible as long as they have annual revenues of less than or equal to $10 million. The CSBFP is a national program that operates through a network of financial institutions in all provinces and territories.

The role of the federal government

Innovation, Science and Economic Development (ISED) Canada is responsible for the design and administration of the CSBFP. It reviews and evaluates the legislative and regulatory frameworks and recommends improvements on a periodic basis. It also administers the program by registering loans, collecting fees and paying lenders eligible portions of losses on defaulted loans. ISED, however, is not involved in the disbursement and administration of the loans.

The role of lenders

Private sector lenders are responsible for making all credit decisions, approving and disbursing the loans, registering the loans with the CSBFP and administering the loans. Each lender has its own lending criteria subject to the requirements of the CSBFP. Once the loan is approved, the borrower receives the funds from the lender, not the government. If a loan is in default, the lender must realize on assets taken as collateral before submitting the claim for loss to the CSBFP. Once the lender's information is reviewed and the claim is approved, the lender is paid 85 percent of the net eligible loss.

Highlights

April 1, 2024 marked the 25th anniversary of the CSBFP. Over the years, the CSBFP in partnership with private sector financial institutions has continued to fill an important gap in the lending market. Since its inception in 1999, the CSBFP has facilitated over 200,000 loans to riskier small businesses representing almost $27 billion. The support and collaborative effort of the program, its partners, clients, and stakeholders, have all led to the program's continued success.

In its early years, the CSBFP was focused on facilitating term loan financing to small businesses for the purchase of fixed assets such as equipment and real property. Over the years, through continuous discussions with stakeholders, the program has adapted to the changing economy to meet the evolving needs of small businesses. Today, the program has a broader offering of financing tools which can be used to finance a larger spectrum of assets and expenses including intangible assets and working capital.

Looking towards the future, the CSBFP is committed to continue supporting small businesses by offering relevant and effective financing tools that allow them to start-up, grow and succeed.

Here are some of the highlights from 2023-24.

Lending by value increased to the highest level in CSBFP history

- 6,238 loans were made to Canadian small businesses valued at close to $1.8 billion, the largest value in CSBFP history;

- Compared to the previous year, the number of loans increased by 647 loans (11.6 percent), and the value of loans increased by $282.8 million (19.0 percent);

- The average loan size was $284,089, which represents an increase of 6.6 percent from 2022–23;

- Fee revenues were $98.0 million, which represents an increase of $11.9 million (13.8 percent) relative to the previous year.

Start-ups and new businesses received the largest share of financing

- Start-ups and businesses operating less than one year continued to receive the majority of loans, which accounted for $1.3 billion (73.5 percent).

Leasehold improvements and equipment were the most common assets financed

- Leasehold improvements and equipment loans represented $1.1billion (61.4 percent) and $363.6 million (20.5 percent) respectively;

- Real property loans accounted for $266.2 million (15.0 percent);

- Working capital and intangible asset loans represented $54.2 million (3.1 percent).

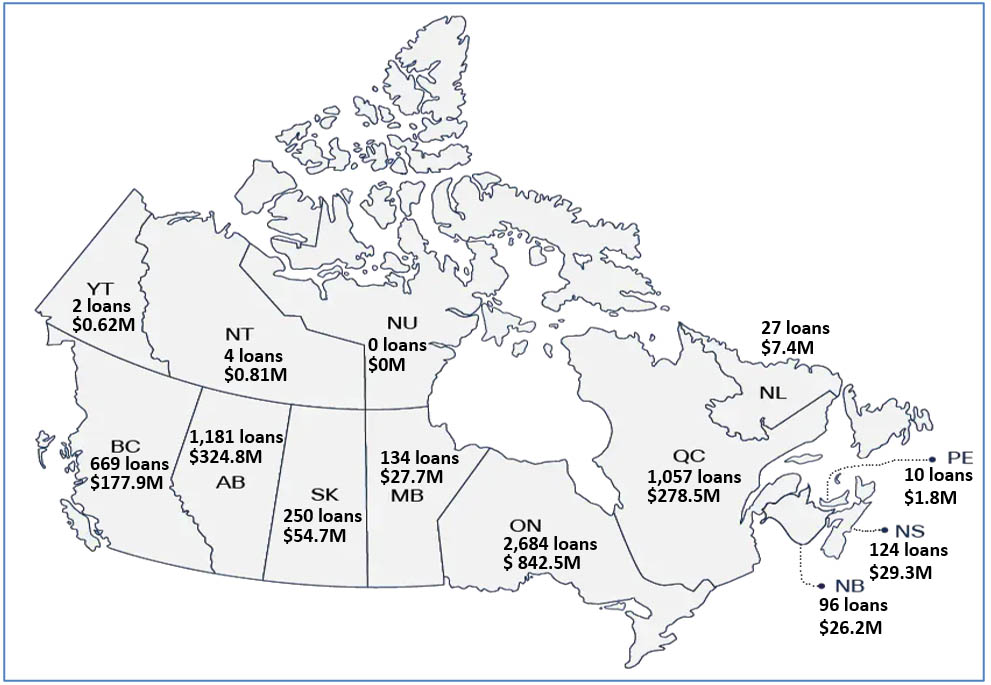

Lending was accessible in every province and territory

Three provinces: Ontario, Quebec and Alberta, represented the majority of overall CSBFP lending in 2023-24, accounting for 4,922 loans (78.9 percent) and $1.5 billion (81.6 percent).

Figure 1 shows lending across all Canadian provinces and territories during 2023-24. The breakdown by regions from highest to lowest volumes is as follows:

- Ontario: 2,648 loans (43.0 percent) totaling $842.5 million (47.5 percent);

- Western Canada: 2,234 loans (35.8 percent) totaling $585.1 million (33.0 percent);

- Quebec: 1,057 loans (16.9 percent) totaling $278.5 million (15.7 percent);

- Atlantic Canada: 257 loans (4.1 percent) totaling $64.6 million (3.6 percent); and

- Territories: 6 loans (0.1 percent) totaling $1.4 million (0.1 percent).

Figure 1: Number & Value of CSBFP Loans by Province and Territory, 2023-24

Number & Value of CSBFP Loans by Province and Territory, 2023-24

| Province or Territory | Number of Loans | Value of Loans ($M) |

|---|---|---|

| Newfoundland and Labrador | 27 | 7.4 |

| Prince Edward Island | 10 | 1.8 |

| Nova Scotia | 124 | 29.3 |

| New Brunswick | 96 | 26.2 |

| Quebec | 1,057 | 278.5 |

| Ontario | 2,684 | 842.5 |

| Manitoba | 134 | 27.7 |

| Saskatchewan | 250 | 54.7 |

| Alberta | 1,181 | 324.8 |

| British Columbia | 699 | 177.9 |

| Yukon | 2 | 0.62 |

| Northwest Territories | 4 | 0.81 |

| Nunavut | 0 | 0.0 |

The CSBFP is open to all industry sectors (except farming) with the majority going to businesses in the accommodation & food services and retail trade sectors

- In 2023-24, accommodation and food services was the largest industry sector using the CSBFP at $859.0 million, representing 48.5 percent of the total value of loans made, followed by;

- The retail trade sector at $253.5 million, accounting for 14.3 percent of the total value of loans, followed by;

- The arts, entertainment & recreation sector at $86.2 million, and the health care and social assistance sector at $73.5 million, representing 4.9 percent and 4.1 percent of the total value of loans made respectively.

Claims increased primarily as a result of elevated interest rates and higher lending amounts in recent years following the COVID-19 pandemic

- The CSBFP paid a total of 876 claims to lenders representing $86.4 million. These claims were associated to defaults on loans that were made during the previous 10 to 15 years;

- The number and value of claims paid increased by 30.4 percent and 30.3 percent respectively compared to the previous year;

- The average claim size was $98,647, which represents a decrease of 0.05 percent relative to 2022-23.

The CSBFP's website, telephone info line and email address were common channels for small business information

The CSBFP website continued to be one of ISED's most popular sites in 2023-24 with 363,360 visits. In addition, 1,679 telephone and 715 email inquiries were received from small businesses and lenders through the program's info line and website. Finally, the program's PDF pamphlet was accessed online 17,842 times.

For more information on the administration and financing activities of the CSBFP, visit the CSBFP website or the Government of Canada's Open data portal.