This report examines the state of the Canadian apparel industry, including its ability to adapt to change to date, its opportunities, examples of success stories and challenges.

- A Canadian Approach to the Apparel Global Value Chain (4.3 MB, 30 pages)

- Permission to reproduce

- 1. Introduction

- 2. Overview

- 3. The apparel Global Value Chain

- 4. Canadian apparel companies and the Global Value Chain

- 5. Moving from "Mediocre" across the Global Value Chain to "World-Class"

- 6. Key challenges in adapting to new models

- 7. Conclusions

- Appendix A: About the 2007 apparel human resources council study 23

- Appendix B: The Canadian apparel industry and specializing within the GVC

- Appendix C: The key success factor index

1. Introduction:

The Canadian apparel industry has long been considered a global player. For years, many Canadian companies have been producing offshore and have seized on preferential access to United States (US) markets to export their products. However until recently, the Canadian apparel industry also operated under protectionism that allowed it to thrive within North America.

In recent years, protectionism has given way to globalization. With that change, Canadian apparel companies have had to compete with imports from low wage countries. Retailers, unencumbered by protectionism, have also seized on the opportunity, often choosing to go directly to offshore manufacturers. As retailers become larger and more globally connected, they continue to build global brands marketed around the world. In doing so, they eliminate many Canadian apparel companies from their supply chain. The result has been major market share declines and job losses in the industry.

The realignment of the global value chain is forcing Canadian apparel companies to reinvent themselves. In certain instances, Canadian apparel companies have capitalized on the environment and become large, global players. However, most of the industry continues to consist of small and medium-sized enterprises (SMEs), struggling to deal with globalization. Many of these organizations must shift from being production-driven to being market-driven. They must shift from being mediocre across the entire value chain to being specialists in market niches, product niches and value added service niches.

2. Overview

2.1 Industry profile (2006)

According to 2006 Statistics Canada data, the Canadian apparel industry accounts for:

- 1.4 percent of manufacturing gross domestic product;

- 1.2 percent of manufacturing investment;

- 3.3 percent of manufacturing employment; and is the

- 19th largest manufacturing sector in Canada.

The industry is highly fragmented:

- Apparel is manufactured in all provinces and territories. While Quebec accounts for 61.3 percent of the value of Canada's apparel production, other key areas include Ontario, Manitoba and British Columbia;

- Approximately three quarters of firms have fewer than 50 employees.

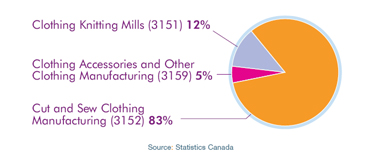

Most companies are however classified as cut and sew manufacturers:

Figure 2.1: North American Industry Classification System (NAICS) Classification of Apparel Companies, 2006 Manufacturing Shipments (Percentage of Total Apparel Shipments)

Source: Statistics Canada

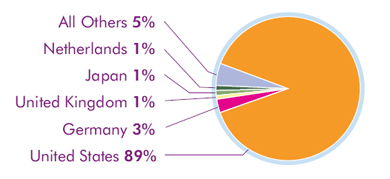

In 2006, 31.5 percent of Canadian apparel was exported, with the vast majority destined for the US:

Figure 2.2: Destination for Canadian Clothing Manufacturing Exports, 2006 (Percentage of Total Apparel Shipments)

Source: Apparel & Textiles Directorate, Service Industries and Consumer Products Branch, Industry Canada, and data from Statistics Canada

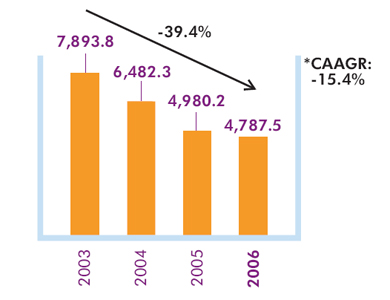

2.2 Declining trends

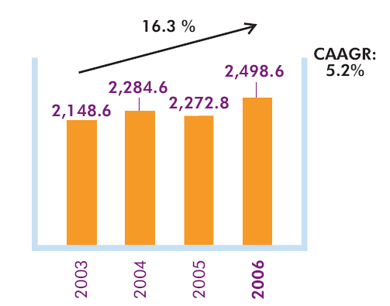

Apparel manufacturing in high wage countries has suffered in recent years and Canada has been no exception. Since 2003, Canadian apparel manufacturing shipments have declined by 39.4 percent:

Figure 2.3: Canadian Clothing Manufacturing Shipments, 2003–2006 (Millions of Canadian Dollars)

Source: Statistics Canada, CANSIM

* Compound Average Annual Growth Rate (CAAGR)

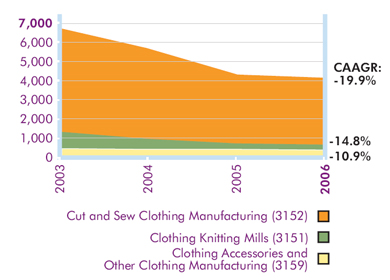

This decline is occurring in all three sectors:

Figure 2.4: Canadian Clothing Manufacturing Shipments by NAICS, 2003–2006 (Millions of Canadian Dollars)

Source: Statistics Canada, CANSIM

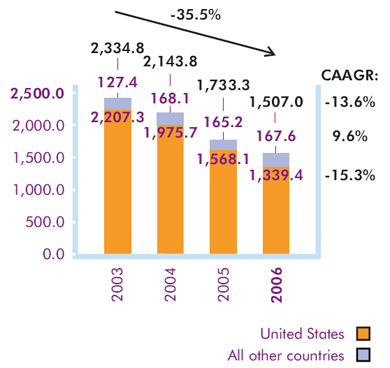

While manufacturing shipments have been declining, imports have been increasing:

Figure 2.5: Total Clothing Imports into Canada, 2003–2006 (Millions of Canadian Dollars)

Source: Statistics Canada, World Trade Atlas

China continues to be the largest source of import increases:

| Market Share of Imports | Percentage Change | |||

|---|---|---|---|---|

| Country | 2004 | 2005 | 2006 | 2004-2006 |

|

Source: Statistics Canada, World Trade Atlas |

||||

| China | 38% | 47% | 50% | 52% |

| Bangladesh | 7% | 7% | 7% | 9% |

| United States | 9% | 7% | 7% | -18% |

| India | 6% | 6% | 6% | -2% |

| Mexico | 6% | 5% | 5% | -4% |

| Italy | 3% | 3% | 2% | -16% |

| Indonesia | 2% | 2% | 2% | 23% |

| Cambodia | 2% | 2% | 2% | 7% |

| Vietnam | 1% | 2% | 2% | 103% |

| Turkey | 2% | 2% | 2% | 6% |

| All others | 23% | 17% | 15% | -22% |

| Total | 100% | 100% | 100% | 15% |

As a result of increasing imports, Canadian apparel manufacturing shipments destined for the domestic market have been in decline:

Figure 2.6: Canadian Clothing Manufacturing Shipments for the Domestic Market, 2003–2006 (Millions of Canadian Dollars)

Source: Statistics Canada, CANSIM

Faced with similar threats, Canadian apparel manufacturing exports to the US have also been in decline. However thanks to new initiatives, gains are being made in other fledgling markets:

Figure 2.7: Destination for Canadian Clothing Manufaturing Exports, 2003–2006 (Millions of Canadian Dollars)

Source: Statistics Canada, World Trade Atlas

As a result of rising imports and declines in manufacturing shipments destined for the two major markets (Canada and the US), employment has decreased dramatically:

Figure 2.8: Canadian Clothing Manufacturing Labour Force, 2003–2006 (Employees in Thousands)

Source: Statistics Canada, CANSIM

2.3 Recent underlying industry challenges

The industry has been hit hard by a series of factors, largely emanating from trade liberalization and retail industry restructuring.

Major trade liberalization initiatives include:

- The removal of import quotas in accordance with the World Trade Organization Agreement on Textiles and Clothing which commenced in 1995 and was fully implemented by January 1, 2005. This agreement opens the Canadian textiles and apparel industries' previously protected two major markets (Canada and the US) to low wage imports;

- Concessions to Least Developed Countries, which allow for duty and quota free imports for textiles and apparel produced in 48 countries (including Bangladesh, Cambodia, Laos and Haiti) effective January 1, 2003;

- The pending termination of the Duty Remission Program on December 31, 2009.

Beyond trade liberalization, retail industry restructuring has also challenged the industry:

- Massive retail consolidation has lead to fewer, larger more powerful retailers. These larger retailers have been:

- Augmenting their global sourcing capabilities, thereby increasingly going directly to offshore factories and eliminating Canadian apparel suppliers from the supply chain;

- Building global brands which often exclude Canadian apparel suppliers;

- Developing their own private label lines rather than supplier controlled brands, thereby reducing supplier profitability and supplier importance to the retailer and consumer;

- Exerting tremendous price and performance pressures on traditionally smaller Canadian apparel companies;

- At times, prescribing "allowable" profit margins to manufacturers;

- Increasingly refusing to take inventory risks, demanding that manufacturers produce shorter runs with shorter lead times;

- Increasingly levying charge-backs on suppliers, requiring payments for a percentage of the cost of unsold product, whether or not the item is returned to the supplier;

- Requiring sharing in advertising costs (co-op advertising) and other discounts such as volume rebates or new store opening discounts;

- In order to compete with large retailers, mid-size retailers are adopting some of these practices as well;

- Highly focused, retail specialty channels are gaining market share at the expense of department stores (which were traditionally important customers to many Canadian apparel companies);

- Smaller, independent retailers, a sector of the channel that must rely on domestic suppliers, are declining as they lose market share to larger, more sophisticated retailers;

- The rise of discounters such as Wal-Mart, are placing greater price pressures on many apparel sectors;

- The retail trend toward "fast fashion" (whereby in certain sectors, the typical two season year has been replaced with new monthly fashion requirements) is putting tremendous performance pressures on certain Canadian apparel companies;

- Retail and consumer pressures to produce garments in "sweat shop free" premises around the world is requiring that many companies implement stringent measures and certification programs to remain in the supply chain;

- Retailers are generally pressuring manufactures to provide higher quality products at lower prices;

- Retailers are demanding more innovative, differentiated products specific to their target markets.

These factors along with other economic conditions (such as a strengthened Canadian dollar and US border controls) have placed tremendous challenges on the Canadian apparel industry. These factors have together triggered a global battle for competitiveness which will continue to evolve. While low wage functions have largely moved to cost competitive countries, the battle for other value added services is likely to ramp up around the globe.

3. The apparel Global Value Chain

The product design step includes a wide array of activities ranging from researching new fabrics and styling trends to the creation of new designs, patterns and samples. Depending on the nature of the product, designs can be driven by fashion trends or by the need for functional innovation and performance. Regardless of the product, extensive end consumer and market trend knowledge must usually be conducted, requiring frequent travel to and research of foreign markets. Many sectors produce seasonal lines and as a result, companies are continuously in a design phase.

The apparel supply chain can be broken down into three major industrial segments:

Figure 3.1: Apparel Supply Chain Segments

The value chain of a traditional apparel company can be broken down into a series of key steps as follows:

Figure 3.2: Apparel Industry Value Chain Segments

3.1 Product design

Key elements often include:

- Market research to understand consumer behaviour and market trends. This includes all forms of intelligence gathering and analysis in order to determine items most likely to sell. This research is used to predict and understand the next fashions, fabric trends, colours, styles, price points, retail requirements, competitive forces and other sources of innovation. Frequent travel and research of foreign markets is often required. Information gathered at this stage adds to the design direction and inspiration;

- For performance products, Research and Development (R&D) is undertaken in order to improve the functional performance of a product. This often requires using focus / user groups, having close integration into new input innovations and integrating experimental production techniques and test user groups;

- Design, using hand sketches, off-the-rack garments, technical drawings, three-dimensional draping on dress forms, or computer-aided design (CAD) to create new concepts and samples;

- Selecting fabric from global sources taking into account factors such as fabric attributes, performance requirements, pricing and availability in proper quantities;

- Pattern making to reproduce a designer's sample pattern into all the properly sized pieces in order to make a complete garment;

- Grading to replicate the patterns into all the proper sizes required. Manufacturers create their own sizes, which although similar, may differ between companies. Sizes may also change over time to keep in line with changing consumer needs and marketing requirements;

- Marking to decide how to cut the fabric as efficiently as possible. This process entails maximizing the number of pattern pieces that can be cut out of a piece of fabric while minimizing waste;

- Merchandising to estimate the number of products to produce by product category, style and size as well as to help estimate required production delivery dates. In certain instances, merchandising may simply refer to putting together a collection for a specific retailer based on imports from a variety of suppliers (e.g. an outsourced buyer);

- Costing of each garment taking into account potential sales volumes and sizing requirements. Decisions must be taken as to where to manufacture the item, with possibilities often including a multitude of offshore factories in various countries, in-house domestic facilities or domestic contractors. The decision must take into account factors such as volume, quality, price, reliability, delivery requirements and international trade laws.

Samples are then produced and a portion of these designs are accepted into the line. These accepted samples are shown to potential buyers. Based on market acceptance, only those styles deemed successful will be entered into the line for production.

3.2 Manufacturing

Manufacturing generally encompasses many processes often performed by semi-skilled labourers. Key steps typically include:

- Inspecting fabric to ensure that it meets specifications. Tests are often performed to measure product attributes such as shrinkage, colour adherence, durability, consistency, etc. Irregularities must be detected early in the process to avoid further production waste and delays;

- Spreading to unroll rolls of fabric onto long tables in preparation for garment production;

- Cutting the spread fabric in accordance with the markers order to produce pieces of garments;

- Bundling or reorganizing cut pieces according to production lots grouped by garment unit, colour dye lot and number garments;

- Sewing or assembling item pieces in order to construct a finished garment;

- Pressing or folding to iron a garment. This is usually conducted after the garment has been fully sewn;

- Finishing or adding specific details to a garment. Examples include screen printing, embroidering and adding buttons trims. Loose threads are usually clipped at this point as well;

- Dyeing and washing can be conducted early or late in the process depending on the garment. For some items, dyeing washing is done after the finishing process in order to ensure perfect colour match for coordinates;

- Quality control to ensure that each element of production completed as intended. Errors must be found as early as possible in order to minimize rework and waste. While quality control involves inspecting units produced, quality assurance refers to the process of ensuring that adequate processes place to prevent production errors in the first place. This often entails manufacturers visiting suppliers to ensure that future shipments will conform to specifications;

- Ticketing and bar-coding price tags onto garments and packages or placing items on hangers according to customer specifications. These requirements often differ amongst customers.

Many of these tasks are highly labour intensive, with much of the costs emanating from the sewing and assembly operations. These tasks can typically be done by semi-skilled operators. As a result, these manufacturing tasks can often be outsourced to low wage environments when conditions are appropriate.

3.3 Marketing

The level of marketing requirements often varies with the business model being deployed by a company. It can be virtually non-existent or it can be the main driver of competitive advantage.

The marketing department is typically responsible for:

- Assisting the design team to understand market trends, end consumer profiles, changing market needs and new opportunities;

- Developing programs to keep brands fresh and relevant to the end consumer;

- Monitoring competitor activities and providing input on product prices, styling, etc;

- Developing and implementing promotional or public relations campaigns aimed at retailers or end consumers;

- Organizing product launches;

- Identifying sales leads and new channels of distribution;

- Developing pricing and in-store promotion strategies to encourage retailer and consumer purchases.

3.4 Securing clients

The process of securing clients generally involves:

- Travelling to meet new and existing customers;

- Merchandising the line to customers by demonstrating product unique attributes or selling features;

- Coordinating potential sales leads with accounting personnel to ensure credit worthiness;

- Working with Production and Distribution departments to ensure delivery requirements can be met;

- Providing retailer and consumer feedback to Design and Marketing departments to assist in future product development and marketing activities.

These functions are at times performed by in-house sales personnel. When companies limit sales functions to pure order taking, these functions are often outsourced to non-exclusive, commission-based sales agents. In some organizations, the sales process can extend into company-owned retail or other direct to consumer models whereby the manufacturer sells directly to end consumer. While these direct to consumer models are often established as a means of clearing end of season products, other companies have made selling to the consumer a core part of their business.

3.5 Logistics and distribution

The logistics department is involved in the import and export of goods. Key tasks include managing matters such as:

- Duties;

- Customs;

- Arrangements with transportation companies.

The distribution department is responsible for:

- Packaging finished goods according to customer specifications (in some cases, these specifications may vary for each customer);

- Ensuring the right goods are shipped to the correct location on time.

Global supply chains and shorter cycle time requirements have added complexity to these tasks through the need for increased communication skills, computerized tracking and inventory control systems.

3.6 Servicing

The service aspect of the value chain pertains to a company's ability to provide a unique service that allows it to differentiate from the competition. Examples include:

- Rapid replenishment services;

- Allowing for the ordering of very small quantities;

- Customized orders;

- Progressive customer service policies such as liberal returns, exchanges, consignment, inventory buy-back programs, etc.

3.7 Strategic implications

The apparel value chain model highlights the fact that as the apparel industry continues to be globalized, opportunities and challenges exist for Canadian companies. As we have clearly seen since the final phase of quota removal on January 1, 2005, Canadian companies have faced cost competitiveness challenges in the area of "cut and sew". As a result, they have suffered significant market share losses in their two major markets, Canada and the US.

While the retail sector continues to be dominated by large players, trade liberalization has accelerated the race to find low cost global producers. Some industry analysts project that this will lead to further massive supply consolidation, whereby mammoth factories in low wage countries will directly supply retailers, thereby cutting out inefficient, non value-added middlemen. If such a scenario was to play out and Canadian companies were not to adapt, the results could be devastating to the local industry.

Fortunately, the global value chain model highlights the many complex elements of the apparel industry (i.e.: product development, innovation, market research, trend identification and setting, understanding of niche markets in Canada and the US, highly educated workforces, marketing talent, etc.). While Canadian companies may not be well positioned as cost competitive manufacturers, in many respects, they should be better poised to take advantage of these other opportunities than low wage competitors.

As a result, the future of the Canadian apparel industry lies in the global disintegration of the industry, as opposed to its consolidation. This disintegration of the value chain is well documented in other industries that have already gone global. Consider:

- Many of the world's largest automotive companies outsource their car designing to specialty firms. The list includes such famous brands as FERRARI, ALFA ROMEO, ROLLS ROYCE, FIAT and HONDA. These world leaders have clearly recognized that a firm that purely specializes in leading edge design can outperform a company that it trying to do everything;

- Pharmaceutical companies often rely on small bio-tech companies to conduct R&D into new medications. They also outsource production to large producers with massive economies of scale. In doing so, many pharmaceutical companies tend to focus on the selling and marketing aspect of the global value chain. Once again, the industry has learned that companies designed for a specific purpose can outperform a company that is trying to do everything;

- Computer companies tend to specialize in niche markets. MICROSOFT focuses on software, IBM spun off its manufacturing arm so that it could refocus on service. DELL refocused to be a leading distributor.

While the Canadian apparel industry has been slow to adapt to such models, the message is not being lost on some of the world's leading apparel companies based in high-wage countries. Consider the case of ADIDAS:

ADIDAS was founded in Germany in 1949. While under family management, the company focused on manufacturing and sales. As imports from low wage countries began to grow, the company was on the verge of bankruptcy. In the 1990s, family management gave way to a new CEO and the company made a comeback by realigning its global value chain. Today, ADIDAS is a world leader in footwear and sports apparel by being focused on design and marketing.

In the area of design, ADIDAS has two major focuses: innovation and fashion. With respect to innovation, ADIDAS targets at least one major new technology or technological evolution per year. The company employed over 630 people in its R&D department in 2005, an increase of 7 percent over the prior year. This team engages in long term projects with well established global research partners such as the Faculty of Kinesiology of the University of Calgary, Canada, the Institute of Sport and Sport Science of the University of Freiburg, Germany and the Sports Technology Research Group of the University of Loughborough, England. In addition, ADIDAS consults with both professional and recreational athletes during the design and development process to improve functionality, comfort and design.

Beyond its own world-class R&D facilities, ADIDAS has entered into strategic alliances with companies such as Design (to develop a new high-tech premium brand) and (to integrate heart rate, speed and distance monitoring equipment into apparel and footwear). With respect to fashion, ADIDAS has entered into a strategic alliance with Stella McCartney, a high-end fashion designer, create a functional sport performance range for women.

The second value chain focus of excellence for the company marketing. In this respect, ADIDAS heavily pursues promoting its brand at world class sporting events such Olympics, World Cup Soccer and other professional sports. Top athletes wear ADIDAS innovations and in turn, their success further promotes the company. For example, ADIDAS achieved record sales at the 2006 FIFA World Cup soccer event, selling 3 million replica jerseys.

Manufacturing is no longer core to the internal operations the company. The vast majority of products are produced independent manufacturers. In 2005, 78 percent of ADIDAS apparel was produced at independent factories in Asia. This new strategic focus has served ADIDAS well. The company achieved or surpassed key financial targets in including achieving currency neutral sales growth of 12 percent; gross margins at record levels in excess of 48 percent; and earnings 22 percent of sales, its highest ever.

The company will continue to pursue the strategy and integrate its 2006 purchase of Reebok into its operations.

Even though ADIDAS has been in existence for nearly 50 years, strong new competitors can grow and be successful. The industry such that not only can turnarounds be implemented, but entrants can quickly gain market share and become global players. Consider the case of UNDER ARMOUR:

UNDER ARMOUR was founded in 1996 by a former University of Maryland football player. The company focused on making a superior T-shirt; one that would provide compression and wick perspiration off the skin rather than absorb it. It was designed to regulate body temperature and enhance performance.

The Company now engineers gear to keep athletes cool, dry and light throughout the course of a game, practice or workout. Its mission is to provide the world with technically advanced products engineered with superior fabric construction, exclusive moisture management, and proven innovation.

The Company went public in 2005. In less than 10 years, it has achieved annual sales in excess of US$281 million and annual net income approaching US$20 million. It employs over 600 people, mostly in the US.

Similar to ADIDAS, UNDER ARMOUR focuses on performance innovation. It sources fabric innovation from third party fabric producers who maintain patents over the materials. UNDER ARMOUR then uses these fabrics to develop new products and patent them when appropriate.

Virtually all manufacturing is outsourced to unaffiliated producers who source the fabric directly from approved suppliers and ship finished products. A small 17,000 square foot "special makeup shop" is maintained in Maryland in order to provide a limited number of products on a rush basis to high profile athletes and teams.

Products are now sold worldwide through over 8,700 retailers.

Marketing is driven by focusing on the next generation of athletes and top prospects who wear and promote the brand. The company also sponsors grassroots sporting events.

Other examples abound in the global apparel world of niche players focusing on areas such as fashion design, lifestyle marketing, niche specialization, etc. New fashion brands are constantly appearing. New market niches are constantly developing. New products are constantly being brought to market. Consider the cases of AMERICAN APPAREL and CROCS:

AMERICAN APPAREL—founded in Los Angeles by former Montrealer Dov Charney with one retail location in 2003 selling casual clothes for men, women and children. Within just three years the company has expanded to 143 countries. Sales for 2006 were an estimated US$300 The Company's 80 percent gross margin is well above the industry average of 60 percent. It produces and sells unbranded, brightly coloured and moderately priced T-shirts, underwear and jeans. Unlike many other vertical retailers, of the 4,000 workers involved in AMERICAN APPAREL's manufacturing process work in the same factory in Los Angeles. This model allows the company to design produce fast fashion and maintain control over every production. The company has recently gone public plans to open an additional 65 stores worldwide.

CROCS—founded recently in Denver, Colorado, manufactures colourful slip-on shoes that have gained popularity in the watersports arena and in mainstream fashion. shoes, sold under the CROCS brand, are made of closed-cell resin and are known for their comfort. operates manufacturing facilities in China, Mexico, Canada (in Quebec City, which accounts for approximately 17 percent of production). In 2005, the company recorded sales of US$109 million (703 percent increase over the prior year), US$17 million net income and employed over 1,130 people.

As these examples show, when industries go global and consolidation occurs, substantial opportunities for SMEs through specialization. Opportunities for new models abundant, not in creating or trying to compete against mammoth one-stop shops, but by creating well defined areas of specialization that offer a unique, world class, value added product. seen from these examples, this can take the form of product, lifestyle and/or functional specialization.

The key then is to focus by channelling energy and resources becoming world class in a chosen area. Realistically for SMEs, this means redirecting funding to this new core competency by reducing investments in non-core elements competitive advantage does not exist and cannot be doing so, Canadian apparel companies can in fact against the world's best and play integral roles in global chains. And when considering that Canada has less than share of the US apparel market, these models offer tremendous growth opportunities.

4. Canadian apparel companies and the Global Value Chain

4.1 Acceptance of GVC Models in the Canadian Apparel Industry

Canadian companies have unfortunately been relatively slow in adapting to the global value chain model of specialization. Instead, many have retained their traditional models of performing all tasks across the value chain in a mediocre fashion while serving a wide, often unfocused target audience. Such positionings leave companies exposed to world class competitor specialists.

The Apparel Human Resources Council's 2007 Apparel Strategic Benchmarking Report (2007 AHRC Study—see Appendix A for study background information) documented this lack of focus from several different vantage points:

- Participating companies demonstrated a lack of focus on having a narrow customer niche. Nearly 40 percent of participants reported targeting three or more age categories. Only 22 percent reported selling to one age category;

- While many companies have proceeded to shift manufacturing to low wage countries, most continue to consider all other areas of the value chain as being a part of their core internal competencies, choosing to not outsource or partner with other players to improve competitiveness;

- Most retailers view their Canadian apparel suppliers as being mediocre performers across the value chain.

These issues are described in detail in Appendix B.

Clearly however, some Canadian apparel companies can excel in today's environment. But in order to take part in global value chains, many Canadian apparel companies must improve in a wide array of areas. The following section defines these areas by comparing some of "the best" from "the rest".

4.2 Improving Chances of Success: The "Best" Versus "The Rest"

After having worked with 130 apparel companies, the 2007 AHRC Study documented a Key Success Factor (KSF) Index in order to help identify the most salient factors driving success. Twenty five key factors were identified and grouped under five major building blocks. This index is reproduced in Appendix C.

A weighting system was developed to assign relative importance for each building block and attribute, resulting in a weighted average index out of 100. Participating companies were scored against this index.

The average score for all participating companies was 54/100, or 54 percent. In contrast, the most profitable companies (measured as earnings as a percent of revenues) scored in excess of 80/100 or 80 percent. These top scoring companies have seen sales grow in the last four years at quadruple the rate of the average company and are nearly three times as profitable.

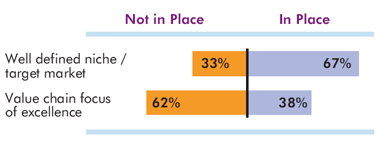

Ten key factors were subsequently identified as differentiating "the best" from "the rest". "The best" were clearly superior in the following areas:

Table 4.1: Apparel Company Ten Key Success Factors

Key Success Factor:

- Having the "operational and financial basics" right

- Having a clear understanding of financial profit drivers

- Having a strong management team

- Having a history of implementing change proactively

- Being in a well defined niche or target market

- Having a value chain focus of excellence and differentiation

- Having growth opportunities

- Being in a sector of low to medium competitive intensity

- Having a corporate culture that is open to change

- Having a willingness to reinvest in the company

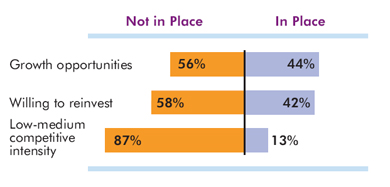

Many of "the rest" fell short in these areas. Some shortcomings relate to the quality of their positioning:

Figure 4.1a: Percent Of Companies With and Without Key Attribute in Place

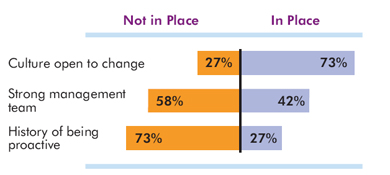

Other shortcomings were caused by human resource challenges...

Figure 4.1b: Percent Of Companies With and Without Key Attribute in Place

Some shortcomings pertain to operations and finance...

Figure 4.1c: Percent Of Companies With and Without Key Attribute in Place

And for many, the root cause of not excelling remained in their lack of having a differentiated focus area of the value chain:

Figure 4.1d: Percent Of Companies With and Without Key Attribute in Place

The findings highlight that many companies suffer from shortcomings in key human resource and professional management skills. While most companies are niched, they still do not offer the customer anything differentiated or better than the competition despite all the possible areas of value chain focus.

5. Moving from "Mediocre" across the Global Value Chain to "World-Class"

By moving from "mediocre" to focused "excellence" Canadian apparel companies can be globally competitive, allowing them to compete head on against strong competitors and to provide specialized services to other global players. Beyond getting the operational basics right, this will generally require mastering the other issues in the KSF Index, while paying particular attention to:

- Selecting viable niche markets;

- Focusing on the US market;

- Having a strategic area of focus within the value chain.

5.1 Selecting viable niche markets

In order to succeed, many apparel companies will have to focus on product niches. In doing so, companies can:

- Develop products that are better designed for the market;

- More cost effectively develop marketing programs that are highly targeted towards a narrow audience.

Examples of some well product-niched Canadian companies include:

- LIJA—Vancouver-based designer and marketer of stylish, feminine women's golf apparel. Designs are fashion forward and can be worn on and off the golf course, allowing the wearer to easily transition from one activity to the next. The line is sold through golf club pro shops across North America. The Company was recognized by Business in Vancouver as one of British Columbia's 50 Fastest Growing Companies and named one of Canada's Fastest Growing Companies by Profit Magazine.

- SILVER JEANS and PARASUCO—Winnipeg and Montreal-based designers and marketers of fashion jeans. Both companies target a youthful market and focus heavily on understanding the end consumer. Both sell throughout North America as well as certain Asian and European countries. PARASUCO also continues to expand its company owned retail stores with locations in Montreal, Toronto, New York, Vancouver and Los Angeles.

- MATT & NAT—Montreal-based designers and marketers of vegan handbags. Products are all manufactured from synthetic leathers, incorporating both the leading edge designs and the quality of high fashion leather handbags. The product thus appeals to fashion forward individuals who care both about the environment and products that are manufactured without harming animals. Products are sold throughout North America as well as certain European countries.

- CREATIVE EDUCATION OF CANADA—Ontario-based designer and manufacturer of children's creative costumes. Costumes are designed to be flexible in sizing and reversible to another costume, thus improving value for money. The costumes are designed to encourage creative play and inspire the imagination. Products are sold largely through specialty toy stores across North America.

- BRAVADO DESIGNS—Toronto-based designer and manufacturer of specialty maternity bras. The Company focuses on designing practical, stylish maternity and nursing bras. It aims to provide highly functional products while enhancing a mother's self image. Its products are sold throughout North America (largely through specialty stores and hospital boutiques) and parts of Europe and Asia.

Canadian companies can also focus on niches where the global reputation of Canada could be of assistance in branding and marketing. For instance, apparel companies could focus on designing and exporting superior winter outerwear, military high tech uniforms, oil and gas uniforms, resource uniforms; west coast lifestyle wear, etc. Consider the cases of:

- INTEGRAL DESIGNS—Calgary-based designer and manufacturer of high-end extreme mountain climbing outer wear and survival wear. Products are developed according to world-class search and rescue specifications as well as the unique needs of high-end mountain climbing enthusiasts;

- ARSON & ORB—Vancouver-based designers and marketers of west coast street wear apparel. The clothing is inspired by board sports, music, art and activism. Designs are a microcosm of the west coast youth lifestyle. The brand names are well known within their niches and are cross branded onto other accessories. Products are sold internationally (e.g. Austria, Switzerland, Czech Republic, Germany, United Kingdom, Italy and Russia) as the Company exports its alternative west coast lifestyle.

5.2 Targeting the US market

Exports will clearly play a vital role in the future of the industry:

- As Canadian companies continue to seek out niche markets, is apparent that the domestic market is too small to support many such models. This will continue to force companies to look elsewhere;

- Canadian companies that become world class specialists will, definition, be able to expand their businesses to foreign markets.

While some industry experts believe Canadian apparel companies must increase their exports to countries in Asia and Europe, Milstein & Co Consulting Inc. believes that the key to success continues to remain primarily in the US for the following reasons:

- There is significant room for growth as Canadian apparel companies have less than 1 percent share of the US apparel market;

- The US market remains the most similar to that of Canada's. As a result, it is most easily understood by Canadian executives. This market knowledge is critical in order to understand niche opportunities and areas of competitive differentiation;

- While border security remains a major issue, proximity of the market still allows for effective selling and servicing, including rapid replenishment models with minimal additional overhead costs compared to other export markets;

- The US dollar decline compared to the Canadian dollar appears to have stabilized. Given the declines in recent years, is unlikely that the US dollar will suffer additional major declines in the coming years. Canadian apparel companies that are competitive at current levels could likely withstand future minor fluctuations.

By contrast, we believe that Asia and Europe should be typically looked at once a company has established itself as highly profitable in North America for the following reasons:

- Selling to Asia and Europe generally requires the injection of additional distributors as Canadian companies tend to be unfamiliar with foreign markets and distribution channels. A Canadian company must therefore be highly profitable before it can afford to add this additional layer of overhead;

- Canadian companies do not tend to understand foreign markets, niches and end consumers as well as they understand North American sectors, thus making it much more difficult to compete for these foreign niches;

- An exception to this principle exists when a Canadian company is exporting a lifestyle niche or known expertise that is sought by the foreign market (e.g. exporting Vancouver lifestyle street wear or yoga wear, Canadian winter outerwear, etc.).

5.3 Selecting a strategic area of focus within the value chain

The value chain model highlights a series of complex business processes where differentiation and hence competitive advantage, can be created in many different means irrespective of the country where goods are manufactured. By focusing on the value chain, companies can differentiate by doing something better than competitors or by doing things differently than competitors. As illustrated in our 2007 AHRC Study, companies can differentiate by doing things better or differently in any of these areas:

Table 5.1: Possible means of differentiation across the value chain

Value chain focus

Possible means of world-class differentiation

Design

Superior fashion or technical design based on one or more of the following:

- Sheer creative ingenuity

- Functional innovations

- Carefully constructed, world class design processes

Manufacturing

Superior manufacturing capabilities through:

- Low cost global manufacturing capabilities

- Fast and flexible local production

Marketing

Strong focus on:

- Mass branding

- Niche branding (functional or lifestyle based)

- Licensing

- Private label

Sales / Service

Strong focus on:

- New regions

- New products

- Service policies

- Selling to discounters

- Selling to majors

- Selling to independents

- Selling to specialty stores

- Selling to institutions / corporations

- Alternative retailing / direct to consumer / home shopping

- Conventional retailing

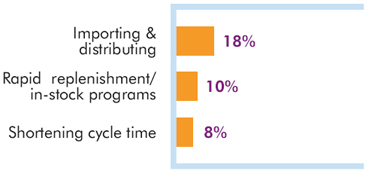

Distribution

Strong focus on:

- Importing and distributing

- Rapid replenishment / in-stock programs

- Shortening cycle time

5.4 Crafting a globally competitive strategy: Canadian apparel examples

In constructing valid strategic business models, companies must combine strengths / differentiating factors in more than one area of the value chain for as a strategy becomes more complex, likelihood of differentiation increases and attempts to copy are inherently discouraged. In doing so, apparel companies can carve out strong competitive positions in highly focused markets. Consider the following examples of strategies crafted in this manner, many of which were originally identified in the 2003 AHRC Labour Market Update Study (2003 AHRC LMU—see Appendix A for background information) or the 2007 AHRC Study:

Strategy # 1: Lead thanks to world-class design and niche branding

A company could focus on the design function by becoming world class in design and building a brand in a niche market. This is a strategy that can be realistically pursued for instance in the men's apparel segment where innovative design is valued.

The key success factors in this case will be having an innovative design team, the ability to direct and control a quality manufacturing program and good relations with specialty stores focused on the niche market.

This is the strategy pursued by Montreal-based ZENOBIA COLLECTIONS. The company has developed its own highend women's wear brand, through its strong design capabilities. The highest quality fabrics are sourced globally and the garments are manufactured locally in order to maintain high quality standards. Its select customers search for and are prepared to pay for top quality and fashion. The collection is sold at select high-end US retailers and through trunk shows and other direct to consumer avenues in order to reach and properly service its niche target market.

Strategy # 2: Create a lifestyle brand and sell to majors

Another strategy might consist of creating and sustaining a very strong brand, in essence, creating a lifestyle brand. In its extreme form, the company can become a brand licensing company, licensing its name to different apparel categories and outsourcing all other functions. Here the focus is in creating a brand, and having a strong sense of style. Companies that have pursued this strategy include Tommy Hilfiger, Calvin Klein and Ralph Lauren.

TOMMY HILFIGER has created a strong brand name and brand recognition where products are now synonymous with all around sophistication. Its name conveys the image of fun, youth and diversity in the global marketplace. It uses this name to market men's, women's, children and even home products, getting a premium price for a premium product sold under its brand name. Advertising and promotion are a cornerstone of their success as the company spends over 41 percent of its net revenues on advertising to specific, targeted demographic groups.

A similar Canadian example could be POINT ZERO. Founded in Montreal in 1979, POINT ZERO designs and markets fashionable men's, women's and children's coordinated sports and street wear. The Company has a team of 17 designers who travel the world to unearth the next big trend. The design team is supported by an in-house staff of graphic artists and pattern makers using the latest in computer systems to produce the lines. In addition to its fashion sense, a large part of the Company's success is due to having a strong price quality price ratio.

Having established a name in the clothing market, POINT ZERO also licenses eye wear, shoes, clothing, handbags, knapsacks, watches, belts, head wear, gloves, socks, yoga wear and a new line of various household products. The Company also intends to expand its licensing into fragrances, lingerie, towels, jewellery, lamps, tabletop accessories, etc.

POINT ZERO has offices and showrooms in Montreal, New York and Los Angeles. It does not operate its own stores, preferring to sell through traditional retail channels from small boutiques to large department stores across North America.

The Company recently enlarged its storage and shipping facilities in Montreal and Los Angeles, and is building a state of the art merchandising and distribution centre in Montreal.

Strategy # 3: Become an Integrated Apparel/Retail Company

A company can decide to be strong in 3 elements of the value chain by having innovative design, marketing capabilities with a strong brand identity and directly controlling the selling by owning or franchising its stores. This is the strategy pursued by GUESS, INC., which designs, markets, distributes and licenses one of the world's leading lifestyle collections of contemporary apparel, accessories and related consumer products, such as watches, jewelry and eyewear.

GUESS employs an in-house staff of three design teams (men's, women's and GUESS Collection) based in Los Angeles. Design teams travel throughout the world to monitor fashion trends and discover new fabrics. The teams regularly meet with members of sales, merchandising and retail operations to further refine the products to meet the particular needs of the market. The company also maintains a fashion library consisting of antique and contemporary garments as another source of inspiration.

Marketing is another strength of the company, as it consistently promotes a strong brand image that stands for a quality, trendsetting lifestyle. Advertising campaigns promote the GUESS image with a consistent emphasis on innovative and distinctive designs. This message is communicated through the use of the company's signature black & white and colour print advertisements, designed by its in-house advertising department located in Los Angeles. This department is responsible for worldwide advertising in order to retain the integrity of the image.

The Company has 680 stores worldwide that are either corporately run or operated by international licensees and distributors. The company also distributes its products through better department stores and select specialty upscale boutiques. In all cases, GUESS works closely with its partners to ensure that its brand image is promoted effectively.

LULULEMON could be considered a similar Canadian example. The Vancouver-based Company was founded in 1998. It focuses on the yoga niche apparel market. Products are based on functional innovation and style by using technical performance fabrics. Design teams meet in every city where there is a LULULEMON store twice per year. They meet with local yogis, athletes and design savvy individuals in order to assist in developing new products. The Company currently employs approximately 650 people and operates 40 stores across North America and one in Australia.

LULULEMON's products are manufactured in Canada, the US, Israel, China, Taiwan, Indonesia and India. The company recently entered into a joint venture with Descente, a leading global technical fabrics supplier. Descente, beyond providing LULULEMON's supply of leading edge technical fabrics, will become a key partner in establishing 20 LULULEMON stores in Japan by 2010.

In 2005, the founder of the Company sold a 48 percent minority interest to US-based private equity firms Advent International and Highland Capital Partners for $225 million. After having seen sales double for the past four years, LULULEMON is continuing its rapid global expansion, with thirty new stores planned for 2007.

Strategy # 4: Be a low-cost commodity producer

A company can decide to be the low cost manufacturer in a "basics" segment. It must be noted that it is not because Canada is a high labour cost environment that this strategy is not an option for Canadian companies. A Canadian company can take advantage of countries with low labour costs by building and running foreign based manufacturing facilities. This is different from merely outsourcing the manufacturing needs. In this case the Canadian company has a facility working exclusively for it. The company can own it directly, co-own it with a local player or have a local player own it, but control the management and get management fees in addition to insuring for itself a low cost high quality production source.

The key skills required consist of knowing how to build and operate efficient manufacturing facilities overseas. This is a strategy pursued by Montreal based GILDAN ACTIVEWEAR that has become a leader in the commodity price sensitive segment of T-shirts.

GILDAN manufactures and sells blank T-shirts which are sold to major print screen printers who then add designs and logos for resale to companies or event organizers for advertising purposes. With over 15,000 employees, the Company has become the North American leader in its market by becoming the lowest cost producer. This has been accomplished through vertical integration of yarn spinning, knitting, dyeing, finishing, cutting and sewing operations located in cost efficient environments, such as Honduras. The Company continues to invest significant capital in new facilities with the latest state-of-the-art manufacturing equipment and technology. In 2006, GILDAN recorded sales in excess of $770 million and net earnings of nearly $107 million.

Strategy #5: Be a product innovator

A company can decide to concentrate its know-how into driving innovation and manufacturing a complex product, thereby isolating itself from the threat of imports from low wage countries. This is the strategy pursued by Vancouver's ARC'TERYX, a company driven by outdoor enthusiasts that produces high-end outdoor gear such as mountain climbing jackets, backpacks, gloves and other clothing.

Driven by innovation, ARC'TERYX (named after the first dinosaur to fly), was founded in 1991 to build better gear. The company focuses not on incremental advancements, but on radically improving the status quo. With over 40 product innovations in its 16-year history, new construction technology, paradigm shifting designs and major fabric technology developments are all part of the norm. All this is achieved by its team of outdoor enthusiasts who understand the market and are constantly finding better ways to meet its customers' needs.

Recognized as a leader in its field, ARC'TERYX was acquired in 2001 by Adidas—Salomon. As an acknowledgement of their tremendous skills, the management team was retained and the Company has continued to operate with minimal intervention from the new parent company. Today, the Company is widely recognized as the leading North American specialist in outdoor apparel, climbing equipment and high-end protective shells. Its highly complex products continue to be manufactured at its Vancouver facility.

Strategy # 6: Become an importer distributing to fragmented retail channels

A company can decide to turn itself into an excellent importer of apparel. Its strengths would be for instance in its sales and distribution capabilities towards a fragmented retail base. It will allow multiple foreign brands with no sales and distribution capabilities to enter the Canadian and US markets. This is the strategy pursued by TYFOON INTERNATIONAL.

While still a private label manufacturer with experience in both knits and wovens including denims, TYFOON's strength lies in its ability to source innovative product for distribution in the Canadian market. TYFOON imports apparel and accessories from leading fashion collections and distributes across the country to Canada's major retailers.

Strategy # 7: Be the preferred, rapid replenishment supplier to majors

A company can capitalize on its proximity to its market and distribution speed in order to compete. Its strengths would lie in customer service excellence, state of the art warehousing, inhouse sales, and forecasting capabilities. It could thus provide rapid replenishment to mass merchandisers. This is the strategy pursued by DORIS HOSIERY MILLS LTD.

DORIS HOSIERY is the largest Canadian supplier of branded and private label leg wear. The company's strength lies in its ability to operate rapid replenishment programs for its major customers. Its on time delivery rates exceed 97 percent. This is accomplished through its fully computerized and automated distribution system, extensive EDI systems and strong in-house forecasting capabilities.

Strategy # 8: Provide several innovative collections per season by shortening the design-to-sale cycle

A company may decide to excel in the management of the entire design-to-sale cycle by being able to offer its clients short cycle times. This is in essence the strategy pursued by ZARA that has been able to reduce design-to-delivery from 10 to 15 days, while not owning a manufacturing base of its own.

The key success factor here has been the investment into automating the entire cycle from design-to-manufacturing-to point of sales systems. Consumer trend information is constantly transmitted from its 500 stores in 30 countries to a design team of approximately 200 professionals located at its head office in Spain. Design teams generate over 11,000 designs per year. Fabrics are sourced globally and executed at mills owned by its parent company. Design and cutting is performed in-house, however sewing is conducted at workshops and cooperatives near its head office. ZARA has supplied technology to all its supply chain partners so that garment production can be traced and monitored through to completion. The Company's sophisticated warehouse includes customized sorting machines patterned on the equipment used by overnight parcel services. Trucks deliver goods to stores within 24 hours driving time, while all others are supplied by air. By mastering the design-to-sale cycle, ZARA has succeeded to attract a large customer base who know exactly when new deliveries will arrive in their local shop and arrive on delivery days to purchase the latest fashions.

A Canadian company that is seeking to follow this model is LE CHÂTEAU. It is a leading Canadian specialty retailer offering contemporary fashion apparel, accessories and footwear to style conscious women and men. The brand's success is built on quick identification of and response to fashion trends through their design, product development and vertically integrated operations.

LE CHÂTEAU brand name merchandise is sold exclusively through its 195 stores. All stores are in Canada, except for five locations in the New York City area.

The Company uses a blend of domestic and offshore sourcing capabilities in order to maintain its fast fashion model, with approximately 42 percent of the Company's goods being manufactured in Canada.

Other strategies specific to contractors

According to the 2003 AHRC LMU, approximately 25 percent of the Canadian apparel workforce is employed by cut and sew contractors. This sector of the industry is undoubtedly being hit hard by globalization. Based on the 2007 AHRC Study, successful contractors tend to be reshaping their businesses by focusing on:

- Specific types of products with the following characteristics:

- Moderate to high fashion;

- Limited labour inputs, either through increasing automation or by avoiding high labour styles.

- Increasing value added service offerings such as offshore sourcing, pattern making, cutting, increased customization, finishing, direct shipping to retailers, etc., in essence becoming manufacturers;

- Clients with rapid replenishment requirements:

- Supplying manufacturers or retailers that supplement import programs with local production for speed to market and short order run requirements;

- Often applicable in fashion sectors.

- Clients with customization requirements:

- Most often applicable in sectors such as promotional wear or uniforms;

- May make use of new technologies (such as sublimation) to differentiate and personalize.

For example, consider the case of CONFECTION CLICHE:

Founded in 1979, the company originally focused on women's clothing. By the late 1980s it specialized in the production of high volumes of T-shirts. By 2000, it quickly refocused to target new customers and niches.

The niches and new customers being targeted by CLICHE include those requiring other value added services, such as customized production, graphic designing, rapid replenishment services, direct shipments to retailers and exporting directly to the US on behalf of its manufacturer customers. The Company continues to grow and is in the process of diversifying and expanding its client base in Canada and the US.

5.5 Future strategies to be deployed across the value chain

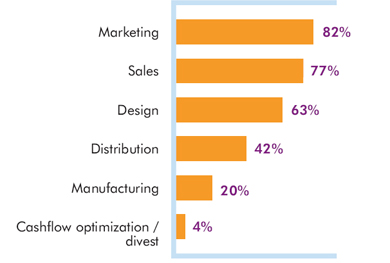

Based on our 2007 AHRC Study, we believe that participating companies will reposition themselves by focusing on the various value chain elements as outlined in Section 5.3 as follows:

Figure 5.1: Future focus areas in the value chain (percent of participants)

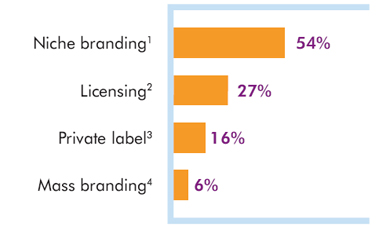

Most common marketing strategies to include:

Figure 5.2: Future focus of marketing efforts (percent of participants)

- Creating a brand for a narrowly defined target market

- Obtaining the manufacturing and or distribution rights for a specific territory for a highly recognized brand name developed by a third party

- Manufacturing products for a specific retailer under a brand name that is controlled and fully marketed by that retailer

- Creating a brand that has mass appeal, aimed at a very large target market

Most common sales strategies to include:

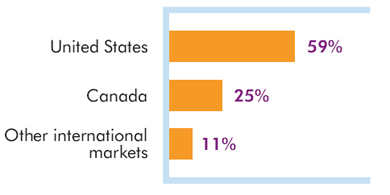

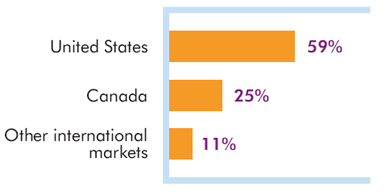

Figure 5.3: Future focus of sales efforts, by region (percent of participants)

Most common direct to consumer sales strategies to include:

Figure 5.4: Future focus of sales efforts, direct to consumer models (percent Of participants)

- Examples include selling directly to sports teams, leagues, home shopping alternatives

Other common sales strategies to include:

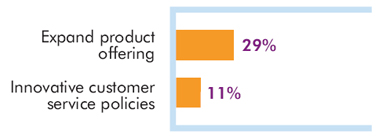

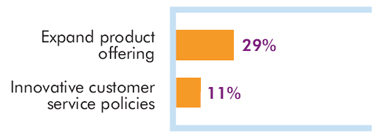

Figure 5.5: Future focus of sales efforts, other (percent of participants)

Future design strategies will include:

Figure 5.6: Future focus of design efforts (percent of participants)

- Performing world-class market research into what the target market wants and rapidly developing relevant designs

- Having a founder / shareholder / key employee who is a design "genius", developing innovative, trend setting designs that lead the market segment or the niche

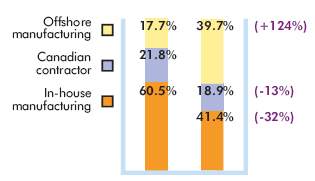

Future distribution strategies will include:

Figure 5.7: Future focus of distribution efforts (percent of participants)

6. Key challenges in adapting to new models

While companies are managing to adapt to offshore sourcing, they are slow to become world class in other parts of the value chain. Challenges are both company specific and general to the industry.

6.1 Company specific challenges

The basics

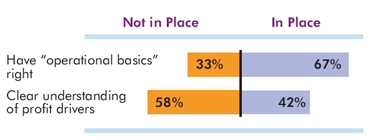

The 2007 AHRC Study indicated that most participants had "operating basics" right, including being able to produce a value for money product that meets the end consumer needs at the right quality level, delivered on-time, with the proper service that retailers demand.

However, the same study noted several weaknesses:

- A startling 58 percent of companies did not have the financial acumen, information or general expertise to identify the true profit drivers in their company. Without this information, these companies have been unable to distinguish profitable versus unprofitable segments of their business, and thus often unable to identify the most profitable niches to grow;

- 58 percent of companies did not have a strong management team, implying that their own internal management competencies may be preventing them from reinventing themselves;

- While 67 percent of apparel companies operate within a niche, 62 percent do not offer the customer anything that differentiates them from the competition.

Contractors were specifically noted to have even greater internal challenges, including:

- Extremely weak sales and marketing capabilities:

- Many companies tend to be dependent on relatively few long term customers;

- These companies do not have an owner or key employees with significant sales capabilities;

- Weak financial and costing which impede their abilities to determine profitable contracts from unprofitable ones;

- Poor workforce cross-training capabilities / flexibility.

A World-Class focus of excellence

Key challenges per company will also vary based on the model being pursued. In general, the following table illustrates the key challenges depending on whether a company intends to maintain an element of the value chain in-house and make it a core focus or whether it intends to outsource it:

Table 6.1: Key challenges by value chain focus

Value chain focus: design

Retained in-house

- Gaining in-depth retailer and end consumer market knowledge

- Using current sales data in order to identify items/styles/product attributes that are selling or not

- Attending leading fashion events for inspiration

- Subscribing to leading trend services

- Partnering with leading global raw material providers to develop new innovative inputs

- Working with customer focus groups/ user groups to identify opportunities for improvement/innovation

Outsourced

- Identifying leading designers/innovators in specific niches and enter into alliance to manufacture/ distribute /sell/ market products in a specific market

Value chain focus: manufacturing

Retained in-house

- Producing niche products

- Customizing production

- Producing short order runs

- Specializing in new technologies and innovation

- Developing a cross trained, flexible workforce and equipment

- Automating to reduce labour component

Outsourced

- Improving offshore sourcing capabilities, including finding offshore sourcing agents and factories, understanding cultural differences, learning foreign business practices,

- Transferring manufacturing capabilities/know-how offshore

- Entering into joint ventures, strategic alliances, partnerships

- Establishing company-owned offshore production facilities

Value chain focus: marketing

Retained in-house

- Developing a brand in a niche

- Securing qualified personnel

- Funding for advertising, promotion

Outsourced

- Identifying and securing licensing rights to sector specific products

- Identifying proper marketing agencies

- Securing appropriate budgets to promote niche brands in North America and beyond

Value chain focus: sales / service

Retained In-House

- Researching new markets; potential retailers; potential end consumers; competitive products

- Dispensing sales reps across a multitude of territories

- Possibly developing company owned retail operation or direct to consumer sales force

Outsourced

- Identifying, securing and motivating third sales agents to sell company products

- Integrating processes with key retailers

- Developing sophisticated forecasting capabilities

Value chain focus: distribution

Retained in-house

- Having adequate information tracking systems

- Having adequate inventory management systems

- Properly training personnel

- Having appropriate facilities and infrastructure

Outsourced

- Identifying 3rd party logistics and distribution facilities near customers that are able to meet company needs

- Identifying skilled, specialized freight forwarders, customs brokers, expertise in international trade law, brokerage and transport

6.2 Industry Specific Challenges

Beyond specific business model challenges as noted above, certain general challenges will impact industry players as well:

Decreasing Domestic Supply Chain

- As manufacturing continues to move offshore, domestic apparel manufacturer suppliers (textile companies, label producers, thread companies, etc.) will face greater challenges;

- In all likelihood, these suppliers will continue to face consolidation and closures;

- As the supply chain erodes, it will become increasingly difficult for those apparel companies wishing to manufacture domestically to do so.

Management Competencies

The 2003 AHRC LMU noted that while most industry executives were aware of the coming industry restructuring, 87 percent did not have a strategic plan to deal with the issues. The 2007 AHRC Study confirmed this still to be the cases at the onset of the program, some three years later.

While the 2007 AHRC Study provided assistance to 130 apparel companies, presumably there continues to be many apparel companies without well-rounded management teams. Beyond specific value chain shortcomings, key weaknesses tend to be in the areas of strategic and financial management.

Succession Issues

Of all participants in the 2007 AHRC Study, 27 percent will face a succession issue within the next 5 years; 42 percent within the next 10 years:

- Most of these companies do not have succession plans;

- There is a strong correlation between companies that have succession plans and strategic plans; i.e., if a company does not have a winning strategy in place, it likely does not have a succession plan;

- Without succession plans, many of these companies will face business continuity issues in the short to mid-term.

Financial Resources

The issue of access to capital for the apparel industry is not new. For years, apparel companies have indicated that they feel there is a lack of support for their industry from the banking community. While there may be some truth to this, it may be for good reason. As previously noted, consider that of the 2007 AHRC Study participants:

- 56 percent did not have a strong management team in place;

- 58 percent were not able to determine the true profit drivers of their business;

- 87 percent did not have a strategic plan that could be acted upon;

- 61 percent were not willing to reinvest in their businesses.

Under these circumstances, it is not a surprise that many companies could not / cannot secure financing. Nevertheless as a result of banking formula-based lending practices, we believe that financing remains a challenge to many well-run apparel companies and small businesses in general.

SMEs at times, also have difficulty securing financing from other lenders. For example, asset based lenders often require substantial premium interest rates. Other larger non-traditional lending institutions and professionals that can assist prefer working with larger companies where greater fees and returns can be earned.

The traditional financing problems will likely become further exacerbated as companies implement new models that do not generate assets that can be collateralized. Consider:

- Soft cost expenditures are often required to implement new models (i.e. designers, marketers, sales and service personnel, increased travel, training and marketing costs, etc.);

- These expenditures offer no collateral security to lending institutions and as a result, are difficult to finance;

- Inventory financing costs are increasing, often as a result of shifts to imports;

- Requirements to fund export receivables are increasing.

To further exacerbate the issues, many executives appear to often strip equity from their companies as opposed to maintaining this capital for future reinvestment.

Human Resources / Skill Requirements

Employment will shift from predominantly production jobs to balanced or predominantly white collar positions. New models will require companies to hire world-class talents in areas such as design, marketing and logistics.

According to the 2007 AHRC Study, positions to be most in demand include:

- Sales professionals (sales managers, brand managers, sales representatives);

- Marketing professionals (marketing managers, marketing analysts, merchandising technicians);

- Designers (product developers and design technicians);

- Import / export specialists;

- Senior management.

This talent appears to be in short supply and in demand by other industries as well. Apparel companies will be challenged to recruit, train and retain these key personnel. Financing such salaries will also be a challenge to companies.

Corporate Structure

According to the 2003 AHRC LMU, 87 percent of Canadian apparel companies had less than 50 employees. Less than 7 percent of companies employed more than 100 personnel. This SME industry structure partly explains the lack of management sophistication in the industry. In order to reinvent themselves, many companies will need to increase their size in order to support greater white collar needs. We believe that this will lead to:

- Further industry consolidation;

- Continued merger and acquisition activity (for companies that have established a niche but need greater volume to expand and operate on a larger scale);

- Partnering / allying / creating joint ventures with world class specialists in order to remain competitive. Such partnerships are likely across the entire value chain in the areas of design, marketing, manufacturing, sales, logistics and distribution.

As in the banking sector, much of the professional expertise in this area (business brokers for example) may be out of reach to many SMEs. Professionals in these areas prefer to work with large organizations whereby they can generate substantial fees as opposed to the SME marketplace.

Industry Regeneration

There are relatively few barriers to entry in launching an apparel company. As a result, the industry is constantly regenerating. Consider that nearly one third of all participating companies in the 2007 AHRC Study were established within the last ten years.

Many of these companies are being founded by new designers graduating from colleges or individuals who have identified an underserved niche. Unhindered with the baggage of yesteryear, many of these companies have viable new business models. In these cases, the challenge is often to secure adequate industry specific managerial talent and financial resources to grow the company.

7. Conclusions

The Canadian apparel industry continues to undergo a period of major restructuring. As the industry as a whole continues to contract, there are many signs of hope. Niches abound and are constantly being developed in the North American and global markets. A host of new business models are being successfully deployed. Companies continue to ramp up their white collar talent in order to compete. Long established organizations have demonstrated an ability to execute turnarounds. Young new entrants have proven an ability to rapidly gain market share. In short, companies with decent foundations have opportunities to survive and grow in these market conditions.

We thank Industry Canada for selecting us to work on this very important mandate. We trust that this initiative will be a critical element in the plan to ensure the future viability of the Canadian apparel industry and its substantial contribution to Canadian employment and the Canadian economy.

Appendix A: About the 2007 apparel human resources council study 23

A.1 Background

In 2003, the Apparel Human Resources Council's The Canadian Apparel Industry: The Shape of the Future—Labour Market Update Study (2003 AHRC LMU) concluded that:

- Approximately 40,000 apparel jobs would be lost by 2005 (40 percent of the workforce) as a result of quota removal and retail restructuring;

- Apparel companies were ill prepared to deal with the coming changes;

- Most industry executives recognized that the industry would undergo major restructuring in 2005, yet 83 percent did not have a strategic plan to deal with the issues;

- Canadian companies had opportunities to survive and grow post-2005, especially by targeting the US market;

- Despite the negative trends, a 1 percent increase in US market share could offset losses;

- Ample niche opportunities exist, especially when targeting the US market.

In response to the study, the Apparel Human Resources Council launched the Apparel Strategic Planning Program. This program was fully funded by the Council. It mandated Milstein & Co Consulting Inc to provide companies with one-on-one strategic planning assistance to help them develop their unique strategic plans.

The exercise included:

- Assessing the impact of trade liberalization on the company;

- Surveying management, key employees and key customers;

- Assessing strengths, weaknesses, opportunities, threats and HR needs;

- Assessing financial viability and ability to execute potential strategies;

- Developing a strategic plan to help the company deal with industry restructuring;

- Customized implementation assistance for companies that already had a plan.

The program was initially established to assist 75 companies, however given the demand it was eventually increased to allow for 130 participants.

A benchmarking report was prepared as a by-product of these nation-wide strategic planning exercises. The purpose of this report was to:

- Provide a "snapshot" of the industry;

- Identify performance trends of successful companies versus the rest of the industry;

- Highlight the strategies for success and the various winning models;

- Provide a "self-help" tool for companies that did not participate in the program to assist in:

- Assessing themselves against benchmarks;

- Determining or reviewing their own strategic direction.

A.2 Program timing

The one-on-one strategic planning exercises commenced in March 2005. Most projects were completed in an elapsed time of three to four months. All one-on-one strategic planning exercises were completed by early 2007. The benchmarking report was completed by March 2007.

A.3 Program promotion

The program was initially promoted across Canada through email blitzes directly to apparel companies, articles, advertisements in Canadian Apparel Magazine and through direct telephone calling. All provincial associations also assisted in promoting the program. Informational presentations were then made to influential professionals, including the major banks and accounting firms.

Interested companies were then invited to participate in presentations entitled "Forum on the Future of the Industry". These sessions were held in February 2005 in Vancouver, Winnipeg, Toronto, Montreal (English and French) and Victoriaville, Quebec (French). At these sessions, industry executives were presented with a situational overview and details of the program were explained. Registration forms were distributed at the sessions and many companies registered immediately.

Further program details were then posted on a Website. Within the first week of the sessions, all of the original 75 slots had been allocated to qualified registrants and a waiting list was started. As previously mentioned, given the demand for the program, by 2006 the program was extended to allow for 130 participants.

A.4 Participant selection methodology

In order to be eligible for the program, applicants had to meet the following conditions:

1. Not be in a turnaround situation

The program was not designed for companies in extreme financial difficulty. Instead, these companies were advised to seek immediate professional assistance in order to address their unique and immediate concerns.

2. Have some element of Canadian manufacturing

The company had to conduct at least some manufacturing in Canada, either through its own plant or through the use of Canadian contractors.

3. Have a minimum number of employees

The company had to employ either directly or indirectly through contractors, a minimum of 15 people in Canada.

Beyond meeting the above conditions, every effort was also made to match the profile of participants to that of the industry. Factors considered included:

- Nature of production activity (manufacturer or contractor);

- Number of employees;

- Geographic location.

A.5 Participants