1. Canadian Retail Market Overview

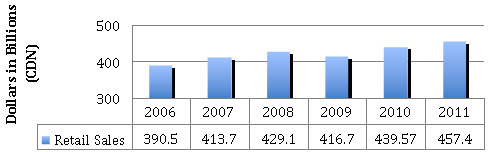

Since the 2005 Consumer Trends Report, the retail sectorFootnote 1 has continued to play an increasingly vital role in the Canadian marketplace, given its contribution to the Canadian economy and its impact on consumers and their consumption activities. In 2011, the sector generated $457.4 billion in retail sales and represented approximately 12 percent of the Canadian workforce (Statistics Canada, 2012c). Despite experiencing falling demand during the recession in 2009, the sector's sales grew by 17.1 percent between 2006 and 2011 ($457.4 billion in sales in 2011, an increase of $66.9 billion compared to 2006). Even at its lowest ebb in 2009 ($416.6 billion in sales), the sector represented 6.2 percent of Canada's gross domestic product, an increase of 0.2 percent compared to 2001 (Industry Canada, 2010; Statistics Canada, 2012c). The gains in sales since the recession have been relatively healthy, rising to $457.4 billion for all of 2011, reflecting an increase of 4.0 percent from the previous year (Statistics Canada, 2012c). Sales in the retail sector were dominated by the motor vehicle and parts dealer sub-sector, which totalled $100 billion in sales in 2011, or 21.9 percent of market share, and the food and beverage stores sub-sector, which totalled $104.1 billion, or 22.8 percent of market share. For a list of total sales by the retail sub-sectors in Canadian, please see Table 1.

The sector has grown by other measures as well. In April 2011, retail sales in Canada were equivalent to retail sales in the U.S. on a per capita basis for the first time (Ladurantaye, 2011) reaching US$13,000 per person (Cooper, 2011). As recently as 2004, sales per capita in Canada had only been US$8,000 versus US$12,000 in the U.S. (Colliers International [CI], 2011a). This reveals that while sales growth in the U.S. has slowed, growth in Canada has continued to accelerate. It's important to note the shift in sales per capita between Canada and the United States may not be fully attributable to strong productivity gains or increasing consumer debt burden in Canada, but instead, due to poor performance by the American retail sector heavily influenced by the 2008–09 economic recession.

| Sub-Sectors of the Retail Market Place in Canada | Retail Sales in 2011 (dollars × 1,000) | Percent of Market Share |

|---|---|---|

| Source: Statistics Canada CANSIM data, Table 080-0022 | ||

| Motor Vehicle and Parts Dealers | $100,005,680 | 21.9 |

| Furniture and Home Furnishing Stores | $15,027,138 | 3.3 |

| Electronics and Appliance Stores | $14,983,443 | 3.3 |

| Building Material and Garden Equipment and Supplies Dealers | $27,038,063 | 5.9 |

| Food and Beverage Stores | $104,134,083 | 22.8 |

| Health and Personal Care Stores | $32,847,751 | 7.2 |

| Gasoline Stations | $57,682,168 | 12.6 |

| Clothing and Clothing Accessories Stores | $26,049,959 | 5.7 |

| Sporting Goods, Hobby, Book and Music Stores | $11,153,804 | 2.4 |

| General Merchandise Stores | $57,785,413 | 12.6 |

| Miscellaneous Store Retailers | $10,695,657 | 2.3 |

Impact of the Global Recession on Consumer Confidence in Canada

The 2008–09 global recession had a mixed impact on consumer sentiment in Canada. Although the Canadian retail sector has recovered from the global economic downturn, a segment of the Canadian population still felt wary and conflicted over the economic environment. In late 2010, 14 percent of the Canadian population believed the economy would weaken in 2011. This figure increased significantly in late 2011, as 33 percent of Canadians thought the economy would weaken in 2012 (Deloitte, 2011).

This is consistent with similar measures of consumer sentiment, such as the Conference Board of Canada's Consumer Confidence Index (CCI). With Canada's CCI reaching a high of 89.0 following the 2010 holiday season (January 2011), the CCI started to fall in March of 2011 and hit a low of 69.9 in December of 2011—the lowest level since 2009 when the Canadian economy started to recover from the 2008–09 recession (Canadian Press, 2011; Deloitte, 2011; Conference Board of Canada, December 2011). As of December 2012, Canada's CCI had recovered slightly from the dip experienced in late 2011 and sat at 77.9 (Conference Board of Canada, 2012).

It's important to note that Canadians, in general, have remained more positive about the Canadian economic climate when compared to American consumers respecting their marketplace. In the same time frame, the American CCI dropped from 62 (in December 2010) to 45 (in September 2011) (Deloitte, 2011). As of December 2012, the United States' CCI stands at 65.1, a slight improvement from the lackluster levels experienced 12 months earlier (Conference Board, 2012).

Footnotes

- Footnote 1

-

For the purpose of this report, the retail sector is defined as: motor vehicle and parts dealers, furniture and home furnishings stores, electronics and appliance stores, building material and garden equipment and supplies dealers, food and beverage stores, health and personal care stores, gasoline stations, clothing and clothing accessories stores, sporting goods, hobby, book and music stores, general merchandise stores, and miscellaneous store retailers.