Notice

The public consultation on the Bankruptcy and Insolvency Act and the Companies' Creditors Arrangement Act closed on July 15, 2014.

This publication is available online in html at https://www.ic.gc.ca/eic/site/cilp-pdci.nsf/eng/h_cl00021.html.

This publication is also available in accessible formats (Braille, large print, etc.) upon request. Contact the Industry Canada Web Services Centre:

Telephone (toll-free in Canada): 1-800-328-6198

Telephone (Ottawa): 613-954-5031

Fax: 613-954-2340

TTY (for hearing impaired): 1-866-694-8389

Business hours: 8:30 a.m. to 5:00 p.m. (Eastern Time)

Email: ic.info-info.ic@canada.ca

Permission to Reproduce

Except as otherwise specifically noted, the information in this publication may be reproduced, in part or in whole and by any means, without charge or further permission from Industry Canada, provided that due diligence is exercised in ensuring the accuracy of the information reproduced; that Industry Canada is identified as the source institution; and that the reproduction is not represented as an official version of the information reproduced, nor as having been made in affiliation with, or with the endorsement of, Industry Canada.

For permission to reproduce the information in this publication for commercial redistribution, also contact the Industry Canada Web Services Centre mentioned above.

Cat. No. Iu173-5/2014E-PDF

ISBN 978-1-100-23479-3

© Her Majesty the Queen in Right of Canada, represented by the Minister of Industry, 2014.

Aussi offert en français sous le titre Direction de l'entreprise, de la concurrence et de l'insolvabilité.

PDF version

Table of contents

- Executive Summary

- Introduction

- Consumer Issues

- Commercial Issues

- Encouraging Innovation through Intellectual Property Rights

- Encouraging Restructuring

- Streamlining Companies' Creditors Arrangement Act Proceedings

- Balancing Competing Interests

- Professional Fees in CCAA Proceedings

- Enhancing Transparency

- Role of the Monitor

- Asset Sales

- CBCA Arrangements

- A Streamlined Small Business Proposal Proceeding

- Division I Proposals Extension

- Liquidating CCAA Proceedings

- Enhancing Equity

- Deterring Fraud and Abuse

- Cross-Border Insolvencies

- Administrative Issues

- Technical Issues

Executive Summary

Pursuant to a statutorily-mandated review of the Bankruptcy and Insolvency Act and the Companies' Creditors Arrangement Act, Industry Canada is conducting public consultations to obtain submissions from interested Canadians regarding Canada's insolvency legislation. The discussion paper, which sets out numerous issues identified from key stakeholder input and an environmental scan of the insolvency marketplace, is intended to provide a framework for the public consultations.

The discussion paper is divided into four sections: first, an introduction; second, consumer insolvency issues; third, commercial insolvency issues; and, finally, administrative and technical issues.

The introduction provides general information regarding Canada's insolvency regime and the policy objectives that underlie it, as well as recent marketplace changes and insolvency trends.

The sections on consumer and commercial issues set out broad themes under which specific issues may be found. For example, the consumer insolvency themes include protection of consumer interests, the "fresh start" principle, consumer exemptions, protecting families, and treatment of student loans in bankruptcy. The commercial insolvency themes include encouraging restructuring, protecting vulnerable creditors and enhancing equity, deterring fraud and abuse, and cross-border insolvencies.

The section on administrative and technical issues sets out a number of discrete matters, including renaming the Bankruptcy and Insolvency Act, creating a unified insolvency Act, and marshalling of charges.

Pursuant to the statutory review provisions contained in both Acts, the Minister of Industry is to table a report in Parliament on the "provisions and operations" of the Act by September 2014. The report would then be referred to a Parliamentary committee for study and report within 12 months of the initial tabling. Any decisions regarding possible legislative or regulatory reforms as part of the statutory review would be taken following consideration of the Parliamentary committee's study and report.

Introduction

The Importance of Insolvency Law

Insolvency laws have a significant impact on the economy. Insolvency rules offer security for investors and lenders in both consumer and commercial borrowing transactions. This, in turn, influences credit market risks, which can affect the cost and availability of credit. In the commercial sphere, the reliability of the insolvency system plays a role in attracting domestic and foreign investment, as well as in promoting entrepreneurship and innovation.

One of the principal considerations in an era of increased globalization and competitiveness is how to make the insolvency process as efficient as possible, while maintaining fairness. By facilitating corporate restructuring and directing assets to productive use, the insolvency system contributes to Canada's economic competitiveness and performance.

Rules governing personal insolvency play an important socio-economic role. They allow honest but unfortunate individuals who experience difficult financial distress to release their debts and obtain a fresh start. The consumer insolvency provisions are aimed at balancing the interests of debtors with the interest of creditors who extended credit in the expectation of repayment.

As such, insolvency laws contribute in a meaningful way to the effective and efficient functioning of the marketplace.

Canada's Insolvency Regime

Legislative Framework

The insolvency regime makes up part of Canada's fundamental marketplace framework laws and relies on two main statutes: the Bankruptcy and Insolvency Act (BIA) and the Companies' Creditors Arrangement Act (CCAA).

The BIA provides a legislative framework to address both consumer and commercial insolvency situations. In bankruptcy, the Act provides for the liquidation of the bankrupt's assets by a trustee and the distribution of the proceeds in a fair and orderly way among the creditors. Alternatively, the Act provides a mechanism for insolvent consumers or commercial debtors to avoid bankruptcy by negotiating settlements with their creditors to reorganize the debtor's financial affairs.

The CCAA provides a legislative framework for the reorganization of insolvent commercial debtors under the court's supervision. It enables an insolvent business to seek a court order staying its creditors from taking action against it while it negotiates an arrangement with them for the rescheduling or compromise of its debts. The CCAA provides a more flexible, court-driven process than the BIA. Businesses reorganizing under the Act must have more than $5 million in debt.

Administrative Framework

Canada's insolvency regime's administrative framework is supported by three pillars:

- Office of the Superintendent of Bankruptcy (OSB): regulator with oversight responsibilities for the insolvency system;

- Trustees-in-Bankruptcy: licensed by the Superintendent, they are responsible for administering estates and performing various roles under the BIA and CCAA; and

- Courts (including registrars in bankruptcy): supervise CCAA proceedings and adjudicate matters under both the BIA and CCAA.

The OSB has statutory responsibility to supervise the administration of all estates and matters under the BIA. Additionally, the OSB has certain functions under the CCAA, including maintaining a public record of CCAA proceedings and investigating complaints regarding the conduct of monitors. In fulfilling its mandate, the OSB sets standards and provides guidance to stakeholders regarding expected conduct through Directives, notices, position papers and programs.

Trustees-in-bankruptcy are responsible for administering insolvencies and can often be engaged to provide advice to financially distressed individuals and businesses. They work with the debtor to complete necessary steps in a bankruptcy, proposal to creditors or restructuring. This involves filing documents with the OSB and ensuring the debtor fulfills the requirements under the BIA or CCAA. Where the debtor fails to fulfill the requirements, as an officer of the court, the trustee is to bring the issues to the attention of the creditors and the court.

The role of the courts varies depending upon the nature of the proceeding. Most individuals who file for bankruptcy will not be required to go to court. Instead, they will obtain a discharge from bankruptcy after the specified period of time through an automatic process. If a trustee or creditor opts to oppose a bankrupt's discharge, the matter is brought to the courts. In other proceedings, the courts are involved at various stages. For example, the courts may be required to resolve disputes or sanction specific actions proposed by the debtor or creditors. In CCAA proceedings, the court plays a key role. Court approval is required to commence a proceeding and it may make various other orders, including approving interim financing, the process for sale of assets, and the disclaimer of contracts. Courts are also responsible for sanctioning any plan of arrangement or compromise.

Objectives of Insolvency Law

Insolvency laws aim to minimize the impact of a debtor's insolvency on all stakeholders. They do this by pursuing the key objectives of equitable distribution of the debtor's assets, and, where possible, by rehabilitation of the debtor.Footnote 1 As noted by the Supreme Court of Canada:

The very design of insolvency legislation raises difficult policy issues for Parliament. Legislation that establishes an orderly liquidation process for situations in which reorganization is not possible, that averts races to execution and that gives debtors a chance for a new start is generally viewed as a wise policy choice. Such legislation has become part of the legal and economic landscape in modern societies. But it entails a price, and those who might have to pay that price sometimes strive mightily to avoid it. Despite the proven wisdom of the policies underpinning the insolvency legislation, it is understandable that few appreciate the "haircuts" or even outright losses that bankruptcies trigger.Footnote 2

It is generally accepted that the objectives of insolvency law may be achieved through legislation that does the following:

- provides certainty in the market to promote economic stability and growth;

- maximizes value of assets;

- strikes a balance between liquidation and reorganization;

- ensures equitable treatment of similarly situated creditors;

- provides for timely, efficient and impartial resolution of insolvency;

- preserves the insolvency estate to allow equitable distribution to creditors;

- ensures a transparent and predictable insolvency law that contains incentives for gathering and dispensing information; and

- recognizes existing creditor rights and establishes clear rules for ranking of priority claims.Footnote 3

It is in this context that Canada's insolvency laws have been developed by Parliament and have evolved through court decisions.

Marketplace Changes

Since the last public consultations on insolvency laws conducted in 2001-2002, which resulted in the legislative reforms of 2008 and 2009, the characteristics of the Canadian consumer marketplace have changed. The ratio of consumer debt to personal disposable income in Canadian households has increased from approximately 110 percent in 2000 to 160 percent in 2012.Footnote 4 The increase can be attributed to higher mortgage debt levels and an increase in home equity extraction, both associated with elevated housing prices.Footnote 5 Higher mortgage debt levels are a potential source of risk as Canadians may be more vulnerable to a decline in housing prices or an increase in interest rates.

In the commercial context, marketplace changes include the growing importance of intellectual property to Canadian companies, the use of more complex corporate structures, a shift by lenders away from relationship lending, significant growth in the use of derivatives to hedge risk and in the practice of distressed debt trading, and an increasing number of cross-border insolvency proceedings. At the same time, the cost and complexity of restructuring proceedings, particularly under the CCAA, continues to grow, resulting in a shift towards other types of workout arrangements such as private workouts and arrangements under the Canada Business Corporations Act.

Insolvency Trends

National Insolvency Rates

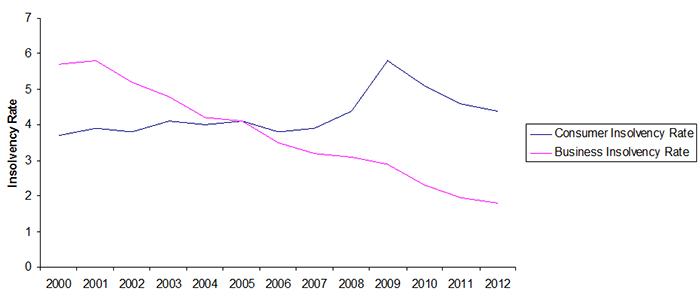

Figure 1 illustrates the national consumer and business insolvency rates between 2000 and 2012.Footnote 6 An overview of insolvency rates provides a clearer picture of trends than does the total volume alone, because it takes into account changes in population sizes over time. As shown in Figure 1, consumer and business insolvency rates have trended in opposite directions during the past decade. The consumer insolvency rate remained relatively steady from 2002 to 2007 before increasing to 5.8 during the economic downturn in 2009 and declining in subsequent years. In 2000 and 2012, the national consumer insolvency rates were 3.7 and 4.4, respectively. This represents an 18 percent increase in the insolvency rate over this period. On the other hand, other than a small increase during the 2001 economic downturn, business insolvency rates have trended downward throughout the decade. In 2000 and 2012, the national business insolvency rates were 5.7 and 1.8 respectively, representing a 68.4 percent decrease.

Figure 1: Consumer and Business Insolvency Rates

Consumer Insolvency Rate — by Age and Regional Breakdowns

Insolvency does not affect all segments of society equally. Variations in the rates of insolvency by age cohort and by geographic region provide important information regarding insolvency trends in Canada.

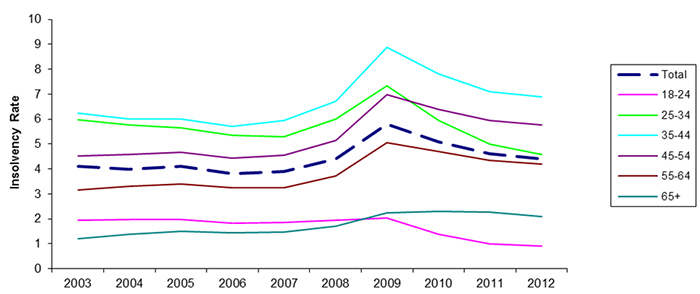

Figure 2 shows the national consumer insolvency rate by age cohort. During the past decade, younger Canadians (those between 18 and 34) became significantly less likely to commence insolvency proceedings. On the other hand, Canadians aged 35 and older become more likely to enter insolvency proceedings. This demographic trend is consistent with anecdotal reports that delayed transitions to adulthood among younger Canadians may be placing a greater financial burden on the parents of adult offspring.Footnote 7

It is also important to note that while the insolvency rate of individuals over the age of 65 has increased over the past decade, it still remains well below the national average.

Figure 2: Insolvency Rates by Age Group

There is also significant regional variation in consumer insolvency rates. Between 2000 and 2012, the consumer insolvency rate has increased in Atlantic Canada, Quebec, and Ontario. There has been a better experience in Western Canada as the insolvency rates in Alberta and British Columbia have remained relatively constant while in Saskatchewan and Manitoba they have decreased slightly. Furthermore, the Atlantic Provinces, Quebec, and Ontario continue to have insolvency rates that are higher than the national rate, while the Western provinces and the Prairie provinces have rates that are lower than the national average.

The higher insolvency rates in Atlantic Canada, Quebec, and Ontario may reflect the underlying economic conditions compared to Western Canada. There is empirical support for the hypothesis that unemployment rates and the growth rates are significant in explaining the variation in insolvency filings.Footnote 8 For example, in recent years economic growth rates in Alberta, Saskatchewan, and Manitoba have been higher than the national average, while growth rates in Ontario, Quebec, and Atlantic Canada have been lower.Footnote 9 Additionally, Western Canada's unemployment rates are lower than the national average, while Atlantic Canada's unemployment rate is higher.Footnote 10

Figure 3: Consumer Insolvency Rates of Insolvency by Region

Growth in Consumer Proposals and Business Proposals

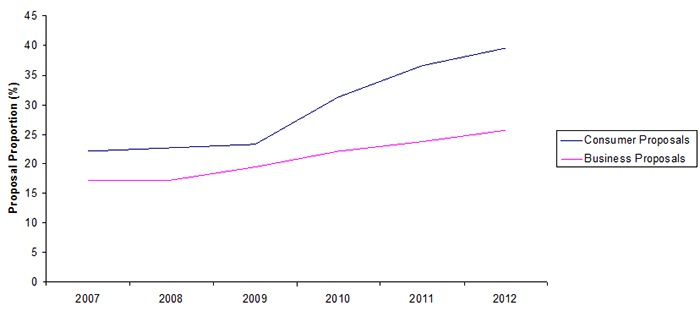

In recognition of the benefits of proposals for insolvent Canadians and their creditors, the 2008-2009 reforms were intended to encourage their use. Figure 4 illustrates the growth in consumer and business proposals under the BIA, as a percentage of total insolvency filings, since 2007. During the same period, the proportion of business proposals as a percentage of total business insolvency filings increased from 17.3% to 25.7%.

Figure 4: Proposal Growth — Consumer and Business Insolvencies

Conclusion

Insolvency laws touch on all aspects of economic life, both for consumers and businesses. They affect the ability of borrowers to access credit, the decisions of investors, and the level of disruption produced by the exit of inefficient firms from the marketplace. They also provide over-indebted consumers with an opportunity to obtain a fresh start and renewed financial health. As a result, it is important to Canada's overall economic performance that its insolvency legislation remains modern, effective and efficient.

In the consumer insolvency context, growing consumer debt levels and changes in demographic insolvency trends – which show that younger Canadians are less likely, and those between the ages of 45 and 54 are more likely, to become insolvent – suggest potential areas for policy focus. Emerging trends in commercial debt markets, including the growth in distressed debt trading and the use of derivatives to hedge economic risk, also suggest areas for policy consideration.

As Canada reviews its insolvency legislation, the overarching objectives of maximizing value, providing a balanced and equitable regime, and ensuring efficient and effective processes will form a base for the policy discussion.

Consumer Issues

Introduction

Individuals who encounter financial distress and are unable to service their debts may resort to insolvency proceedings (i.e., bankruptcies or proposals) under the BIA. The consumer insolvency provisions are aimed at balancing the interests of debtors and their creditors.

In bankruptcy, the debtor's property, subject to certain limitations,Footnote 11 is liquidated by a trustee and the proceeds are distributed to his or her creditors. In return, a bankrupt is released from most types of debts.Footnote 12 Where the bankrupt has the financial means to contribute a portion of his or her income towards the outstanding debts ("surplus income"), the legislation requires them to do so. First-time bankrupts without surplus income are eligible for discharge from bankruptcy after nine months. The period before being eligible for discharge is longer for those bankrupts with surplus income and for those who have previously been bankrupt.Footnote 13

Alternatively, the BIA provides insolvent debtors with the option of making a proposal to their creditors to repay, over a period of up to five years, all or a portion of what is owed. Proposals have the advantage of allowing the debtor to achieve financial rehabilitation while permitting them to retain assets that would otherwise be liquidated in a bankruptcy. For creditors, successful proposals typically offer a greater recovery than would be available in a bankruptcy.

Protection of Consumer Interests

Consumer Deposits

A retailer may receive payment before providing the contracted goods or services to the consumer. Questions of fairness arise if that retailer then becomes insolvent. The rights of buyers of prepaid goods and services are regulated to some extent by provincial consumer protection legislation, but in the absence of an insurance fund or other compensation, the consumer may become an unsecured creditor in the retailer's bankruptcy.

A consumer lien on the assets of insolvent retailers may protect consumers who have provided deposits or pre-payments. The Senate Committee in 2003 considered the merits of adding consumer liens to the BIA but recommended that the issue should continue to be governed by provincial legislation.Footnote 14 In the United States, consumer deposits are treated as preferred claims in bankruptcy for up to approximately US$2,250. The claims rank ahead of unsecured creditors' claims but behind secured claims.

Advocates for consumer liens assert that it is not possible for consumers to determine the financial condition of a retailer before making a deposit and that a consumer lien would provide protection similar to that given to unpaid suppliers. However, a preferred claim may not result in any meaningful recovery for the consumer as the retailer's assets may be subject to an existing secured charge. If the consumer lien ranked ahead of secured creditors, it would be more effective but lenders would likely react by reducing the availability, or increasing the cost, of credit to retailers to take into account the possibility of such liens ranking ahead of their security.

Stakeholders are invited to make submissions regarding whether, and how, Canada could enhance protection for consumer deposits either through consumer liens or, alternatively, through other mechanisms within the insolvency regime.

Responsible Lending

The BIA provides that debtors' conduct can be subject to scrutiny in order to ensure fairness and integrity of the system. However, creditor behaviour may also contribute to financial difficulty for some Canadians. For example, credit granting practices such as extending credit on onerous terms to individuals who are unable to meet their existing financial obligations can lead to higher rates of insolvency. This may impact on existing creditors, whose recovery would likely be reduced due to the increased claims.

In the wake of the 2008 financial crisis, there have been increased calls for legislative intervention in the United States and other countries for "responsible lending" regimes that would impose certain duties on creditors before they extend credit and restrict the insolvency remedies available to those who did not meet these duties. Possible responses could include empowering the trustee or court to disallow the claim of a creditor where credit was extended improvidently or on unconscionable terms. Additionally, the lender could be required to disgorge payments made on such loans in the period leading up to a bankruptcy or proposal, similar to the treatment of preferences.

Stakeholders are invited to make submissions regarding whether, and how, the BIA could take into account creditors' conduct that has contributed to the financial difficulties or insolvency of a debtor.

The "Fresh Start" Principle

One of the key objectives of the BIA is to enable an honest but unfortunate debtor to obtain a discharge from his or her debts, subject to such conditions as the court may see fit to impose. This is referred to as the "fresh start" principle. Limiting the fresh start principle are specified classes of debt that are not released by an order of discharge.Footnote 15 The exceptions are based on overriding public policy concernsFootnote 16 because the nature of the debt outweighs the benefit of the bankrupt being relieved of them.

Licence Denial Regimes

Licence denial regimes are used by certain creditors to continue collection efforts even though the debt was stayed and then released through the insolvency process.Footnote 17 For example, the regimes may permit a creditor to deny a driver's licence or vehicle registration unless full payment is received. The regimes relate almost exclusively to claims arising from the use of motor vehicles.Footnote 18 Creditors that rely on these regimes include insurance companies, provincial insurance regimes, electronic toll-highway operators and rental car companies.

Proponents of these regimes argue that they only encourage voluntary payment since driving is not a right and that debtors may choose to forgo the privilege of driving should they not be able to pay the debt in full. On the other hand, it has been argued that once insolvency proceedings are commenced these special collection tools are replaced with those available through the collective insolvency process. They may no longer be used as they interfere with the insolvency process and frustrate the debtor's ‘fresh start'.

There is greater clarity in the United States as the Bankruptcy Code expressly bars the use of these special collection tools to collect released debts.Footnote 19 In Canada, it has been left up to theFootnote 20 In order to ensure consistent national treatment, Industry Canada is interested in the views of Canadians regarding this issue.

Submissions are invited as to whether amendments are required to the BIA to address the apparent conflict between the "fresh start" principle and the objectives of licence denial regimes.

Reaffirmation Agreements

Reaffirmation agreements between a bankrupt and a creditor are those where the bankrupt agrees to pay a debt that was or will be released by a bankruptcy. Courts have recognized that bankrupts may reaffirm an obligation in one of two ways: 1) by conduct, where the bankrupt continues to make payments to a creditor under an agreement, or 2) by express agreement where the bankrupt enters into a written agreement with the creditor to repay an otherwise released debt.

There is no statistical evidence regarding the extent to which reaffirmation is taking place in Canada or whether the practice is being abused. Some commentators have called for greater regulation of reaffirmation on the grounds that it undermines the "fresh start" principle in insolvency. Reaffirmation by conduct (i.e., continued payments) is of particular concern since bankrupts may reaffirm an agreement without realizing he or she is doing so. On the other hand, there may be compelling reasons why a bankrupt may want to voluntarily continue to pay a debt obligation (a common example is a car lease agreement, where the bankrupt requires the use of a car).

Reaffirmation of debts was raised during the last statutory review. The Personal Insolvency Task Force (PITF) in its 2002 reportFootnote 21 recommended that reaffirmation agreements in respect of unsecured transactions be prohibited because they offend the "fresh start" principle and have the effect of giving one creditor preference over other creditors. However, the PITF recommended that reaffirmation be permitted for secured transactions on the ground that it allows the bankrupt to retain the assets covered by the security agreement and the secured creditor would be in the same position as they would have been if they had to enforce the security. Other stakeholders indicated the need for greater study into the scope and frequency of reaffirmation agreements before making any legislative changes on this issue.

Stakeholders are invited to make submissions regarding whether reaffirmation agreements should be regulated under the BIA, either through the mechanisms discussed above or through other mechanisms within the insolvency regime.

Consumer Exemptions

Registered Savings Products

Successive governments have created initiatives intended to encourage Canadians to create long-term savings for various purposes. For example, Canadians may save for retirement through registered retirement savings plans (RRSPs), for children's post-secondary education expenses through registered education savings plans (RESPs) or for disabled persons' future financial security through registered disability savings plans (RDSPs).

In 2009, RRSPs were exempted from seizure in bankruptcy, subject to a clawback of contributions made in the 12 months before the filing. The goal was to protect retirement savings in a similar way to the protections afforded to registered pension plans, which are exempt from seizure in the event of bankruptcy of the holder of the pension. The exemption of RESPs was also examined in the last review. The Senate Report recommended that the BIA be amended to exempt RESPs from seizure in bankruptcy if: the RESP is locked in; and, RESP contributions in the one-year period prior to bankruptcy are paid to the trustee for distribution to creditors.Footnote 22 Largely because these conditions could not be met, which created a significant potential for abuse, RESPs were not exempted from seizure in an insolvency proceeding.

An RDSP is a long-term savings plan intended to assist Canadians with disabilities and their families to save for the future. Eligible parties may contribute any amount per year up to a lifetime contribution limit of $200,000. Government matching grants and bonds are also available to supplement the RDSP, depending on the amount contributed and the family income of the beneficiary.

RDSPs serve the public interest by encouraging savings for the support of people with disabilities. As a result, it has been suggested that they could be exempted from creditor claims in bankruptcy, similar to the protection provided to RRSP funds. Supporters of an exemption for RDSPs note that there are significant differences between RESPs and RDSPs that reduce the potential for abuse in bankruptcy. Unlike an RESP, only individuals who claim the disability tax credit under the Income Tax Act qualify for an RDSP and there can only be one account for that person. Furthermore, only a parent, legal guardian or trust institution may open and contribute to the RDSP and only the beneficiary can access the funds. It is possible, however, that exempting RDSPs could create the potential for abuse that adversely impacts other creditors' interests.

Stakeholders are invited to make submissions regarding the treatment of registered savings products in bankruptcy.

Federal Exemption Lists

Generally, a bankrupt's property is liquidated by a trustee and the proceeds are distributed among the creditors according to the distribution scheme set out in the BIA. Certain property is, however, exempt from distribution to creditors. The exemptions are set by provincial/territorial law.

Stakeholders have questioned whether it would be more appropriate to have a federal exemption list that would apply to all personal bankruptcies regardless of the bankrupt's province of residence or, alternatively, would permit the bankrupt to choose between the federal and provincial exemption list.

In the last statutory review, the Senate Report and the PITF Report recommended that there be a federal exemption list that the debtor can select in preference to the otherwise applicable provincial or territorial exemptions. The issue of whether to develop a federal exemption list was not addressed in the 2008 and 2009 insolvency reforms.

A federal exemption list could create a minimum standard available to all bankrupts. On the other hand, if it varies significantly from existing provincial/territorial exemption lists, it could create uncertainty for creditors who would not know which list a bankrupt would select.

Submissions are invited as to whether the introduction of a federal list of exemptions should be considered.

Protecting Families

Equalization Claims

Marriage breakdown and insolvency are often closely linked as marriage breakdown can often be a trigger for insolvency proceedings.Footnote 23 The special nature of some family law debts has been recognized in insolvency law. Under the BIA, a specified portion of unpaid child and spousal support is treated as a preferred claim and is paid ahead of the claims of unsecured creditors.Footnote 24 Also, family support obligations are not released by the bankrupt's discharge.Footnote 25

With respect to family assets, most provinces use the "division of property" approach. Divorcing spouses are deemed to have an inchoate claim to half of the family assets which are then divided between the spouses. In the case of exempt assets, bankruptcy has no impact on such divisions as the inchoate claim is not a money claim that would be stayed or released by the bankruptcy.

Ontario, Manitoba and Prince Edward Island use an "equalization" approach under which spouses are entitled to keep property held in their own names but share any increase in the value of marital property that occurred during marriage. Usually this means one spouse must make an equalization payment to the other spouse. Under provincial law, such a payment is considered to be a debt owed by one spouse to the other and is treated as an unsecured claim in an insolvency proceeding.

In SchreyerFootnote 26, the Supreme Court of Canada found that if the paying spouse becomes bankrupt, an equalization payment may be released in the bankruptcy. As a result, the non-bankrupt spouse was not entitled to payment of the equalization claim while the bankrupt spouse was entitled to keep the exempt property, which was the family farm. The Court noted the apparent injustice and suggested there should be better protection for equalization payments in the event of bankruptcy to avoid such inequitable results.Footnote 27

Submissions are invited as to whether, and how, bankruptcy legislation could be amended so as to improve the status of equalization payments in bankruptcy.

Family Support Claims and the Levy

Bankruptcy provides an efficient collection mechanism for creditors as they may rely on the collective remedies available to the trustee to satisfy their claims. In order to offset the costs of the OSB, the regulator responsible for protecting the integrity of the bankruptcy system, a levy is applied to all payments made by a trustee.Footnote 28 The levy is typically five percent of payments.Footnote 29

Subject to certain conditions, family support claims are provable claims under the BIA.Footnote 30 This means that a creditor may file a proof of claim and receive a dividend out of the estate. Family support claimants may receive treatment that is preferential to other creditors, to a specified extent, as a portion of their claims may be paid in priority to the claims of other unsecured creditors.Footnote 31 The claims also survive the bankruptcy process, meaning that they are not released when the bankrupt receives his or her discharge.Footnote 32 The practical impact is that family support claimants can expect to receive greater recovery through the BIA process than other unsecured creditors and they are also entitled to collect the remaining indebtedness post-bankruptcy without competing with creditors whose claims have been released.

As a result of the Cameron decision, in which the court held that "the levy is to be shared by all creditors who benefit from the proceedings,"Footnote 33 family support creditors must give the bankrupt credit for amounts paid in respect of the levy. Some stakeholders have suggested, however, that not all section 178 creditors credit the bankrupt for the amount of the levy, resulting in an inequitable situation where some section 178 creditors obtain full payment and others do not.

Submissions are invited as to the treatment of section 178 creditors with respect to the Superintendent's levy.

Vesting of Family Property Claims

Upon bankruptcy, all property of the bankrupt at that date and any property that may be acquired by or devolve on the bankrupt before his or her discharge, with certain exceptions, vests in the trustee for distribution among the bankrupt's creditors. Property can include the bankrupt's right to sue a former spouse for an equalization claim or for the division of matrimonial property.

In the last statutory review, the Senate Report recommended that the right to sue the bankrupt's spouse for equalization or division of property under provincial/territorial matrimonial property law be excluded from property vesting in the trustee.Footnote 34 The Senate Committee heard that the trustee often settles the claim at a significant discount. As a result, the non-bankrupt spouse retains most of the bankrupt spouse's share of the family assets and the creditors receive very little from the settled claim. Moreover, confidence in the insolvency system may be undermined.Footnote 35

Stakeholders have recommended that the right to sue remain with the former spouse but that any proceeds obtained from the action be considered property to be distributed among the creditors.

Stakeholders are invited to make submissions regarding the treatment of the right to sue a former spouse for an equalization claim or the division of property as property vesting in the trustee.

Joint Debts

Section 142 of the BIA addresses the distribution of property when partners become bankrupt. The section is intended to deal with business situations involving partnerships, not matrimonial situations. Some stakeholders have raised the concern that parties may attempt to apply s.142 in matrimonial situations which could have the effect of distorting the distribution of property that would otherwise take place.

Submissions are invited as to whether s.142 should be amended to restrict its application to business partnerships.

Treatment of Student Loans in Bankruptcy

Discharge of Student Loan Provisions

The federal and provincial governments have implemented student loan programs intended to assist full- and part-time post-secondary students pay for higher education and training. Since these loans are granted on need rather than ability to repay in the event of bankruptcy they are treated differently than other debts under the BIA. In 1997, the BIA was amended to create a two-year waiting period from the time a student ceased to be a full- or part-time student before the loan could be released in bankruptcy. In 1998, the waiting period was increased to 10 years. It has been noted that students typically benefit from the educational opportunities that are facilitated by the government student loans and that the loans are eligible for interest relief, debt forgiveness and other relief under the terms of the student loan program. Accordingly, many stakeholders recognize that the release of student loans in bankruptcy should be subject to special rules, including a waiting period.

The Senate Report recommended a waiting period of five years or, in the case of hardship, a waiting period of less than five years. The Senate heard from stakeholders that the 10-year waiting period created "a period of social atrophy" as the debtor could neither afford to pay the debt, nor to move on from it through the normal means of bankruptcy.Footnote 36 In 2009, the BIA was amended to reduce the waiting period from 10 to seven years or, in the case of significant financial hardship, from 10 to five years. Some stakeholders suggest that the seven- and five-year waiting periods still impose too high of a burden.

Stakeholders are invited to make submissions regarding whether the current provisions regarding the release of student loan debts should be amended.

Hardship Discharge

Under the BIA, release of government-funded student loans can be granted on grounds of hardship if the debtor satisfies the court of good faith towards repayment of the loan and that the bankrupt is experiencing and is likely to continue to experience financial difficulty that prevents repayment of the student loan debt. An application for discharge on the basis of hardship may only be made after at least five years have elapsed from when the student ceased to be a full- or part-time student.

In an effort to assist those who demonstrate financial need, however, the Canada Student Loan Program offers several repayment assistance measures. For example, it offers eligible students relief measures such as (a) the Repayment Assistance Plan, (b) the Repayment Assistance Plan for Borrowers with a Permanent Disability, and (c) the Severe Permanent Disability Benefit.Footnote 37

Some stakeholders have suggested that, despite relief measures available under student loan programs, the five-year waiting period in the case of hardship is unwarranted. They argue that obtaining debt relief can be difficult and that, in any event, a hardship discharge is only available if the debtor convinces a court that the hardship is a continuing event that will prevent payment in the future. In their view, this removes the need for a waiting period.

Stakeholders are invited to make submissions regarding the current hardship discharge provisions.

Partial Release of Debts

Under the hardship discharge provision,Footnote 38 the courts have found that they do not have the authority to order a release of part of the student loan debt; either all or none of the debt is to be released by court order. Some stakeholders have suggested that it may be appropriate to give the courts more discretion to release a portion of debt where warranted.

Stakeholders are invited to makes submissions regarding possible flexibility for court-ordered partial discharges on hardship grounds, including any factors the court should consider in exercising its discretion.

Commercial Issues

Introduction

In the commercial insolvency context, debtors and creditors have numerous options for dealing with severe financial distress. The BIA provides a rules-based framework for bankruptcy and proposals (e.g. restructuring) by businesses of any size. The CCAA provides a more flexible court-driven framework for reorganizations by companies with at least $5 million in debt. Secured creditors may also opt to put in place a receivership in many circumstances. Corporations have also increasingly been turning to arrangement provisions under corporate legislation, such as the Canada Business Corporations Act.

The 2008-2009 reforms were designed to encourage restructurings of viable but financially-distressed firms because the benefits of a successful reorganization include the likelihood of greater returns to creditors than in bankruptcy, preservation of jobs and relationships with suppliers and lenders, and ensuring that assets remain productive to the overall benefit of the Canadian economy.

The Sarra Report

During summer 2011, Dr. Janis SarraFootnote 39 conducted eleven public hearings regarding Canada's commercial insolvency regime. This work was supported by the Canadian Insolvency Foundation. Based on the hearings, Dr. Sarra published a report titled "Examining the Insolvency Toolkit: Report of the Public Meetings on the Canadian Commercial Insolvency Law System"Footnote 40 (the "Sarra Report").

Industry Canada greatly appreciates the contribution made to the Canadian public policy debate by Dr. Sarra and all of those who participated in the public hearings.

Encouraging Innovation through Intellectual Property Rights

Creating an economic climate that encourages innovation is considered a vital component of a country's long-term competitiveness. Intellectual property (IP) rights, such as patents and copyrights, play an important role in promoting innovation. IP statutes promote innovation through the incentive of a temporary monopoly and at the same time ensure reasonable access to users, and preserve marketplace integrity (e.g. trade-marks). IP laws focus on the rights of creators and licensees, while insolvency laws focus on the interests of debtors and creditors. However, as economic framework legislation, both IP law and insolvency law can promote innovation and marketplace integrity by mitigating entrepreneurial risks. Insolvency law can provide investors with commercial certainty in the case of default, which facilitates investment in the development of innovative ventures, as well as businesses that rely on the authorized use of IP through licences.

Copyright and Patented Items

There are existing provisions in the BIA regarding rights of holders of patentsFootnote 41 and copyrights.Footnote 42 It has been suggested that these provisions should be modernized, to better reflect the importance of IP rights in the Canadian economy. For example, the provisions related to copyright speak of "manuscripts" that have been "put into type". The archaic language creates difficulties when the copyright in question is software, for example.

Additionally, some stakeholders have called for greater rights for IP producers and creators in insolvency proceedings, enhancing the limited rights that currently exist. For example, it has been suggested that the protection for patentees could be extended to other IP, such as trade-marks. It has also been suggested that the bankruptcy provisions be extended to CCAA restructurings and receiverships.

2009 Amendments—Rights of IP Licensees

Effective licensing rights are essential to a robust IP marketplace, as licensing gives innovators a way to monetize their works and release the innovation into the marketplace during the IP's period of statutory protection. Legislative amendments in 2009 were aimed at reducing the uncertainty faced by IP licencees in an insolvency restructuring. The reforms expressly permit the disclaimer of IP licences, in order to give debtors and the courts the flexibility to restructure. However, IP licencees may preserve their rights to use the IP as long as they continue to perform their obligations under the licence.

The reforms were viewed as a positive step forward but some commentators have observed that there are outstanding issues regarding IP licences in insolvency. For example, the licencee protection only applies if the licensor restructures but not in bankruptcy or receivership. Others have noted that the new provisions only refer to the licensee's "right to use" the IP in question and do not require the licensor to provide upgrades or maintenance of the technology that may have been included in the IP licencing agreement. It has been noted that, while the amendments protect a licensee against a disclaimer, an insolvent licensor could sell IP free and clear of current licenses. Some commentators have called for additional legislative guidance to assist in this judicial balancing of interests.

Submissions are invited regarding how to improve the existing rules to support the objective of encouraging innovation, while also balancing the competing interests in an insolvency proceeding.

Encouraging Restructuring

Streamlining Companies' Creditors Arrangement Act Proceedings

The CCAA sets out a court-driven insolvency proceeding. In order to commence a CCAA proceeding, an initial court order is required. Typically, the order provides for a stay of proceedings against the debtor company, appoints a monitor and sets out the rights and powers of the debtor company during the proceeding, including the ability to carry on business, sell assets and terminate employees. It may also provide for interim financing in order to provide liquidity to fund operations during the proceedings. The debtor company typically returns to the court for approval of various steps in the restructuring process, such as the sale of assets, settling contentious claims or dealing with out-of-the-ordinary-course transactions. Finally, court sanction of a plan of arrangement and distribution of assets to creditors is required.

Concerns have been expressed by stakeholders regarding the complexity and cost of CCAA proceedings. The following issues have been raised as areas of concern in existing practice.

Initial Orders

Some stakeholders have expressed the concern that initial orders can be too broad, which can negatively affect creditors since it may be difficult to successfully challenge decisions that have been acted upon (e.g., where interim financing has been accessed by the debtor). Some stakeholders have suggested that a short automatic stay period (i.e., five to 15 days) followed by an initial court appearance may provide more creditors with the opportunity to appear before the court. The automatic stay could provide limited authority to ensure the debtor company is able to "keep the lights on". Alternatively, the statute could restrict an initial order to what is necessary to allow the debtor to carry on business for a short period until there is a court hearing or notice to creditors.

Stakeholders are invited to make submissions regarding the breadth of initial orders and potential options for streamlining the process.

Claims process

In CCAA restructurings, the time and cost associated with resolving claims can be prohibitive. Some stakeholders have suggested that a default mechanism for determining claims may be appropriate, particularly in smaller CCAA proceedings. The Sarra Report notes that in Alberta the monitor or a court-appointed claims officer determines the amount of claims owing and that amount is accepted unless the creditor objects within a specified period.Footnote 43

Stakeholders are invited to make submissions regarding the existing claims process and whether consideration should be given to a default process.

Court Applications

Significant resources can be dedicated to court applications in many larger CCAA proceedings. The consequence is increased cost for all parties and potentially reduced recovery for creditors. Some stakeholders have suggested that the debtor company could be statutorily authorized to take specified actions or the monitor could be authorized to approve certain actions by the debtor without requiring court sanction. It has also been suggested that the monitor could be granted more authority to mediate or settle disputes.

Stakeholders are invited to make submissions regarding the existing role of court appearances in CCAA proceedings and whether consideration should be given to possible approaches to reduce the number and cost of such court appearances.

Balancing Competing Interests

Role of Unsecured Creditors

Unsecured creditors can be diverse and unorganized, making it difficult for them to have an effective voice in a corporate restructuring. Some stakeholders have suggested that a mandated committee, with professionals paid for by the debtor, could create a more balanced playing field. Other stakeholders, however, have suggested that unsecured creditors' committees would simply create further delays and increase costs (see, for example, Professional Fees in CCAA proceedings below). Some view the existing provisions, which authorize the court to appoint professionals to represent specific creditors, as sufficient.

Stakeholders are invited to make submissions regarding the effectiveness of the existing provisions and other potential mechanisms to ensure an effective voice for unsecured creditors in restructuring proceedings.

Acting in Good Faith

The Sarra Report suggests that since there is no obligation on parties in a CCAA proceeding to act in good faith, creditors may take positions during the bargaining process that they know have little chance of being approved but that will improve their position relative to other creditors. It is suggested that such strategies have the potential to undermine the integrity of the insolvency system and a constructive bargaining process.Footnote 44

Stakeholders are invited to make submissions regarding whether the CCAA should expressly address whether parties to proceedings have a duty to act in good faith.

Eligible Financial Contracts

Under the BIA and CCAA, eligible financial contracts (EFCs) enjoy "safe harbour" provisions that permit them to be terminated, netted and have collateral realized despite the stay of proceedings that may be ordered by the court. These "safe harbours" were implemented in order to ensure a proper functioning derivatives market and to reduce systemic risk. Protections were also put in place in the BIA and CCAA to prevent an insolvent debtor from terminating or assigning an EFC as they could potentially do with other contracts.

The Insolvency Institute of Canada issued a report on derivativesFootnote 45 that recommended several actions be taken with respect to EFCs. First, it was recommended that the insolvent party, the trustee, the receiver or the liquidator be permitted to terminate or assign EFCs, subject to certain restrictions. It was also recommended that "walk-away" clauses, which permit a solvent counterparty to refuse to make net termination payments owing to the insolvent party in the event of an insolvency, should be rendered ineffective. The report also recommended that financial collateral securing an EFC be exempted from the existing deemed trusts (e.g. for employee withholdings) and super-priorities (e.g. for unpaid wages, pension contributions). At the same time, the report recommended that financial collateral should be limited to assets that are no longer under the control of the insolvent party, either through assignment or pursuant to a title transfer credit support agreement. The report also recommended that similar rules be applied in receiverships.

On this issue, the Sarra Report suggested EFCs, such as credit default swaps (CDS), may lead to an uncoupling of legal and economic interests and may change creditor behaviour. The Sarra Report also suggests that consideration be given to new types of derivatives that have emerged in recent years that do not fit within the original intention of the EFC safe harbour provisions.Footnote 46 The Sarra Report noted that derivatives could be made subject to the CCAA stay of proceedings, except with leave of the court, and that a process could be put in place to determine whether particular EFCs should be stayed or disclaimed.Footnote 47

Stakeholders are invited to make submissions regarding eligible financial contracts, and their impacts on insolvency and restructuring proceeding, as well as potential policy responses.

Professional Fees in CCAA Proceedings

The issue of professional fees in large corporate insolvencies has received increased attention from stakeholders and insolvency professionals in Canada and elsewhere. Reliable data regarding professional fees in Canadian insolvency proceedings are not currently available. Concerns have been raised that the expense of CCAA proceedings has been growing and may deter businesses use of insolvency proceedings in favour of alternatives that may not properly protect the interests of all creditors and stakeholders. Some stakeholders have also raised concerns that elevated professional fees can harm creditors' recoveries.

Under the CCAA, the court is responsible for reviewing fees charged to the debtor company to ensure they are "fair and reasonable". Parties to the proceeding are entitled to challenge fee applications and the court may reduce or reject fees where warranted. There is no obligation to report professional fees to the OSB or other parties, although they are available in the court record.

Other countries are examining the impact of professional fees on their respective insolvency systems, and the potential role of regulators and professional bodies. For example, in the United States, a guideline regarding attorneys' fees in larger Chapter 11 cases came into force on November 1, 2013.Footnote 48 Among other things, legal firms must disclose their non-bankruptcy blended hourly rate, hours and fees per task, and make their billing data available to the court, the U.S. Trustee and major parties to the proceeding. The guideline also sets out approaches for examining fees to ensure they are appropriate. The United KingdomFootnote 49 and AustraliaFootnote 50 are also examining this issue.

Stakeholders are invited to make submissions regarding the impact of professional fees on insolvency proceedings, including the utility of greater disclosure practices.

Enhancing Transparency

Creditor Lists

Currently, the CCAA requires the monitor, within five days after an initial order is made, to prepare a list of creditors and to make it publicly available.Footnote 51 The Sarra Report raised the idea of requiring the debtor company to continuously maintain and disclose a creditor list in order to provide more transparency regarding interested parties in the proceeding.Footnote 52 Unsecured creditors, such as trade creditors and suppliers, may be able to use the information to better organize. It could also provide information about creditors that can assist in formulating bargaining positions. However, some stakeholders noted that developing and updating a creditor list can be time consuming and expensive, especially if there is active debt trading. This could have the effect of distracting the debtor company from its primary objective of achieving a successful restructuring.

Stakeholders are invited to make submissions regarding imposing an obligation on the debtor company to maintain a creditors' list during a CCAA proceeding.

Empty Voting and Disclosure of Economic Interests

Under the CCAA, creditors have the right to vote on a plan of arrangement or compromise, based on the expectation that they have an economic interest in the success of the restructuring. Stakeholders, however, have raised concerns that as a result of changes in the marketplace, not all creditors may have the same incentives to support a restructuring. In particular, stakeholders have raised concerns regarding the impact of the trading in distressed debt and the potential effects of credit default swaps on creditor incentives and decision making.

Distressed debt trading, in which existing debt is sold at a discount by initial creditors to speculative purchasers, has played an increasingly prominent role in CCAA restructurings. On a positive note, the distressed debt market gives initial creditors an opportunity to fix their losses at an early stage and exit the insolvency proceeding. On the other hand, through purchases of debt at a discount, the purchaser can acquire a more significant voting position than warranted by their economic exposure. At the same time, distressed debt purchasers may hold short-term objectives that run counter to the objective of restructuring the debtor.

Credit derivatives are a form of financial instrument that allow creditors to hedge against credit exposure and that may allow speculators to bet against a particular firm. Credit default swaps (CDS) are a common form of derivative to protect against credit loss, in which a buyer obtains protection from the seller in case of a "credit event", such as default, restructuring or bankruptcy, for a fixed period. Unlike traditional credit insurance, the amount of compensation that can be claimed under a CDS is not limited to the actual loss suffered, there is no automatic right of subrogation and the CDS buyer or seller is not required to hold an actual interest in the hedged debt. It has been suggested that given these characteristics of a CDS, a creditor who holds CDS positions may have disincentives to support a workout or restructuring. Alternatively, a CDS holder may have different incentives in a restructuring proceeding than an unhedged creditor. The lack of transparency with respect to CDS holdings can mean that the restructuring company and unhedged creditors may be unaware of the motives of hedged creditors and their incentives with respect to the outcome of the restructuring process.

It has been suggested that the potential for misalignment of creditors' interests caused by distressed debt trading and credit derivatives, including CDS, may be mitigated by empowering the court to take account of actual economic interests when considering approval of a restructuring plan. Additionally, increased disclosure requirements could provide other creditors with vital information to understand and respond to the incentives of hedged creditors. Others have stated that disclosure and consideration of true economic interests instead of nominal debt holdings could lead to potential negative repercussions in the distressed debt and credit derivative markets.

Stakeholders are invited to provide input on whether courts should be empowered to require greater disclosure of creditors' actual economic interests or to take account of those interests.

Role of the Monitor

Under the CCAA, an insolvency professional is appointed to monitor the business and financial affairs of the debtor (the "monitor").Footnote 53 As described in the Sarra Report:Footnote 54

"Monitors are relied on by the courts and the parties to provide information and their views on the financial condition of the debtor, the efficacy and fairness of sales processes or DIP financing arrangements, and their impartial opinion on a host of other issues that arise during the proceeding. Integrity and independence are hallmark attributes of a good monitor."

In 2009, the role of the monitor received statutory clarification, with particular focus on the duty to provide notice to stakeholders and informed guidance to the court.Footnote 55 The Superintendent of Bankruptcy also became the regulator for monitor conduct, and a detailed professional conduct regime was added to the CCAA.Footnote 56 As noted in the Sarra Report, the role of the monitor is continuing to evolve.Footnote 57

Pre-Filing Reports

A relatively new development is the monitor's "pre-filing report", which is a description of the debtor company's affairs up to the date of a CCAA filing. The report is prepared for the purposes of the initial application and, hence, prior to the monitor's appointment. Pre-filing reports have been found by the courts and insolvency professionals to be beneficial, as they provide timely information to the court. It has been suggested, however, that the monitor's ability to exercise the requisite attribute of independence, prior to receiving a court appointment, is debatable. It has also been suggested that monitors be precluded from introducing evidence in pre-filing reports.

Stakeholders are invited to make submissions regarding whether pre-filing reports should be permitted and, if so, in what circumstances.

Conflict of Interest

The court, creditors, and other stakeholders rely on the monitor to maintain an impartial perspective when providing information on the restructuring process. However, in some CCAA restructurings, the monitor has a pre-existing relationship with the debtor company, for example having acted as the debtor company's financial advisor, which can raise questions as to the monitor's independence.Footnote 58 In larger CCAA cases, the debtor company often has separate financial advisors who act independently of the monitor, thereby reducing the potential for real or perceived conflicts of interest. In small- to medium-sized CCAA cases, however, the monitor has often acted as the debtor company's financial advisor pre-filing, raising concerns as to the monitor's impartiality. Some commentators have suggested that such a pre-filing relationship can facilitate a successful restructuring and reduce costs, as the monitor already has knowledge of the debtor company's financial situation. Further, the risks of conflicts are mitigated by the fact that monitors are professionals that are subject to various forms of oversight: they must comply with professional codes of conduct,Footnote 59 are subject to appointment restrictions,Footnote 60 and are also subject to oversight by the OSB and the court.Footnote 61 Others have noted that while a monitor that has acted as a financial advisor to the debtor company may improve the efficiency and reduce the costs of a CCAA restructuring, further measures such as disclosure of the monitor's relationship with the debtor company may be necessary in addition to OSB and court oversight.

Stakeholders are invited to make submissions regarding whether additional measures are necessary to address the potential for conflicts of interest where a monitor has a pre-filing relationship as financial advisor to a debtor company.

Asset Sales

Credit Bidding

Credit bidding refers to the ability of a creditor to use a claim as a form of currency during asset sales in an insolvency proceeding. Canadian legislation is silent regarding credit bidding, but courts have permitted it.Footnote 62 The United States Bankruptcy Code specifically provides that a lien holder may bid its allowable claim in a sale of the property unless the court orders otherwise.Footnote 63

The Sarra Report notes concerns inherent to credit bidding, particularly with respect to imbalances of power in favour of, and information available to, secured creditors. Such imbalances could reduce the likelihood of competing bids, thereby reducing the potential value of the assets being sold.Footnote 64

Stakeholders are invited to comment on whether credit bidding should be permitted and, if so, what limitations may be appropriate.

Stalking Horse Bids

A stalking horse bid is an initial bid that sets a minimum floor for the eventual sale of assets. While insolvency legislation is silent regarding such bids, Canadian courts permit this type of sales process regularly.

The Sarra Report suggests that stalking horse bids deliver "the message day one to customers, suppliers, employees and other key stakeholders that the business will carry on, and that there is an informed party that has faith in and is committed to the business."Footnote 65 It also notes that courts have considered four criteria in assessing a stalking horse bid process: the degree of control exercised over the initial stage to determine the stalking horse bidder; the need for a stalking horse bid as opposed to a traditional sales process; the economic incentives (break fees and other protections) granted to the bidder; and, whether sufficient time is permitted for other bidders to consider topping the credit bid.Footnote 66

Stakeholders are invited to comment on whether stalking horse bids should be expressly permitted under Canadian insolvency legislation and, if so, what limitations may be appropriate.

Applicability of Asset Sale Test

Asset sales are subject to court approval if they are made outside of the ordinary course of business.Footnote 67 Some stakeholders have suggested that it is unclear when sales are material enough to become exposed to the court approval process. Because court approval of sales outside the ordinary course of business must take into account how the sale could impact on the payment of wage and pension claims,Footnote 68 stakeholders have suggested a materiality test should be created to ensure court approval is sought when appropriate.

Stakeholders are invited to comment on whether a materiality test is required to determine when asset sales will be subject to court approval.

CBCA Arrangements

The Canada Business Corporations Act (CBCA) permits a corporation to undertake an "arrangement" in order to effect a corporate change that would not be feasible under any other provision of the Act.Footnote 69 Typically, an arrangement is used to conduct a series of changes to a corporation's structure, including mergers, amalgamations and divestitures. In recent years, arrangements have been used to restructure the affairs of insolvent corporations.

The reasons for choosing to restructure under the CBCA rather than insolvency legislation may include the speed and flexibility under which an arrangement can be accomplished; that the debtor's management remains in control of the corporation; that there is no oversight by an independent party such as a monitor; that there are no reporting or other requirements to creditors; and, that it avoids the stigma associated with insolvency.

The CBCA requires that the corporation effecting an arrangement be solvent. Courts have interpreted this to mean that the applicant corporation need be solvent but other affected corporations may be insolvent. As such, some corporations have bypassed the solvency requirement by creating a solvent shell company that is then used as the applicant.Footnote 70

The Director under the CBCA has published a policy statement regarding the use of CBCA arrangement provisions by financially distressed corporations which indicates that corporations must be in compliance with the solvency provisions of the legislation.Footnote 71

Stakeholders have expressed concern with the CBCA arrangement provision because it is skeletal, providing the court broad discretion to make "any interim or final order it thinks fit".Footnote 72 As a result, there may be insufficient protections for creditors and a general lack of safeguards compared to insolvency legislation, which strives to balance the competing interests of various affected parties. It has been suggested that insolvency-type protections could be incorporated into the CBCA arrangement provisions. Alternatively, the Sarra Report suggested that it may be appropriate to consider changes to the CCAA in order to respond to the issues that drive parties to use the CBCA.Footnote 73

Stakeholders are invited to provide input regarding the practice of CBCA arrangements involving insolvent companies.

A Streamlined Small Business Proposal Proceeding

The cost of the existing Division I proposal process may be significant and can be prohibitive in the context of small- and medium-sized enterprises (SMEs). It may be appropriate to consider creating a simplified and less expensive proposal process intended to make it easier for SMEs to restructure. Some stakeholders have suggested that certain steps in the process could take place automatically (e.g., 45-day extension of the stay of proceedings), subject to creditors' rights to object.Footnote 74

Stakeholders are invited to make submissions regarding whether a simplified, less expensive proposal process for SMEs would be warranted.

Division I Proposals Extension

A Division I proposal must be filed within six months of the filing of a notice of intention.Footnote 75 It has been suggested that the time limit may hinder the debtor's ability to obtain creditor approval, particularly in more complex commercial proceedings.Footnote 76 Some stakeholders have suggested permitting the court to extend the time limit in exceptional circumstances where clear criteria exist for granting an extension.Footnote 77 On the other hand, other stakeholders have expressed concern that it could lead to abuse of the stay if the length of proceedings is too long.

Stakeholders are invited to provide input on extending the time for filing a Division I proposal following the filing of a notice of intention to file a proposal.

Liquidating CCAA Proceedings

The CCAA was originally envisioned as a restructuring tool. In recent years, courts have noted an increase in the number of liquidating CCAA filings,Footnote 78 meaning that the Act is used to sell the assets — typically as a going concern business — and proceeds are distributed among the creditors. Stakeholders have expressed concern with the appropriateness of liquidating CCAAs because there is often no opportunity for creditor approval. Additionally, there can be pressure on the court to approve sales as there is no other going-forward solution. The sales may avoid many of the checks and balances provided by the plan approval process.

Some stakeholders have expressed the view that if liquidating CCAA proceedings are to continue, the CCAA should provide protections and add principles for the court to consider in determining whether to approve the sales processes. Other stakeholders have strongly supported maintaining judicial flexibility to permit the tailoring of appropriate solutions in the particular circumstances of the case.

Stakeholders are invited to provide input on whether the CCAA should be amended to codify protections for stakeholders and principles for the courts to consider in liquidating CCAA proceedings.

Enhancing Equity

Employees' Claims

Notable commercial insolvencies, including Nortel Networks and AbitibiBowater, have raised concerns about debts and obligations owed to employees, former employees and pensioners (together referred to as "employees"). Employees' claims can include unpaid wages, vacation pay, severance and termination pay, long-term disability benefits, pension obligations as well as other employment benefits, such as dental, drug and extended healthcare plans.

Currently, employees benefit from numerous legislative and regulatory protections, as well as government programs, not available to other creditors:

- In bankruptcy and receivership:

- Pre-filing unpaid wages and vacation pay are granted a super-priority over cash, accounts receivable and inventory for up to $2,000 per employee,Footnote 79 plus up to $1,000 super-priority for disbursements incurred as part of their employment:Footnote 80

- To the extent such claims are unfulfilled by the super-priority, they are granted a preferred claim over all of the debtor's remaining property;Footnote 81

- Unremitted normal cost pension contributions are granted a priority over secured creditors without limit;Footnote 82

- Pre-filing unpaid wages and vacation pay are granted a super-priority over cash, accounts receivable and inventory for up to $2,000 per employee,Footnote 79 plus up to $1,000 super-priority for disbursements incurred as part of their employment:Footnote 80

- In restructuring proceedings, a proposal or plan of arrangement or compromise must provide for the payment of:

- Pre-filing unpaid wages and vacation pay of up to $2,000 per employee;Footnote 83

- Post-filing wages, vacation pay and disbursements;Footnote 84

- Unremitted normal cost pension contributions;Footnote 85

- The federal Wage Earner Protection Program (WEPP) pays eligible workers up to approximately $3,600 for unpaid wages, vacation pay, and severance and termination pay. The WEPP is subrogated to the employees' claim for up to the amount of the super-priority;

- The BIA and the CCAA both respect the pension fund trust created under federal or provincial pension legislation, meaning that the amounts held in that pension fund trust are only available to pensioners and are not available to other creditors;

- The federal government announced as part of Budget 2012 that federally-regulated employers that offer long-term disability plans will need to do so pursuant to insurance rather than self-funding, meaning that an employer's failure would not affect such benefits.

In recent years, there have been calls to increase protections for employees. For example, it has been suggested that severance and termination could be included in the definition of wages, as they are currently excluded. It has also been suggested that the existing cap of $2,000 on unpaid wages could be increased or removed entirely, permitting employees to obtain priority for the entirety of their claim. With respect to pensions, some stakeholders have suggested that defined benefit pension plan deficits be prioritized, either ahead of secured creditors (i.e. a super-priority) or ahead of unsecured creditors (i.e. a preferred claim). With respect to employee benefit plans, it has been suggested that amounts owed with respect to these plans be prioritized or that the company be barred from terminating such plans without court approval.

International comparisons are imperfect due to differences in employees' claims and how such claims are treated in insolvency proceedings. Industry Canada researchFootnote 86 found that, of the member countries of the Organisation for Economic Co-operation and Development (OECD) for which information was ascertainable, most — like Canada — provide some form of priority for employees' remuneration in insolvency proceedings. In almost all cases, the insolvency priority is capped either in amount, by a specified time period, or both. Many countries also offer a wage guarantee fund similar to the WEPP. With respect to pensions, many OECD countries with private pension plans provide a preferred claim in insolvency for outstanding contributions. Canada exceeds this by providing a super-priority. Pension deficits are by and large treated as unsecured claims in OECD countries, as is the case in Canada.Footnote 87 Finally, with respect to employee benefit plans, the United States Bankruptcy Code provides that retiree benefit plans cannot be modified or terminated in a restructuring proceeding without court approval.Footnote 88

Concerns haved been expressed by some stakeholders, however, that any enhancement in the existing super-priority or preferred claims could result in lenders reducing credit available to employers and change behaviour of unsecured creditors, such as suppliers who may impose more restrictive trade credit practices (e.g. shorter payment terms). Industry Canada understands that some manufacturers experienced a reduction in credit availability in 2008, when the $2,000 super-priority was first introduced. Any increase in the amount of the priorities could be anticipated to further negatively impact on credit availability, particularly for small and medium-sized enterprises which have fewer assets against which to apply the super-priority. The House of Commons Standing Committee on Industry, Science and Technology considered Bill C-501 that proposed prioritizing pension claims. The Committee heard from numerous witnesses and decided to oppose the Bill's pension-related provisions due to concerns about their potential negative impact on the Canadian economy.

Stakeholders are invited to make submissions regarding whether, and how, Canada could enhance protection of employee claims in insolvency proceedings.

Employees' Claims in Asset Sales

Under the CCAA, a plan of arrangement or compromise may not be sanctioned by a court unless it provides for the payment of unpaid wages of up to $2,000 per employee and all unremitted normal cost contributions owed to a pension plan.Footnote 89 In recent years, however, the Act has been used more often to affect a liquidation of the debtor company (see discussion of "Liquidating CCAAs" above). In these circumstances, there is no plan of arrangement or compromise. In order to ensure that the asset sales that occur in a liquidation scenario do not defeat the requirement that these claims be paid, the Act provides safeguards.Footnote 90 As noted above at "Asset Sales", however, not all sales are conducted under the safeguard provisions, and for those that are it may be difficult to determine if they satisfy the safeguard provisions.

Stakeholders are invited to make submissions regarding whether the existing provisions adequately protect the employees' claims.

Hardship Funds