To obtain a copy of this publication or an alternate format (Braille, large print, etc.), please fill out the Publication Request Form at www.ic.gc.ca/Publication-Request or contact the:

Web Services Centre

Industry Canada

C.D. Howe Building

235 Queen Street

Ottawa, ON K1A 0H5

Canada

Telephone (toll-free in Canada): 1-800-328-6189

Telephone (Ottawa): 613-954-5031

TTY (for hearing-impaired): 1-866-694-8389

Business hours: 8:30 a.m. to 5:00 p.m. (Eastern Time)

Email: ic.info-info.ic@canada.ca

Permission to Reproduce

Except as otherwise specifically noted, the information in this publication may be reproduced, in part or in whole and by any means, without charge or further permission from Industry Canada, provided that due diligence is exercised in ensuring the accuracy of the information reproduced; that Industry Canada is identified as the source institution; and that the reproduction is not represented as an official version of the information reproduced, nor as having been made in affiliation with, or with the endorsement of, Industry Canada.

For permission to reproduce the information in this publication for commercial purposes, please fill out the Application for Crown Copyright Clearance at www.ic.gc.ca/copyright-request or contact the Web Services Centre (see contact information above).

© Her Majesty the Queen in Right of Canada,

as represented by the Minister of Industry, 2014

Cat. No. Iu173-6/2014E-PDF

ISBN 978-1-100-25276-6

Aussi offert en français sous le titre Nouveau départ : un examen des lois canadiennes en matière d'insolvabilité.

PDF version

Contents

- Letter from Minister James Moore

- Introduction

- Canada's Insolvency Framework

- Insolvency Trends

- Review Process

- What Canadians Said

- Conclusion

- Endnotes

- Annex A — Stakeholder Submissions

Letter from Minister James Moore

The Bankruptcy and Insolvency Act and the Companies' Creditors Arrangement Act require that the Minister of Industry report to Parliament on the provisions and operation of both Acts in 2014. I am pleased to table this report in fulfillment of that responsibility.

The Government of Canada launched a public consultation in May 2014, with the release of a Discussion Paper seeking input on key aspects of Canada's insolvency regime and its administration. The public consultations built on previous research and analysis of economic and insolvency trends by departmental officials, as well as contributions from stakeholders. The results of the review activities are captured in this report.

Insolvency laws are important marketplace framework legislation that have an impact on Canada's competitiveness. An efficient, well-functioning insolvency regime is vital to Canada's continued economic prosperity. Stakeholders told us that Canada's insolvency laws have responded well to the needs of Canadian consumers and businesses, particularly during the recent recession. At the same time, Canada's insolvency laws must evolve to meet the needs of the economy and changes in the global marketplace. Our government is committed to ensuring that Canadian insolvency legislation maintains its status among the most modern regimes in the world.

In tabling this report, I would like to thank the many Canadians who participated in the review. The extensive public feedback in response to the Discussion Paper, including input from insolvency experts, academics, and other stakeholder groups, will inform our work as the review continues in the coming parliamentary session.

The Honourable James Moore

Minister of Industry

Introduction

In 2008, the world experienced one of the deepest economic downturns since the Great Depression. Canada was not spared as we experienced a recession that was felt across Canada, a record number of personal insolvencies and the failure or restructuring of numerous businesses.

Canada's post-2008 performance led G7 countries with the highest level of job creation and one of the best growth rates coming out of the recession. Canada experienced a positive macroeconomic environment, including a low federal government debt-to-gross domestic product ratio, the lowest overall tax rate on new business investment among G7 countries, a sound approach to regulation of financial institutions and a stable, low inflation environment. These factors were reinforced by the Economic Action Plan, which responded to the global crisis by reducing taxes, investing in infrastructure, enhancing skills training, supporting sectoral and regional adjustment and facilitating business lending. Despite lingering turmoil in certain countries, Canada is projected to continue its stable growth as domestic firms reinvest to enhance their competitiveness.

Even in a growing economy, Canadians will face challenges: one of the highest consumer debt-to-income ratios in the G20 and changing demographic trends that are increasingly imposing financial burdens on the "sandwich" generation will test consumers' resilience; and globalization will present new business opportunities but also greater challenges from international competitors.

In this context, Canada's insolvency environment continues to evolve: relationship lending, which was once predominant, is declining; new players, including private equity and distressed debt traders, are presenting unique challenges to corporate restructuring efforts; financial market innovations, such as credit and other derivatives, are shifting parties' interests and incentives; and the growth in cross-border insolvency proceedings is increasing the complexity of cases and bringing new competing interests for scarce resources.

What remains constant is that there will be individuals and businesses who, for various reasons, find themselves overwhelmed by debt. For them, and for the benefit of the economy, an effective insolvency regime is necessary to ensure an efficient process to settle debts and, where appropriate, provide individuals with a fresh start and businesses with an opportunity for financial rehabilitation.

Canada's insolvency laws are well-regarded internationally and are frequently cited as a model in international insolvency panels, such as the United Nations Commission on International Trade Law (UNCITRAL). While these laws proved robust during the 2008 downturn, it is critical to ensure that they remain responsive to new challenges in the constantly evolving domestic and global economic landscapes. To that end, the Bankruptcy and Insolvency ActEndnote 1 (BIA) and the Companies' Creditors Arrangement ActEndnote 2 (CCAA) include a statutory provision that requires their periodic review. This report is a step in the review process.

Canada's Insolvency Framework

"Reorganization serves the public interest by facilitating the survival of companies supplying goods or services crucial to the health of the economy or saving large numbers of jobs."Endnote 3

Canada's insolvency regime is composed primarily of two Acts, the BIA and the CCAA. The BIA provides the legislative framework to address personal and corporate insolvency. In a bankruptcy, a trustee liquidates the bankrupt's assets and distributes the proceeds in a fair and orderly way among the creditors. Alternatively, the BIA provides procedures for insolvent consumers and businesses to avoid bankruptcy by negotiating an agreement with their creditors to reorganize their financial affairs. This is referred to as a "proposal". The CCAA provides the legislative framework for insolvent companies with more than $5 million in debt to reorganize under court supervision. It enables the insolvent company to seek a court order staying its creditors from taking action against it while it negotiates an arrangement to reorganize its financial affairs. A monitor is appointed by the Court to watch over the restructuring and provide information to the Court and creditors. While corporate restructurings can occur under either Act, the CCAA's court-driven process provides greater flexibility for judges to deal with the specific issues in the cases before them.

The Superintendent of Bankruptcy (the Superintendent) is part of the administrative framework, overseeing the functioning of the insolvency regime and ensuring its integrity. The Superintendent has statutory responsibility to supervise the administration of all estates and matters under the BIA, and regulates the trustees who administer consumer and commercial bankruptcies and proposals. The Superintendent also has certain functions under the CCAA, including maintaining a public record of CCAA proceedings and investigating complaints regarding the conduct of monitors. In fulfilling his mandate, the Superintendent sets standards and provides guidance to stakeholders regarding expected conduct through directives, notices, position papers and compliance programs.

I. History

The BIA has its roots in the Bankruptcy Act of 1919, which was substantially reformed in 1949. The BIA was further amended in 1992, 1997 and 2008-2009. The CCAA came into force in 1933 but only became a commonly used restructuring statute in the 1980's. It was amended in 1997 and 2009.

The 1992 reforms focussed on maximizing creditor value through reorganization and rehabilitation, improving the equitable distribution to suppliers and employees and improving the administration of the BIA. The 1997 reforms encouraged consumer debtor responsibility, and improved the reorganization provisions and the administration of the Acts, including the introduction of specialized provisions related to securities firms and international insolvencies.

The most recent legislative reforms, which came into force in 2009, had four main objectives: to encourage the restructuring of viable, but financially troubled, companies; to better protect workers' claims for unpaid wages and vacation pay; to make the bankruptcy system fairer and reduce abuse; and, to improve the administration of the system. Best practices that developed under the CCAA were codified in order to enhance certainty in restructuring proceedings. Unpaid wages of up to $2,000 per employee and unremitted pension contribution claims were prioritized ahead of secured creditors and collective agreements were protected. Debtors who had high income-tax debt were denied an automatic discharge from bankruptcy and those with surplus income were required to pay more into their estate and remain in bankruptcy for a longer period of time.

II. Economic Implications

"Capital and credit, in their myriad of forms, are the lifeblood of modern commerce."Endnote 4

Insolvency legislation is a key component of Canada's marketplace framework legislation that governs commercial relationships for both consumers and businesses. Certain and reliable rules provide security for investors and lenders that, in turn, influences the cost and availability of credit in the Canadian marketplace.Endnote 5 This can help attract higher levels of domestic and foreign investment while the fresh start provided by bankruptcy offers a safety net that promotes entrepreneurship.Endnote 6 Efficient bankruptcy and insolvency processes help to ensure that debtors' assets can be returned to productive use quickly, improving Canada's overall economic performance.Endnote 7 Equitable treatment of stakeholders and transparent processes also help to protect the integrity of the insolvency regime.

Although broad economic considerations are important, it is essential to not lose sight of the individuals and businesses affected by these events and who must be dealt with equitably.

III. Objectives of Insolvency Policy

"Despite the proven wisdom of the policies underpinning the insolvency legislation, it is understandable that few appreciate the 'haircuts' or even outright losses that bankruptcies trigger."Endnote 8

In a dynamic, market-based economy, insolvency is a fact of life. From time to time, individuals and businesses will encounter financial difficulty, as a result of choices made, economic downturns or personal misfortune beyond their control.

Countries have traditionally taken different approaches to the social and legal consequences of excessive debt. Canada adopted a "fresh start" policy for consumers, which relieves honest but unfortunate debtors of excessive debts. In recent years, there has been movement internationally towards the fresh start approach, which reduces costs for creditors and the negative social consequences for individuals faced with unmanageable debts.

Within the commercial insolvency sphere, Canada has encouraged the financial rehabilitation of viable, but financially distressed, businesses as that typically increases recoveries for creditors, maintains supplier relationships and protects jobs. Other countries are moving in a similar direction.

The objectives underlying the BIA and CCAA include minimizing the impact of a debtor's insolvency on all stakeholders by pursuing an equitable distribution of the debtor's assets and, where possible, by rehabilitation of the debtor. This is achieved by legislation that:

- provides certainty to promote economic stability and growth;

- maximizes the value of assets;

- strikes a balance between liquidation and reorganization;

- ensures equitable treatment of similarly situated creditors;

- provides for timely, efficient and impartial resolution of insolvency;

- preserves the insolvency estate to allow equitable distribution to creditors;

- ensures transparent and predictable insolvency laws that contain incentives for gathering and dispensing information; and

- recognizes existing creditor rights and establishes clear rules for ranking of priority claims.Endnote 9

Insolvency Trends

I. Consumer

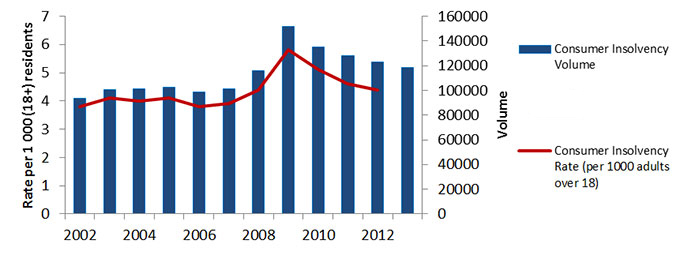

The Canadian consumer insolvency rate (the number of consumer insolvencies per 1,000 residents aged 18 years or older) has trended higher over the past few decades. This may be due to greater comfort with, and easier access to, consumer credit and reduced stigma related to bankruptcy. While the period of 2002-2007 saw a relatively stable consumer insolvency rate, the 2008 downturn pushed it to a new peak in 2009. Since that time, the rate has trended back towards pre-recession levels.

Figure 1: Consumer Insolvency Rate and Volume

Source: Office of Superintendent of Bankruptcy

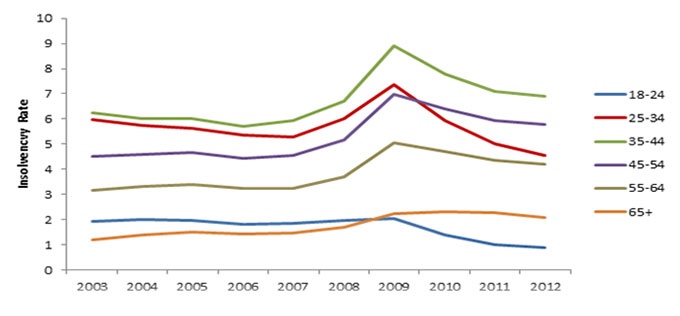

The rate of insolvencies is not evenly distributed among Canadians when viewed by age. Those aged 35-54 are at the highest risk of insolvency. Since 2008 two potentially significant trends have appeared. The consumer insolvency rates for Canadians older than 35 are higher than prior to the recession and insolvency rates for Canadians younger than 35 are lower. This could be indicative of delayed transition to financial autonomy by offspring placing greater financial burdens on parents. It is too early to determine whether the trend is an anomaly or indicative of a longer-term change.

Figure 2: Consumer Insolvency Rate by Age Cohort

Source: Office of Superintendent of Bankruptcy

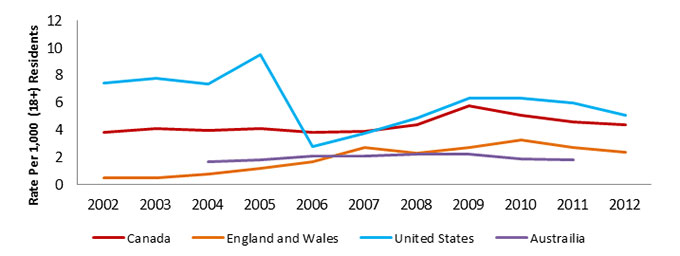

Internationally, it can be difficult to compare consumer insolvency rates because countries have taken different approaches to the social and legal consequences of excessive debt. Different levels of social stigma related to insolvency may also impact consumer insolvency rates. That being said, Canada's consumer insolvency rate appears high compared to some other developed countries.

Figure 3: Consumer Insolvency Rate: International Comparison

Source: Statistics Canada, OECD, American Bankruptcy Institute, United Kingdom Office of National Statistics, Australian Bureau of Statistics, with Industry Canada calculations.

This could be a sign that Canada's insolvency regime is readily accessible, providing Canadians overwhelmed by debt with the fresh start they need. Alternatively, it could be a sign that Canadians are not managing their use of credit appropriately. Furthermore, because Canadians have the highest debt-to-income ratio among G7 countries, consumers are more susceptible to economic shocks, such as job loss or other negative life events.

II. Business

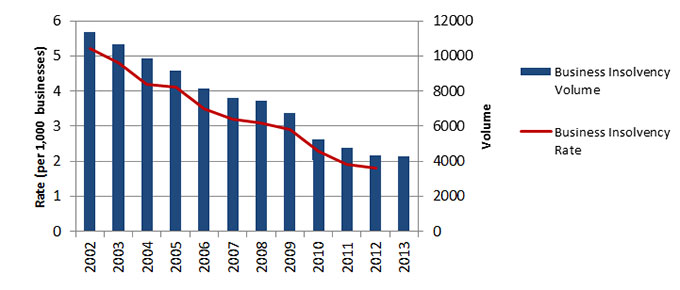

In contrast to the consumer insolvency trends, the business insolvency rate (the number of business insolvencies per 1,000 businesses operating in Canada) has fallen nearly 70 percent since 2002.

Figure 4: Business Insolvency Rate and Volume

Source: Office of Superintendent of Bankruptcy

It is unclear why the business insolvency rate continues to trend downwards. It may be related to the relatively low cost of credit during the past decade, although other countries experienced low credit cost yet saw their business insolvency rates climb. It could also be attributed to closer monitoring by lenders, resulting in remedial actions before businesses reach the tipping point into insolvency. Finally, the cost of formal insolvency proceedings may have encouraged more private workouts or business closures.

Of note, unlike other periods of economic downturn, the 2008 recession did not result in an increase in the business insolvency volume. This is consistent with anecdotal evidence that suggests lenders were hesitant to trigger defaults post-2008 as there was a very limited market for distressed assets.

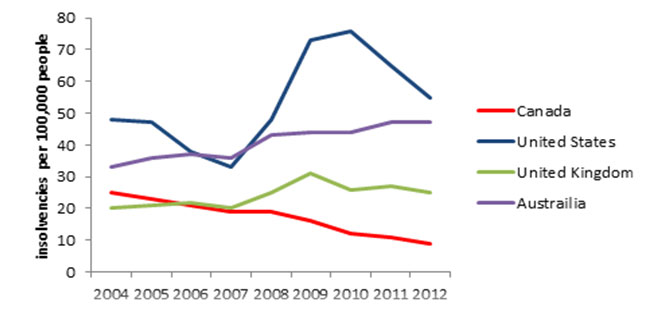

Internationally, Canada has a lower per capita business insolvency rate (the number of business insolvencies per 100,000 individuals) than comparable countries. The 2008 downturn resulted in spikes in business insolvencies in both the United States and United Kingdom whereas Canada maintained its downward trend. Australia's business insolvency rate continued to climb throughout the period.

Figure 5: Business Insolvency Rate

Source: Trading Economics; OECD; Industry Canada calculations.

Review Process

The 2009 reforms to both the BIA and CCAA require the Minister of Industry to lay before Parliament a report on the provisions and operation of the Acts.Endnote 10 Industry Canada has monitored the Canadian insolvency marketplace to identify emerging trends and issues. In early 2013, a systematic environmental scan was initiated in order to gain a comprehensive understanding of how Canada's insolvency laws are functioning. The review included an examination of academic research and expert commentary, of insolvency proceedings and judicial decisions, and of domestic and international economic and insolvency trends. It was complemented by a broad outreach effort to an array of key stakeholders, including insolvency practitioners and academics, industry associations and employee and retiree groups, among others.

In May 2014, Industry Canada launched an on-line public consultation based on a wide-ranging discussion paper (the Discussion Paper) in order to obtain the views of Canadians. More than 70 individuals and organizations made submissions on a variety of issues. Interested stakeholders were also given the opportunity to meet with Industry Canada officials to share their views in person or by teleconference. Annex A provides a list of written submissions received by the Department. The Discussion Paper and submissions may be found at:

http://www.ic.gc.ca/eic/site/cilp-pdci.nsf/eng/h_cl00870.html

This report fulfills the Minister of Industry's statutory obligation. Pursuant to the BIA and CCAA, this report is to be referred to a Parliamentary committee designated to review it and report back to Parliament within one year or such further time authorized by Parliament.

What Canadians Said

Overall, most stakeholders are generally satisfied that the BIA and CCAA achieve their objectives in an efficient manner. That being said, Industry Canada received submissions regarding a large number of issues that could be addressed to improve the functionality of Canada's insolvency regime. Below are descriptions of several key issues that generated significant stakeholder commentary. The list is not intended to be exhaustive nor is it intended to exclude other issues. Industry Canada intends to continue to examine all matters raised in the public consultations.

I. Consumer Issues

Registered Disability Savings Plans – When an individual becomes bankrupt, the trustee gathers together the bankrupt's assets for distribution to the bankrupt's creditors. The BIA, however, provides that the bankrupt is entitled to keep certain property that is exempt under provincial law and the BIA (e.g. personal belongings, work tools, pension entitlements and funds held in registered retirement savings plans).

Stakeholders expressed a strong preference to see an exemption added to the BIA for registered disability savings plans, which are intended to provide for the financial needs of severely disabled individuals when those who care for them are no longer able to provide support.

Licence Denial Regimes – Provinces are responsible for issuing licences or permitting Canadians to engage in certain activities, such as driving. Some provinces have linked the ability to obtain or renew a licence to the payment of debts owed to the province or other specified entities. While this is within the province's authority in normal circumstances, it creates a conflict with the bankruptcy regime if the provincial legislation permits a creditor to demand payment outside the insolvency process, instead of inside the process like all the other unsecured creditors.

There was stakeholder consensus that licence denial regimes – to the extent they purport to apply to debts released in bankruptcy – violate the fresh start principle and could have a significant, negative impact on the bankrupt and other creditors. As a result, stakeholders suggested that such regimes should not apply to debts released in bankruptcy.

Family Law and Equalization – Family law and insolvency proceedings often intersect. In recognition of the social importance of family-related obligations, the BIA provides that spousal and child support orders are not releasable in bankruptcy. In a recent case before the Supreme Court of Canada,Endnote 11 a spousal claim for an equalization payment against property that was exempt from seizure under provincial law as against other creditors – but not as against a claim for equalization – was defeated. The Court suggested that as a matter of fairness insolvency law should ensure that such claims are protected in the future.

Stakeholders agreed with the Court's assessment that the BIA should expressly protect equalization claims against exempt property held by the bankrupt.

Reaffirmation Agreements – Through bankruptcy proceedings, an individual can have most of his or her debts released. In some cases, however, the bankrupt may wish to "reaffirm" (i.e. reinstate) a debt obligation for specific reasons. For example, anecdotal evidence suggests that car loans are often reaffirmed in order to permit the bankrupt to continue to use a vehicle that is required for work, especially in rural areas. Currently, a bankrupt may reaffirm a debt either through a written contract or by conduct (e.g. by making a payment on the debt following discharge from bankruptcy).

Stakeholders expressed concern that reaffirmation defeats the fresh start principle. There was also concern that bankrupts might not realize the consequences of reaffirmation by conduct. As a result, the majority of stakeholders were supportive of limitations in the BIA on reaffirmation by conduct.

There was no consensus regarding other consumer issues that were identified in the Discussion Paper, including responsible lending, consumer deposits, implementation of a federal exemption list and discharge of student loans.

II. Commercial Issues

Intellectual Property – The knowledge-based economy continues to expand in importance in addition to the manufacturing-based, bricks-and-mortar economy. Stakeholders told us that it is crucial that Canada's insolvency laws respond as effectively to financial distress involving intangible and intellectual property as they do to "hard" assets, such as real estate, equipment and inventory.

On this topic there was substantial consensus that Canada's insolvency laws require significant modernization. It was recognized that amendments implemented in 2009 were a positive first step but that they were not broad enough to address all of the shortfalls. There remain aspects related to intellectual property for which there were calls for change, including modernizing the language related to the existing provisions on copyright and patents and ensuring that all types of intellectual property are recognized and properly treated.

Priorities – Bankruptcy is often described as a "zero-sum game" because there are finite and insufficient assets available to satisfy the bankrupt's debts and liabilities. Changing the ranking according to which creditors are entitled to be paid would impact all creditors. This could, in turn, affect the cost and availability of credit for Canadians. As noted by the Standing Senate Committee on Banking, Trade and Commerce, "…the availability of credit at reasonable cost has implications for the levels of domestic and foreign investment, entrepreneurship and innovations, and personal investment and consumption."Endnote 12

In response to the Discussion Paper, there were calls from employee groups, pensioners, fresh produce sellers, small businesses and tax authorities seeking priority payment on the basis that they experience different vulnerabilities and, therefore, are in need of special protection. It was conveyed that there is a need to consider the unique risks and challenges in different sectors of the economy. On the other hand, lenders and insolvency practitioners suggested caution in considering these types of requests due to the potential impacts on credit cost and availability, particularly for financing of inventory that is related to farming. Some stakeholders recommended that options outside of insolvency should be considered in order to offer more secure protection for socially important claims and to protect the integrity of insolvency proceedings.

Streamlined Proceedings – Insolvency proceedings, particularly corporate restructurings, can be complex, requiring significant time, effort and expertise. As a result, one of the key issues for insolvency law is to put in place efficient processes that permit a quick resolution, while ensuring fairness through necessary checks and balances.

In the CCAA context, most stakeholders supported streamlining measures, such as reducing the need for court approval of interim actions. Better disclosure of professional fees was also raised although there was no consensus on concrete actions that should be taken.

Stakeholders also suggested that the cost of restructuring under existing mechanisms is often too high for small and medium-sized businesses. This would suggest a more streamlined proceeding may be warranted, especially given the importance of small business entrepreneurs in driving the economy.

Cross-border Insolvencies – Globalization continues to transform the world's economy and create new markets and opportunities for Canadian workers and businesses. At the same time, as business becomes more international, the number of cross-border insolvencies has also increased.

Some stakeholders suggested that reforms may be necessary to ensure Canada's insolvency laws keep pace with globalization trends. They pointed to work being undertaken by UNCITRAL's insolvency working group, in which Canada is an active participant. Others, however, cautioned that any potential reforms should take into account the conditions necessary to promote investment in Canada and to protect the legitimate interests of Canadian firms in global markets.

Financial Contracts – Innovation in the financial markets has resulted in continual evolution of products that assist business and investors in managing risks, including credit risk. It is in the intersection of these financial instruments and insolvency law that stakeholders are seeing emerging issues that may require policy responses to ensure that the balance in insolvency proceedings is maintained.

Most stakeholders indicated support for measured disclosure requirements, which would provide greater transparency for other creditors and the courts. There was no consensus regarding possible changes to rebalance the competing interests between those who use these financial products and other insolvency stakeholders.

III. Administrative Issues

Accessibility – The insolvency regime provides Canadians with unmanageable debts a potential for a fresh start. The administration of files is carried out by private sector trustees. This means that the cost of accessing the insolvency system is based, to a certain extent, on market forces. Existing measures, such as the Bankruptcy Assistance Program and agreements to pay trustee fees post-discharge under the BIA, are intended to ensure access to bankruptcy.

Some stakeholders have suggested that there may still be accessibility issues as the cost of a simple bankruptcy, estimated to be as high as $1,500, may be too high for low and no-income individuals. They suggested that new options could be developed to ensure better access to the insolvency regime.

Legislative Structures – Currently, Canada's insolvency regime is implemented by a number of different laws under the mandate of different Ministers: the BIA, CCAA and the Canada Business Corporations Act fall under the responsibility of the Minister of Industry; the Winding-up and Restructuring Act, which can be used by certain corporations and financial institutions, falls under the shared responsibility of the Ministers of Industry and Finance; the Canada Transportation Act, under the Minister of Transport, can be used to resolve the insolvency of certain railway companies; and, the Farm Debt Mediation Act, under the Minister of Agriculture and Agri-Food, is available to insolvent Canadian farmers.

While there was little consensus as to concrete action, many stakeholders expressed support for rationalization of the current legislative structure.

Modernization – The BIA was last comprehensively reformed in 1949, with significant amendments being made on several occasions since 1992. Some stakeholders suggested that a comprehensive review of the BIA may be warranted in order to remove outdated concepts and provisions. Other stakeholders suggested that the role and powers of the Superintendent could be enhanced.

Stakeholders also raised a number of issues that are tangential to insolvency law policy, including taxation issues, the operation of the Wage Earner Protection Program, and regulation of pensions. These matters could impact on the effectiveness and efficiency of the insolvency regime and could be considered in the context of the review.

Conclusion

The 2008 economic downturn led many developed economies into a deep recession. Canada's experience was better than most as a result of positive actions taken to address the downturn yet, still, a significant number of Canadians suffered personal insolvency and major firms failed. The BIA and CCAA were up to the challenge and played their part by providing individuals with the needed fresh start and offering viable but financially troubled firms the opportunity to restructure.

That being said, stakeholders have been clear in expressing the need for the BIA and CCAA to be reviewed and updated periodically due to the evolving insolvency environment. As key marketplace framework legislation, the BIA and CCAA play an important role in Canada's economic performance. They also affect the lives and livelihoods of hundreds of thousands of Canadians every year. It is imperative that legislation of this significance is reviewed and updated to ensure it continues to meet its objectives.

This report and the review that supported it is one important step towards that goal. A parliamentary committee review and report stage will occur next. During this time, Industry Canada will continue to reach out to stakeholders, including academics and insolvency experts, and conduct further study and analysis. Decisions regarding any potential reforms will be made following the parliamentary committee report stage.

Annex A — Stakeholder Submissions

- Air Canada Pionairs

- American Frozen Food Institute, Virginia

- Anne Clark-Stewart

- Assuris, Ontario

- Barb Sabathil

- Benoit Mario Papillon, Université du Québec Trois-Rivières

- BC Produce Marketing Association

- Bruce Leonard, Esq., Ontario

- Canadian Association of Insolvency and Restructuring Professionals

- Canadian Bankers Association

- The Canadian Bar Association

- Canadian Bond Investors Association

- Canadian Federation of Agriculture

- Canadian Federation of Independent Business

- Canadian Federation of Pensioners

- Canadian Institute of Actuaries

- Canadian Life and Health Insurance Association Inc.

- Carol Martin

- Cavendish Farms, New Brunswick

- Consumers Council of Canada

- Credit Union Central of Canada

- Dennis A. Fege

- Doug Querns

- EarthFresh Foods, Ontario

- Edward Song

- Fresh Produce Alliance, Ontario

- Fresh Produce Association of the Americas, Arizona

- Frozen Potato Products Institute, Virginia

- Gail Clark

- Government of Alberta

- Healthy Trends Produce LLC, Arizona

- Holland Marsh Growers' Association, Ontario

- Hoyes Michalos and Associates Inc., Ontario

- Hugh C. Stewart

- Iain Ramsay, Kent Law School, United Kingdom

- Insolvency Institute of Canada

- Insurance Corporation of British Columbia

- International Insolvency Institute

- International Swaps and Derivatives Association, Inc., New York

- IPR Fresh, Arizona

- James Callon (former Superintendent of Bankruptcy), Ontario

- Jean-Daniel Breton, CPA, CA, FCIRP, Québec

- Jerry Hockin

- Kaliroy Premium Greenhouse Tomatoes, Arizona

- Ken Rowan & Associates Inc., Ontario

- L&M Companies, Inc., Ontario

- Laurie Gescheke

- Leo Wynberg, CA, CIRP

- Marion Evans

- Melinda Long

- Nishaben Patel

- The Ontario Produce Marketing Association

- The Oppenheimer Group, British Columbia

- Paddon & Yorke Inc., Ontario

- Planned Lifetime Advocacy Network, British Columbia

- Prince Edward Island Potato Board

- Roderick J. Wood, University of Saskatchewan and F.R. (Dick) Matthews, Q.C., University of Alberta

- Rumanek & Company Ltd.

- Sam Babe, J.D., M.B.A., Ontario

- Sandia Distributors Inc., Arizona

- SCRG, a Sears Canada retirees association, Ontario

- Sheila Maxwell

- TMX Group Limited

- Unifor, Ontario

- United States Department of Agriculture

- United States Fresh Fruit and Vegetable Trade Associations

- WaudWare Incorporated, Ontario