Table of contents

The development of the CSR Guide benefited from input from an Expert Advisory Group (see Annex 3); however, the Guide neither represents a consensus of the Advisory group nor the views of individual members and the organizations to which they belong. The businesses mentioned in the Guide are not endorsed by the Government of Canada or by the Expert Advisory Group.

Questions, comments and suggestions concerning the Guide should be sent to:

CSR Manager

Industry Canada,

235 Queen Street

Ottawa ON K1A 0H5

PDF version

- Part 1—Introduction

- Part 2—Building a CSR plan of action

- Part 3—Key CSR issues

- Annex 1—CSR standards, guidelines and initiatives

- Annex 2—Additional tools and resources

- Annex 3—CSR expert advisory group

Part 1 – Introduction

1.1 About the Guide

The CSR Implementation Guide for Canadian BusinessFootnote 1 provides practical advice to companies on corporate social responsibility (CSR). It contains information on: how to build a business case for carrying out CSR initiatives; how to develop and implement a CSR strategy; and how to measure and communicate the outcomes.

1.1.1 Intended audience

The Guide is intended for Canadian businesses interested in integrating CSR principles and practices into their operations. It will be of use to:

- Businesses of various size across all different sectors and industries;

- Businesses that are new to or are already engaged in CSR initiatives;

- Businesses with international operations; and

- Business leaders and employees with responsibility for CSR, including senior management, board members and "front-line" employees.

1.1.2 Structure

The Guide has three parts:

- Part 1 provides an overview of CSR, including sections on defining CSR, on the current context that is shaping the discourse, and on the business case for adopting CSR initiatives;

- Part 2 sets out a CSR implementation framework; and

- Part 3 outlines 4 key topics related to building and executing a CSR strategy:

- Stakeholder engagement, risk management, CSR reporting, and CSR and the law.

The Guide is intended to be suggestive, not prescriptive. As such, throughout the Guide, text boxes are used to illustrate 'real-world' case studies and examples, and to provide "quick glimpse" summaries of selected topics. The aim of this information is to provide the reader with applicable context and insights, and to assist companies in identifying an approach to CSR that best fits their context.

In addition, three annexes accompany this Guide:

- Annex 1 contains supplementary information on key international CSR standards, guidelines and initiatives that are endorsed by the Government of Canada;

- Annex 2 provides a list of additional tools and resources to help implement a CSR strategy; and,

- Annex 3 lists the members of the CSR Expert Advisory Group that provided input into the development of the Guide.

|

|

Reality Check |

|

|

Examples of CSR initiatives |

|

|

CSR and small business |

|

|

Guidance and links for producing a CSR report |

Introduction

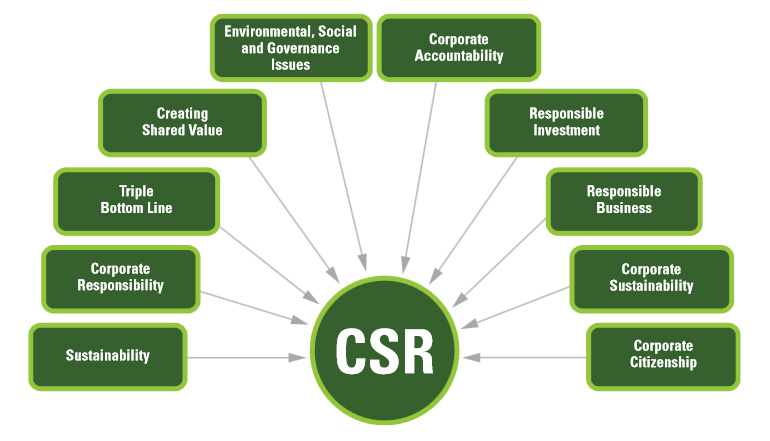

1.2 CSR Defined

The Government of Canada CSR strategy entitled Doing Business the Canadian Way: A Strategy to Advance CSR in Canada's Extractive Sector Abroad, defines CSR as the "(…) voluntary activities undertaken by a company to operate in an economically, socially and environmentally sustainable manner." There is, however, not one universally accepted definition of CSR, and as such other notable definitions do exist.

The International Organization for Standardization (ISO) uses the term ‘social responsibility' to define CSR as "The responsibility of an organization for the impacts of its decisions and activities on society and the environment, through transparent and ethical behaviour that:

- contributes to sustainable development, including the health and welfare of society;

- takes into account the expectations of stakeholders;

- is in compliance with applicable law and consistent with international norms of behaviour; and

- is integrated throughout the organization and practiced in its relationships."

The Organisation for Economic Cooperation and Development (OECD) defines ‘responsible business conduct' in its Guidelines for Multinational Enterprises as "The positive contributions that multinational enterprises can make to economic, environmental and social progress, and to minimize the difficulties to which their operations may give rise."

As is evidenced by these three definitions, there are many different terms for what is considered CSR:

Irrespective of how CSR is labelled, what is most important is integrating social, environmental and economic considerations into a business' core values, culture, decision-making, strategy and operations. This should be carried out in a transparent and accountable manner, with the overall objective being more effective and efficient business practices, increased wealth creation and improved societal outcomes.

1.2.1 Aspects of CSR

Beyond complying with laws and regulations related to CSR topics, voluntary CSR initiatives typically pertain to one or more of the following topics:

- Corporate governance

- Community involvement, development and investment

- Anti-bribery and corruption policies

- Corporate philanthropy and employee volunteering

- Employee health and safety

- Involvement and respect for Aboriginal peoples

- Accountability and transparency

- Community health and safety

- Environmental stewardship

- Corporate ethics

- Supplier relations, and sourcing practices

- Technology development and research

- Human rights

- Customer satisfaction

- Consumer safety

- Employee engagement and well-being

- Labour rights

- Adherence to principles of fair competition

- Performance measurement and reporting

- Empolyee development

Many of the subjects above intersect with Canada's regulatory and legal framework; Section 3.3 of the Guide provides more information on the relationship between CSR topics and relevant laws.

Reality Check

"We already obey all the laws so why do we need to do more than that?"

Compliance with the law is the minimum expectation for companies. Complying with the law, however, does not ensure that a company is profitable or competitive, that it attracts the best employees or that it gains the support of communities. CSR has the potential to provide significant business benefits, including differentiating your innovative products and services from your competitors; reducing costs and risks; helping attract and retain employees; meeting customer and partners' needs; and building strong relationships with communities.

Introduction

1.3 Current Context for CSR

This section aims to provide background information that explains why considering CSR has become integral to business success.

1.3.1 Why is CSR important?

The activities of the private sector can have a significant impact on the environment, on communities and on the economy. Effectively recognizing and managing these environmental, social and economic costs, as well as the impacts, opportunities and risks they present is an indicator of a well-managed company.

United Nations (UN) Principles for Responsible Investment

In 2006, the UN launched the Principles for Responsible Investment (PRI). The UN PRI provides a practical framework for investors to recognize environmental, social and governance factors in investment decision-making and ownership. As of 2012, more than 1,000 investors, managing more than $30 trillion in assets—approximately 20% of the world's capital—have signed on to the United Nations PRI.

Companies that derive the most value from CSR have moved beyond considering it an "add-on" or a separate function. They embed CSR initiatives into their everyday business, strategically integrating and aligning them into their core functions. Michael Porter, a professor at Harvard University and a leading expert on the value of integrating CSR into business operations, calls this approach "creating shared value."

Creating shared value

The "creating shared value" concept encourages companies to think about creating societal benefit as a powerful way to create economic value for the firm. Using a business value proposition to address societal needs can involve redesigning a product, reconfiguring the value chain, and engaging with supporting industries and business partners towards a social goal.Footnote 2

Environmental sustainability

Despite progress in minimizing the environmental impacts of the private sector, the costs of unsustainable business practices on the environment are significant. A 2011 study by Trucost, commissioned by the United Nations Environment Program, estimated that the annual environmental cost from global human activity was 11% of the world's GDP in 2008, and that the world's 3,000 largest publicly-listed companies were responsible for $2.15 trillion US, of environmental damage.Footnote 3 CSR initiatives, such as recognizing and managing the environmental, social and economic costs of production, are therefore a fundamental part of the response of the private sector to adapt business practices and to address unsustainable uses of the environment.

Economic sustainability

Economic activity is central to all companies—generating wealth for shareholders and employees. Responsibly managing the broader economic impacts of business, such as monitoring the labour conditions of key suppliers, is an important element of CSR, and is also an opportunity to ensure a company's long term competitiveness and profitability.

Social sustainability

Businesses are an integral part of the communities where they operate. Their success and "license to operate" are based on continued good relations with a wide range of individuals, groups and institutions. Companies are increasingly well positioned to confront a wide range of social issues, and are recognizing that actions in this area are increasingly scrutinized and publicized by consumers and the media. From employee well-being and local community development to major global issues, such as gender inequality, poverty, the spread of chronic diseases, human rights abuses and high child mortality rates, addressing these topics is in the long term self-interest of business.

A final point in this section addresses the emerging trend of companies to both collaborate and compete in the CSR sphere. This means that companies are collaborating on CSR efforts when that is more efficient, while continuing to compete on their signature CSR initiatives. For example, companies may cooperate by working together with a voluntary labour standard scheme to ensure industry-friendly outcomes, while the same companies compete in other CSR areas, such as on supply chain sustainability initiatives.

Small and medium enterprises (SMEs) have characteristics that enable CSR efforts

- SMEs are flexible and adaptable—they are able to quickly act on new opportunities as they arise and to take advantage of new niche markets.

- SMEs are creative and innovative—they constantly look for efficiencies through creative thinking and innovation, and often champion new ideas in the marketplace.

- SMEs are less bureaucratic—this makes it easier to get the CSR message across and to get your whole company involved.Footnote 4

Introduction

1.4 Business Case for CSR

Formulating a business case for CSR can differ from one company to another since it depends on many factors, such as:

- company size;

- industry or sector;

- products and services;

- position in a supply chain;

- location;

- customers;

- suppliers;

- stakeholders and partners;

- corporate leadership; and

- reputation.

Nevertheless, there is growing consensus regarding the connection between CSR and business success. A 2013 study by the MIT Sloan Management Review and the Boston Consulting Group found that more than 60% of companies that have embedded sustainability into their management agenda have reported increased profits from sustainability initiatives.

Additionally, a study of 275 global Fortune 1000 companies found that the top 50 most sustainable companies outperform the bottom 50 by 38% when it comes to shareholder returns over a five-year period. Despite the fact that it is not possible to know whether this is a direct ‘cause' and ‘effect' relationship, the study still provides compelling motivation to invest in sustainability. In fact, 93% of CEOs recognize that sustainability initiatives are important to their company's future success.Footnote 5

At a more operational level, the following describes some of the key potential business benefits of adopting CSR initiatives.

| Competitive Advantage |

The integration of CSR initiatives across a company can lead to the development of innovative processes, technologies, products or services; addressing sustainability issues through these channels can:

|

|---|---|

| New business opportunities |

Markets for environmentally sustainable and ethical products are expanding, leading to new market opportunities; applying CSR initiatives will help your company to compete on either the supply or demand side of any new opportunity, and to ensure that your existing markets remain viable for the long term. |

| Access to finance |

Financial institutions and institutional investors are increasingly incorporating social and environmental criteria into their assessment of investments and lending. Companies that can demonstrate a strong CSR performance may have preferential access to investment funds or to financing, or may receive preferential terms. |

| Improve efficiency |

Carrying out CSR initiatives related to, for example, energy, water, transportation, packaging, manufacturing processes and waste can often reveal opportunities for efficiencies and cost reductions. |

| Enhance ability to recruit, develop and retain staff |

Employees want to work for companies that reflect their values on the environment and society. Companies that implement a CSR strategy can realize improvements to staff recruitment, engagement and retention. |

| Improve stakeholder and community relations |

CSR initiatives can support companies in building strong relationships with governments, key stakeholders and communities. These relationships can help a company to build and to maintain a "social license to operate" and can evolve into public, private and civil society alliances. |

| Manage risks |

Use CSR initiatives to better anticipate and manage risks related to: Access to resources

Operations

Financial and legal exposure

Reputation

|

Given the benefits listed, the following two boxes demonstrate how companies are benefiting from CSR initiatives.

Companies benefit from implementing CSR

- Vancity, a Vancouver-based credit union, installed programmable thermostats and automatic lighting systems and as a result cut electricity use by 20%.

- In 2012, TD CanadaTrust implemented a video-conferencing pilot program which saved over 800,000 km of travel and 48 tonnes of CO2.

- In 2009, Canadian grocer and retailer Loblaw made a commitment that by 2013 it would only sell fish from certified sustainable sources. Overall, the initiative has resulted in deepening and more stable supply chain relationships.

"(…) a study looked at 230 workplaces with more than 100,000 employees and found that the more a company actively pursues worthy environmental and social efforts, the more engaged its employees are. The Society for Human Resources Management compared companies that have strong sustainability programs with companies that have poor ones and found that in the former morale was 55% better, business processes were 43% more efficient, public image was 43% stronger, and employee loyalty was 38% better. Add to all that the fact that companies with highly engaged employees have three times the operating margin and four times the earnings per share of companies with low engagement, and you've got a compelling business case for this trend to continue (…)."Footnote 6

The business case for implementing CSR initiatives expands beyond optimizing business operations and ensuring long-term viability to the need to align a business with the values of its customer/client base. The following four text boxes demonstrate the growing importance of maintaining a strong corporate reputation in the eyes of customers/clients.

CSR and reputation

The Reputation Institute's 2011 "Pulse Survey" indicated that CSR is responsible for more than 40% of a company's reputation.Footnote 7

Canadians are talking about CSR

A majority of Canadians (60%) talk with friends and family about topics related to social responsibility: 42% say they talk with friends and family about a company's ethical behaviour and 33% say they have recommended a company because they believed it was socially responsible.Footnote 8

Canadians consider themselves to be ethical consumers

- More than half of Canadians (58%) consider themselves to be ethical consumers.

- Three in ten respondents (29%) said they would spend an additional $15 or more on a $100 item if they were sure it was ethically made.Footnote 9

Ethical consumers

According to a 2012 survey by the Responsible Consumption Observatory, nearly three-quarters (73.8%) of Ontarians believe that to consume responsibly is to buy eco-friendly goods and services. In 2012, nearly half (46.4%) of Ontario consumers surveyed had increased their consumption of green goods and services, and 53% had occasionally switched brands due to environmental convictions.Footnote 10

"Aspirational" consumers

Through a global study on consumer values, motivations and behaviours, BBMG, GlobeScan and SustainAbility found that 37% of consumers surveyed could be categorized as "aspirational" consumers. "Aspirational (consumers) represent the persuadable mainstream on the path to more sustainable behaviour. They love to shop, are influenced by brands, yet aspire to be sustainable in their purchases and actions." This consumer segment represents a significant opportunity for forward-looking brands to unite consumerism with social and environmental values."Footnote 11

"Aspirational" consumers represent hundreds of millions of consumers globally, and the largest consumer segment in Brazil, China and India. They are also among the most likely to believe in the need to "(…) consume a lot less to improve the environment for future generations" (73%), and to feel "(…) a sense of responsibility to society" (73%).

-Raphael Bemporad, Co-Founder of BBMG

Despite the strong business case for implementing a CSR strategy, some companies face challenges in doing so. The table below presents some examples of common obstacles to implementing CSR and strategies to overcome them. Many companies also anticipate significant obstacles; the table below presents a series of perceived obstacles and how a company may overcome them.

| Lack of resources |

|

|---|---|

| Too costly |

|

| Lack of expertise |

|

| Stakeholders are not demanding action |

|

| Lack of upper management support |

|

The next section of the Guide presents a CSR implementation framework, with a focus on how to develop and implement CSR initiatives.

Part 2—Building a CSR Plan of Action

2.1 CSR implementation framework

This part of the Guide follows a "plan, do, check and improve" framework that supports continuous improvement. The framework is intended to be flexible; you are encouraged to adapt it and to select the aspects and actions that are most relevant and that have the greatest impact potential.

The five key tasks to building a CSR plan of action are shown in the figure below, and the following table demonstrates the process for executing each task. The next five sections of the Guide go into greater detail on each of these tasks.

| Phase | Task | Process |

|---|---|---|

|

||

| Plan | 1. Assess the existing CSR situation |

How to do a CSR assessment:

|

| 2. Develop a CSR strategy and initiatives |

How to develop a CSR strategy and initiatives:

|

|

| Do | 3. Implement the CSR strategy and initiatives |

How to implement a CSR strategy:

|

| Check | 4. Communicate about the CSR strategy and initiatives |

How to communicate a CSR strategy and initiatives:

|

| Improve | 5. Evaluate and scale-up the CSR strategy and initiatives |

How to evaluate a CSR strategy and initiatives

|

Part 2—Building a CSR Plan of Action

2.2 Task 1: Assess CSR Awareness and Action

In this section you will learn:

- What a CSR assessment is and why it is important

- How to do a CSR assessment

2.2.1 What is a CSR assessment and why do it?

Carrying out a CSR assessment can help a company to identify its potential CSR-related gaps, opportunities, risks, challenges and problems, and can culminate in an understanding of where a company is strong and where it is weak relative to internal CSR goals, competitor initiatives and best practices.

A CSR assessment can provide an understanding of the following:

- the internal and external drivers motivating a company to undertake a systematic approach to CSR;

- the existing internal interest and buy-in;

- the key CSR issues that are affecting or that could affect a company;

- an inventory of existing CSR-related initiatives;

- key stakeholders who are, or who need to be, engaged;

- the current corporate decision-making structure and its strengths and inadequacies in terms of implementing a more integrated CSR approach; and

- the human resource and budgetary implications of a chosen CSR approach.

2.2.2 How to do an assessment

A five-stage CSR assessment process is set out below:

- Assemble a CSR team

- Develop a working definition of CSR

- Articulate a business case for CSR

- Review corporate documents, processes and operations

- Identify and engage with key stakeholders

Of course, this is not the only way to do an assessment; rather it is one way for a company to review, through a CSR lens, the full range of its operations. The bottom line is such that as long as a thorough appraisal is carried out, then it will have achieved the objective of the assessment.

Quick tip for SMEs

- Consider using one of the many existing self-assessment tools, such as the Corporate Responsibility Assessment Tool, published by the Conference Board of Canada; see Annex 2 for additional tools.

- Ask an industry association or CSR specialist organization whether it offers assistance with self-assessment.

I. Assemble a CSR Team

Who are a company's CSR champions?

After confirming the need for a CSR team, frank discussion should take place at the outset about the team's objectives, members' responsibilities, and anticipated workload and outcomes. Regular two-way communication between a CSR team and the company as a whole may also be useful. The following table provides guidance for selecting a CSR team.

|

Representatives of the board, top management or owners It is critically important that a CSR team be directly accountable to senior management, and ultimately to the board (if applicable). This acknowledges that effectively implementing CSR initiatives requires integration into a company's central values and operations. Having a senior manager on the team also sends a clear signal that a company considers CSR to be important. Additionally, senior management and executives have access to:

|

|

Management-level representation from all of the business units Ensuring each business unit is represented from the beginning means an efficient integration of CSR practices and processes into all operations, processes, and decision-making. |

|

Front-line staff Front-line staff are often most familiar with a company's day-to-day business and interactions with customers, business partners and stakeholders. Front-line staff are also likely to have critical insights into CSR obstacles and opportunities. |

Include diversity on a CSR team

Once you have an idea of who should be represented on your CSR team, consider choosing individuals that represent diversity in terms of age, gender, ethnicity, and seniority—a variety of perspectives will contribute to a more robust and effective CSR strategy.

II. Develop a working definition of CSR

Does everyone in a company think of the same thing?

A chosen CSR definition will become the foundation for the rest of the assessment and provides the opportunity to identify what CSR means for a company. The definition should be something quite general that reflects a company's values, and that resonates with its business priorities.

Below are selected company examples of what a working definition of CSR could look like.

|

|

|

|

III. Articulate a company's business case for CSR

Why we do this?

After having developed a definition of CSR, the next step is to draft a business case. Of most importance, a business case must include how a company will benefit and derive value from implementing any CSR initiatives. As such, consider the following questions to Guide this exercise:

Questions to ask as you build your company's business case

- What are a company's short-and long-term goals?

- What benefits would a company like to realize from implementing CSR initiatives?

- In which areas of a business could particularly large CSR gains be made?

- In which areas can a company potentially gain a competitive advantage?

- Are there any risks or threats that a company faces that could be dealt with through CSR initiatives?

- Where are a company's opportunities for cost reductions?

- Who initiated an interest in CSR?

- What were the circumstances?

- What do board members, senior executives, and owners have to say?

- In which areas of a business do key stakeholders have particular influence and/or interest?

- What do its customers or clients think about CSR?

- Do any broader changes led by senior management align with a CSR approach?

- What are competitors doing when it comes to CSR?

- What benefits are they seeing?

- What company data and/or literature can support the case?

IV. Review company operations, documents and processes

What is already in place? Where are the gaps? What can be changed?

With a working CSR definition and a defined business case, the next step is to review company documents, processes and operations for actual and potential CSR implications. In other words, you want to understand where a company's existing policies and documents intersect with any potential CSR topics; many companies are already engaging in CSR initiatives without necessarily identifying them as such.

Key operational and governance documents

What is in place that already supports CSR? Where are the gaps?

Documents to include in a review could include a company's:

- mission and value statements;

- codes of conduct;

- policies (e.g., human resources, health and safety, management systems, procurement/sourcing, ethics, anti-bribery, environmental protection, community engagement, labour, supply chain engagement, security, research and development, executive compensation, etc);

- operating documents or guidelines;

- employee job descriptions, and education and advancement programs;

- consumer engagement strategies;

- risk management analyses; and

- communications products.

In summary, collecting and reviewing this and similar information will provide quick insight into a company's potential CSR focus areas.

Below is a sample framework for conducting a document review.

|

Assessment Criteria |

Document A |

Document B |

Etc. |

|---|---|---|---|

|

Why was this document developed? What was it in response to? |

- | - | - |

|

What aspects of CSR are mentioned in this document? |

- | - | - |

|

Does this document reference any international standards or guidelines relating to CSR? (See Annex 1 for examples of such standards). |

- | - | - |

|

How does this document compare to our competitors'? |

- | - | - |

|

What gaps can be identified in terms of existing and desired CSR initiatives? |

- | - | - |

Decision-making processes

Who makes which decisions and how?

Existing decision-making processes and criteria may have an impact on how a CSR strategy is developed and implemented. Often, a variety of different departments and individuals will already be making daily CSR-related decisions. The table below, therefore, describes common business processes at companies, and suggests questions to map different departments' connections with CSR.

| Business process | Key questions to ask |

|---|---|

|

Customer service and business development |

|

|

Human resources |

|

|

Procurement/sourcing |

|

|

Marketing and media relations |

|

|

Research and development |

|

|

Strategic and business planning |

|

|

Project management |

|

|

Risk management |

|

|

Assurance |

|

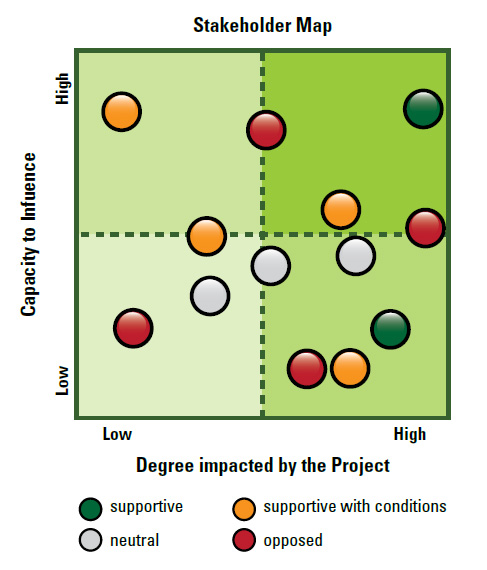

V. Identify key stakeholders

Who are key stakeholders?

Determining the potential interests and concerns of stakeholders can reveal opportunities and potential problem areas related to the development of a CSR strategy.

A useful technique is therefore to carry out a stakeholder mapping exercise. This is a way of identifying the variety of stakeholder relationships that a company has, and of assessing the relative proximity or strength of that relationship. A sample list of potential stakeholder groups and an example of a stakeholder mapping exercise from the International Finance Corporation's Strategic Community Investment Good Practice HandbookFootnote 16 are included below.

Note that while stakeholder mapping is listed here as the last element of a CSR assessment, this exercise could be undertaken concurrently with other steps in this section.

Existing CSR assessment tools

- Conference Board of Canada. Corporate Responsibility Assessment Tool

- See Annex 2 for a list of additional CSR assessment tools and resources.

Note that section 3.1 in the Guide provides detailed guidance and practical tools on how to identify and engage your stakeholders.

Reality Check

"Assembling a CSR team, developing a working definition of CSR with employee/management engagement, reviewing core documents, decision-making processes and CSR-related activities, and mapping stakeholders. Do you know how much time it will take to simply recruit and engage a CSR team that represents all of our business lines and offices throughout Canada and around the world, let alone schedule them into regular meetings to manage CSR activities? You've got to be kidding!"

If done properly, effectively implementing CSR initiatives does indeed take a significant investment of resources at the "front end" of the process. The return on this investment flows from a company being as prepared as possible to address the CSR challenges, opportunities and choices available, and from a company being less vulnerable to unexpected social and environmental-related challenges.

The next step is to turn a CSR assessment into a strategy and initiatives; the next section of the Guide provides details on this next task.

Part 2—Building a CSR Plan of Action

2.3 Task 2: Develop a CSR Strategy and Initiatives

In this section you will learn:

- What a CSR strategy and initiatives are and why they are important

- How to develop a CSR strategy and initiatives

2.3.1 What is a CSR strategy?

How will you organize a CSR strategy? What are the focus areas?

One company may choose to focus its efforts in multiple areas—employee health, environmental impact and supporting local communities through its sourcing practices, while another might focus entirely on environmental initiatives related specifically to one issue, such as water usage.

A CSR strategy is a road map for moving ahead on CSR issues. It sets a company's direction and scope over the long term with regard to CSR initiatives. The ultimate goal is to embed a CSR strategy into a company's strategic objectives, processes and competencies.

An effective CSR strategy identifies the following:

- overall direction and objectives for where a company wishes to go in its CSR work;

- a basic approach for getting there;

- specific focus areas, initiatives and performance indicators; and

- immediate next steps.

CSR and small business

A CSR strategy is most likely to succeed when it:

- is aligned with a company's values and core business;

- is supported and championed by senior management;

- makes use of input and ideas from a company's employees; and,

- approaches issues systematically, building on strengths and addressing weaknesses.

Quick tips for SMEs

- Determine priorities before developing a strategy; priorities will Guide the overall strategy.

- Set aside time to identify links between the actions in the strategy and the business case for CSR.

- Join an association with a CSR focus; there are a number of associations that offer assistance with developing a CSR strategy or that can make a referral.

2.3.2 How to develop a CSR strategy

The following six steps describe a typical approach to developing a CSR strategy:

- Research what competitors are doing

- Develop CSR initiatives

- Build support with senior management and employees

- Set performance measurements

- Hold discussions with major stakeholders

- Review and publish strategy and initiatives

Each step is described in more detail below.

I. Research what competitors are doing

Examining the vision, values and policy statements of leading competitors, along with their codes, new CSR-related product lines or approaches, and any initiatives or programs in which they participate, can provide example models and can inform competitive positioning. Assessing the benefits, costs, immediate outcomes, resource implications and changes to current practices necessary to adopt similar approaches may also provide helpful information. When reviewing the CSR initiatives of others, consider the following questions:

How to assess what your competitors are doing

- What people and organizations were involved in developing these initiatives?

- Would these groups be the same people and organizations that would need to be involved in a company's own CSR initiatives?

- What are the objectives underlying the development of these CSR initiatives? Are those objectives the same or different from those underlying a company's CSR objectives?

- Can a particular CSR issue identified by a company be resolved or addressed through the use of these or similar CSR initiatives?

- What are the potential costs, drawbacks and benefits of the various types of initiatives?

- What approach, standard or initiative is a company already associated with, eg., issue or industry specific codes, corporate standards or certifications, including voluntary standards, and/or international initiatives.

- What is the applicability or suitability of these initiatives to a company in light of its scope of activities and the geographic range of its operations?

- Will a company benefit from the initiatives and, if so, how?

II. Develop CSR initiatives

What should be done? What will be done? How will these actions benefit a company?

Drawing on the work from a preparatory CSR assessment exercise, especially the information collected to formulate a business case, and from an analysis of competitors' strategies, the next step is to begin to draft a complete strategy, including objectives, focus areas and actual initiatives.

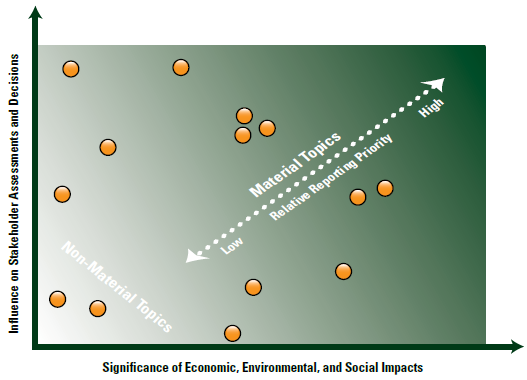

CSR objectives should reflect the CSR issues that matter most to a company. Carrying out a risk or materiality assessment provides a structured basis for the identification and prioritization of CSR issues. More information on this important step is provided in Section 3.2 of the Guide.

CSR initiatives are statements that indicate what a company intends to do to address its social and environmental impacts, to maximize benefits and to manage risks. CSR initiatives should be clear and concise plain language statements.

When choosing among possible CSR initiatives, there are many considerations to take into account, including:

- the size of the risk or opportunity;

- the extent to which the risk or opportunity can impact a business;

- the estimated effectiveness of possible actions;

- the ease of implementation;

- the financial and human resources needed to implement the changes;

- legal and customer requirements; and

- the speed with which decisions can be implemented.

Additionally, consider the following when developing initiatives:

Initiatives might:

- set minimum standards for a company; or

- define performance standards that a company aspires to meet, such as complying with a voluntary standard and certification scheme.

Initiatives will normally include reference to:

- the scope of CSR topics to which they apply;

- specific actions to be carried out;

- the expected outcome; and

- any external framework or standard that your company will apply.

Initiatives may also include:

- a timeline for implementation or delivery;

- management actions to be taken;

- types of data to be collected;

- the indicators that will be used for evaluation and reporting; and

- collaborations or partnerships to pursue.

The end goal of this exercise is to develop and to prioritize CSR initiatives based on their alignment with a company's business strategy, ease of implementation and anticipated pay-offs.

Voluntary Labelling Standards

Codes and standards are often linked to third-party verification or certification labelling programs. Careful examination of the codes' terms at the outset—to make sure they are compatible with your company's mission and culture—can reduce the likelihood of not meeting the initiative's objective; there may also be investments required for companies to "get up to code."

The following are examples of CSR initiatives developed by various companies—the first set includes broad and high-level statements that demonstrate in which areas the company will focus its CSR initiatives and the second set of examples illustrate specific actions that the company will carry out.

Bridgehead Coffee's vision, mission and values

Vision: We link our customers with small-scale farmers in the developing world through sustainable fair trade.

Mission: We demonstrate that business can be socially responsible and profitable. We strive to provide the highest quality products and service for our customers, while honouring these core values:

Values:

- We maintain fair trade as the founding principle of our business.

- We encourage community building locally and globally.

- We create premium products for our customers.

- We use organic and locally produced products wherever possible.

- We consciously reduce our environmental impact.

- We encourage a healthy, open and inclusive work environment.

- We provide ongoing education and growth for employees and customers.

Teck's vision statement

As part of the corporate sustainability strategy, Teck has developed vision statements relating to each of their key sustainability issues. Below are two examples:

Water: contribute to the ability of present and future generations to enjoy a balance between the social, economic, recreational and cultural benefits of water resources, within ecologically sustainable limits.

Community: collaborate with communities so they genuinely benefit in a self-defined and sustainable manner from our activities and products. Communities consider themselves better off as a result of their interactions with us and offer broad support for our efforts.

The Co-operators Group Limited vision, mission and values

Vision: The Co-operators aspires to be valued by Canadians as:

- A champion of their prosperity and peace of mind.

- A leader in the financial services industry, distinct in its co-operative character.

- A catalyst for a sustainable society.

Mission: Financial security for Canadians and their communities.

Statement of values

At The Co-operators we:

- Strive for the highest level of integrity.

- Foster open and transparent communication.

- Give life to co-operative principles and values.

- Carefully temper our economic goals with consideration for the environment and the well-being of society at large.

- Anticipate and surpass client expectations through innovative solutions supported by mutually beneficial partnerships.

Co-operative principles include:

- voluntary and open membership;

- democratic member control;

- member economic participation;

- autonomy and independence;

- education, training and information;

- co-operation among co-operatives; and

- concern for the community financial.

Subsequently, the following companies demonstrate examples of specific initiatives, which can usually be measured using quantitative or qualitative methods.

Examples of specific company initiatives

Mountain Equipment Co-op (MEC) initiatives related to product design and community investment:

- Increase the volume of bluesign® approved MEC-brand apparel materials to 50% of all apparel materials purchased.

- Maintain 1% of annual gross sales to support the outdoor community and maintain MEC's commitment to "1% For The Planet."

- Divert at least 92% of waste from landfill.

- Reduce total GHG emissions by 20% from 2007 levels.Footnote 17

TD initiatives for employee engagement

- Show continuous improvement in employee engagement score (calculated using an Employee Engagement Index based on the average response to 3 questions on 'feelings of accomplishment,' 'pride in TD,' and 'plans to be with TD in one year.'

- Provide diversity and inclusion training for all employees in North America.Footnote 18

Loblaw's initiatives for food safety and quality

- Obtain 100% of seafood from sustainable sources by the end of 2013. Achieve 100% Global Food Safety Initiative (GFSI) certification for control brand vendors.

- Convert all control brands to meet the federal government's recommended maximum sodium requirements by 2016.Footnote 19

Blackberry initiatives for supplier auditing

- Audit 50 suppliers against the Blackberry Supplier Code of Conduct, which is based on the Electronics Industry Citizenship Coalition Code of Conduct, comprised of topics related to labour, ethics, environment, and health and safety.Footnote 20

Ford initiatives for product design

- Expand the use of the Product Sustainability Index (PSI) and Design for Sustainability principles in product development.

- Reduce global facility CO2 emissions per vehicle by 30% by 2025 compared to a 2010 baseline.

- Use at least 25% recycled content in seat fabrics on all new and redesigned vehicles sold in North America.Footnote 21

Kraft Foods

- Obtain 100% of its raw materials from sustainable sources for its European coffee brands by 2015.Footnote 22

Cascades

- Reduce the discharge of effluent per saleable metric tonne by 6% by 2012.

- Increase the use of recycled fibres and virgin fibres that are Forest Stewardship Council certified (or equivalent) to 86.3% by 2012.

Collaboration in the Supply Chain—The MACH Initiative

The MACH Initiative was launched by the Quebec aerospace cluster, Aéro Montréal, in June 2011. MACH is designed to optimize the performance of Quebec's aerospace supply chain and increase its global competitiveness. Through the initiative, approximately 20 Quebec aerospace suppliers will be provided training, continuous improvement and, among other services, business development support. The suppliers will also benefit from the expertise and guidance of eight world-class Original Equipment Manufacturers (OEMs) and systems suppliers.

MACH aims to strengthen Quebec's supply chain structure and the companies involved in it by facilitating collaboration between customers and suppliers, and by promoting the implementation of strategies and projects to close existing integration gaps in the Quebec aerospace supply chain. Key elements of the Initiative focus on creating joint environmental programs related to water use and to transportation, and enhancing community benefits related to international development and childhood education.

Developing a supply chain policy

Supply chain management can be a key component of your CSR strategy. Your supply chain can be the source of many risks as well as opportunities. In order to manage these effectively, consider using the following tips to create a supply chain policy:

- have a clear purpose or statement of intent;

- clearly set out the minimum expected standards, for example, related to the working conditions of your partners;

- reference internationally recognized human rights instruments such as the Universal Declaration on Human Rights and core International Labour Organization (ILO) conventions;

- have accompanying guidance notes so that those responsible for sourcing can give meaningful guidance to suppliers;

- consider putting CSR information and commitments into contracts;

- detail how the supply chain will be managed and monitored, and how performance on issues such as labour rights or economic standards will feed into appraisals and the renewal of contracts.Footnote 23

III. Build support with senior management and employees

Are all of a company's leaders supportive of adopting a CSR strategy? What do the employees think?

Without the backing of a company's leadership, a CSR strategy and initiatives have little chance of success. A CSR team should therefore report to senior management about the findings of the assessment and should seek support for moving ahead on the proposed strategy and initiatives. It is equally important to continue to build support among employees, given the key role they will ultimately play in implementing CSR initiatives.

Board level buy-in at Sprint

Sprint has made sustainability a board-level agenda item. Sustainability is part of the company's formal board review process, its annual review, and at nomination and governance committee meetings. Board members go over the company's sustainability performance and consider the company's progress against its goals.Footnote 24

IV. Set performance indicators

How can progress and achievements be monitored?

After having finalized CSR initiatives, the next step is to set performance indicators that are aligned to the initiatives. These indicators allow a company to measure whether it is executing its CSR initiatives, and can be used to inform adjustments in approach or resources be necessary. When developing CSR indicators, it is best practice to follow the SMART guidelines:Footnote 25

The following boxes provide various examples of performance indicators:

|

Initiative |

Reduce the amount of waste sent to the landfill |

|---|---|

|

Key performance indicator |

Reduce solid waste by 25 percent by the end of the year |

|

Measurement method |

The kilograms of garbage produced each month, which are recorded and monitored |

|

Initiative |

To improve relations with the community, double the number of town hall meetings a company holds and reduce the number of complaints by half |

|---|---|

|

Key performance indicator |

The number of town hall meetings and the number of complaints at the end of the year |

|

Measurement method |

Quarterly tallying of meetings and complaints which are recorded and monitored |

|

Initiative |

Do not offer improper payments to officials since all employees are aware of the company's requirements and legal obligations |

|---|---|

|

Key performance indicator |

Training course developed and implemented as part of employee induction training, and regular updates are provided for all staff |

|

Measurement method |

Whether training program is implemented and the number of staff trained as a percentage of total staff |

In all three cases, a regular review of the initiative's objectives against the indicator might lead a company to modify the indicator, as it is not capturing the objective. For instance, in the second example above, a company might conclude that increasing the number of town hall meetings did not improve community relations, since underlying problems were not also addressed. As a result, a better objective might be increasing the number of resolved complaints. It is also important to revisit and to re-evaluate targets over time as performance and operating priorities change.

Reality Check

Now that we've set some initiatives with performance indicators, what happens if we don't reach them?

Presenting a balanced description of a company's performance, both positive and negative, is an important way to build trust with stakeholders. Describing the key actions, programs or changes that a company has put in place to address the problem of not meeting an initiative is a good way to communicate about a company's approach to sustainability. In the end, balanced reporting is integral to maintaining trust and to ensuring reputational benefit.

V. Hold discussions with major stakeholders

Once CSR initiatives that are supported by management have been drafted, it is likely that they'll generate interest from external stakeholders. Consider, therefore, engaging with the following stakeholder groups:

|

Business partners, customers, supply chain partners and contractors |

When initiatives apply to these parties, their involvement and agreement to comply with the terms of any initiative is critical. Try to understand their perspective by asking:

|

|---|---|

|

Broader stakeholders |

Reaching out to consumers, shareholders, labour and environmental organizations, community groups and/or governments can help a business to understand these groups' interests and concerns, and could build support for a company's CSR initiatives. Try to understand these groups' perspectives by asking:

|

VI. Review and publish a strategy and initiatives

Once final initiatives and performance indicators have been drafted a final review should be carried out, with a focus on the following key themes:

- the adequacy of the initiatives to manage the CSR issues important to ad business and to its stakeholders;

- whether the initiatives will likely lead to the desired outcome;

- the links between the initiatives and the business case; and

- the feasibility of implementing the chosen initiatives.

Ultimately, final focus areas, initiatives and indicators should be reviewed and endorsed by senior management and the board, if applicable. Once the strategy has been finalized, it should be shared with employees, business partners and other stakeholders. Making initiatives public is critical to building trust in a company's CSR strategy and in mobilizing the support needed for implementation. Accordingly, the next section provides guidance on how to implement a CSR strategy.

CSR and small business

"Our organization is very small and we don't have many strategies other than growing our business. This process seems too complicated for us."

Developing a CSR strategy does not have to be complex. Start by picking one area to focus on based on an easily achievable goal. For example, a company could decide to start making a difference by putting in place a recycling program, by providing tele-work opportunities to employees once a week, or by outlining energy-saving tips for around the office. Record the CSR initiatives that have been implemented and build on those successes year after year. A strategy will become apparent from the priorities that emerge and the actions taken.

Reality Check

"I can see the CSR leadership team and even our executive team getting excited about developing a strategy of this nature. What I can't see is our over-extended middle-management group getting excited about it. In fact, I can see them pushing back, challenging its importance and relevance."

That is why it is so important to invest time in developing a business case for CSR. Use the same systems and formats as for justifying a reallocation of funding to a new initiative, engaging the finance team in the process. Demonstrating how a CSR strategy and initiatives support existing business objectives is an integral part of building support at the middle management level.

Part 2—Building a CSR Plan of Action

2.4 Task 3: Implement a CSR Strategy and Initiatives

In this section you will learn:

- What CSR implementation is and why it is important

- How to implement a CSR strategy

2.4.1 What is CSR implementation?

Implementation refers to the day-to-day decisions, processes, practices and actions that ensure that a company carries out its CSR initiatives, thereby delivering on its CSR strategy.

It is through the process of implementation that a company should realize the value of its CSR strategy and initiatives—delivering on efficiencies, generating value, realizing new business opportunities and minimizing risks.

CSR—A really big change management exercise

The speed at which a company implements sustainability initiatives is different for every organization. For all organizations, however, taking real steps towards sustainability requires fundamental changes to the way that:

- leadership thinks about its business objectives;

- employees think about the work that they do and how they do it; and

- processes and procedures drive performance towards economic, environmental and social objectives.

Fundamental change is not easy or quick, but taking steps towards increased sustainability will help an organization to grow its reputation as a corporate citizen; retain and attract talent; reduce operational costs; and better understand how an organization learns, grows, and adapts to changing market conditions and expectations.

2.4.2 How to implement a CSR strategy

Every company is different and will approach CSR implementation in different ways. The steps below demonstrate one way to implement CSR initiatives.

I. Develop an integrated CSR decision-making structure

Given a company's existing mission, size, sector, culture, organization, operations and risk areas—and given its CSR strategy and initiatives—what is the most effective and efficient CSR decision-making structure to put in place?

The following includes considerations to take into account when designing a CSR decision-making structure.

Considerations for implementing a company's CSR strategy

1) Identify people or committees at the top levels of the company who will assume key CSR decision-making and oversight responsibilities.

- Assigning CSR responsibilities to senior management ensures that CSR issues will receive the attention they deserve and forms a strong basis for an effective chain of CSR accountability within the organization—all of which can support a board's corporate governance function.

There are several options for board participation:

- a sitting board member could be tasked with broad responsibility for CSR activities;

- a new member who has specific CSR expertise could be appointed;

- CSR responsibilities could be added to the work of existing board committees;

- a new CSR board committee could be formed; or

- the entire board could be involved in CSR decisions.

2) Ensure it is visible to all employees.

- CSR initiatives help to drive transparency, accountability and performance. Ensuring the CSR decision-making structure and roles are visible to all employees will help to support delivery.

- CSR responsibilities should be built into job descriptions and performance evaluations.

3) Establish accountability throughout your organization.

- Accountability should start with the board and follow through to the executive and senior levels, supported by coordinated cross-functional decision-making and specialized staff expertise.

- A senior official or committee responsible for overall CSR implementation within a company should be identified and given the resources to do the job. Particular departments having CSR responsibilities (e.g., environmental, health and safety, worker relations, supplier relations, community relations, customer relations, investor relations) could report to the senior official or committee.

Further, employee support for CSR implementation can be maintained in a number of ways, for example by:

- identifying and engaging CSR champions;

- incorporating CSR performance indicators into business plans;

- providing regular updates on progress (in meetings or the company newsletter);

- developing incentives (such as rewards for best suggestions);

- removing or reducing disincentives (e.g., competing interests, such as premature deadlines, seeing cost as the only consideration when choosing suppliers, or resource constraints that encourage employees to choose non-CSR options); and

- celebrating CSR achievements, motivating teams, and building enthusiasm and pride.

II. Design and conduct CSR training

What knowledge and skills do employees need to implement CSR initiatives?

Training can be a key enabler for delivering on a CSR strategy and initiatives. Training addresses knowledge, skills and attitudes, and is most effective when the learner has input into the development of the learning process. There are five steps to establishing a successful training program:

- conducting a needs analysis;

- setting learning objectives;

- designing the program (i.e., content, format, logistics, timing, duration);

- implementing the program; and

- evaluating the program against the learning objectives.

Developing CSR training

Implementing a CSR strategy requires employees with skills, expertise and capabilities in a range of disciplines, processes and practices. Training is an important tool to ensure employees have the necessary skills. The skills needed, and the focus of any training, may vary substantially across different organizational roles, from senior managers who have responsibility for engaging with a company's stakeholders, to those with responsibility for implementing a management system, to those who must appropriately manage a company's waste.

Undertaking a training needs assessment can help to target training courses at key skill gaps and needs.

Existing sustainability training resources

III. Establish mechanisms for addressing problematic behaviour

What could go wrong and what can be put in place now to ensure it's handled appropriately?

Early detection of activities that are contrary to CSR principles and initiatives is important to ensure the continuous and smooth implementation of a company's CSR strategy. For this reason, it is important for a company to put in place mechanisms and processes that will allow for the early detection, reporting and resolution of problematic activity.

A company should devise approaches that are sensitive to the vulnerable position of employees that report wrongdoing, or a potential non-compliance with any of the CSR initiatives. In addition to clear and fair guidelines on how to report a breach of CSR initiatives, a company could consider anonymous hotlines, email boxes and ombudspersons.

For more specific guidance on whistle-blowing mechanisms, see the U.K.-based Public Concern at Work website or visit Ethics Practitioner's Association of Canada.

Part 2—Building a CSR Plan of Action

2.5 Task 4: Communicate Performance

In this section you will learn:

- What CSR communication is and why it is important

- How to communicate your CSR activities

79% of Canadians are interested in learning how companies are trying to be socially responsible.Footnote 26

2.5.1 What is CSR communication?

Communicating on CSR initiatives and performance is a critical competency for successful companies. Communicating provides the basis for informed decision-making by interested parties who may wish to purchase a company's products, to invest in a company or to support a company's activities in their community. The goal is to communicate CSR progress in a meaningful way that will attract positive attention to a business and that will engage stakeholders.

Other benefits of CSR communication can include:

- higher levels of customer satisfaction and loyalty;

- improved company, brand and product reputation;

- more motivated and productive employees;

- better relations with the local community and public authorities; and

- improved access to financing.

2.5.2 How to communicate a CSR strategy and initiatives

The steps below describe one way to develop a CSR communications strategy.

I. Establish a target audience and objectives

With whom should communication be established? What impact is desired through communication?

The first step in communicating on CSR is to identify the individuals and groups that a company would like to target regarding its CSR communications. It is then helpful to define communication objectives for each stakeholder group. For example, communications targeted at employees may be designed to strengthen employee engagement and satisfaction. The following table lists possible target audiences for CSR communications.

Common audiences

- Employees

- Customers/consumers

- Local community

- Media

- Consumer associations

- Suppliers

- Business partners

- Investors

- General public

- Trade unions

- Public authorities/regulators

- Local organizations or institutions

- Not-for-profit / non-governmental organizations

- Prospective employees

- Aboriginal communities

II. Choose a message

How to decide what to communicate.

For market facing stakeholders

If a target audience is the market in which a company operates (e.g., customers/consumers, investors, business partners, consumer associations, or suppliers), focus on how you integrate CSR initiatives into business operations, or highlight performance achieved. For example, describe initiatives related to supporting local suppliers, product quality and safety, fair purchasing, reductions in energy and water use, sustainable packaging, certification against a voluntary ethical standard, emissions reductions, environmental manufacturing, working conditions and human rights practices, reduced waste and hazardous waste generation, and/or sustainable sourcing.

For community facing stakeholders

If a target audience is the community where a company operates (e.g., local community, local media, prospective employees, not-for-profit / non-governmental organizations, local organizations or institutions, or public authorities), describe commitments to health and safety conditions, investments in the local economy, such as by working with local enterprises, or how CSR initiatives contribute to a healthy and natural environment, or your support for local groups through donations, sponsorships and volunteering.

For internal stakeholders

If a target audience is a company's workforce (e.g., employees and trade unions), describe CSR initiatives related to job safety, work/life balance, diversity in the workplace, training and professional development, corporate culture, and/or values-driven practices.

III. Decide how to communicate

How to get your message across? What is the most effective medium for communications?

The most effective media and communication channels for CSR communication vary depending on the audience and the objectives of the communication. Options vary from launching an awareness campaign to featuring CSR initiatives in advertising and speeches. Whatever the approach, ensuring that the message and the medium match the intended audience and objectives is critical.

Types of CSR communication approaches

Internal stakeholders

- Employee training and education

- Employee updates

External stakeholders

- Sustainability and integrated reporting, e.g., annual reports

- Advertising, websites, social media

- Information packages, brochures, newsletters and mailing lists

- Point of sale materials and salesperson assistance

- Media and events

The next section explains some of these approaches in more detail.

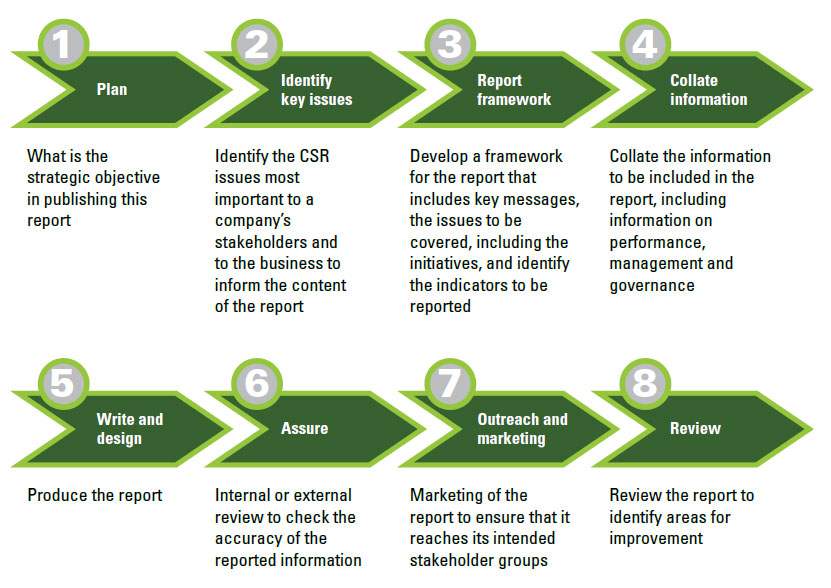

Reporting

A CSR report (also called a sustainability report) enables companies to report sustainability information in a way that is similar to financial reporting. Systematic sustainability reporting gives comparable data with agreed disclosures and metrics. A CSR report provides information about economic, environmental, social and governance performance.

For more detailed guidance regarding CSR and sustainability reporting, and the key steps involved, please see the “Reporting” section in Part 3.

Advertising, websites and social media

Advertisements are an effective way to get consumer attention for a company's CSR initiatives, and may also attract new employees who wish to work for a responsible company. Consider using values-based messaging that reflects consumers' motivations for buying environmentally and socially responsible products and services. Adding CSR information to a company's website ensures that parties can easily access information of interest, and can also be a place to showcase CSR performance information. Consider investing in interactive features to engage and to inform customers.

Engaging current and future clients, employees, and business partners through social media about CSR initiatives and performance is a low cost and effective measure.

Social media tools such as Facebook or Twitter allow a company to connect with thousands of followers instantaneously to share CSR-related material and to receive feedback faster and cheaper than through any other medium.

The following boxes describe how selected companies are using social media as an effective tool to promote and to communicate on their CSR initiatives and performance.

Mountain Equipment Co-operative (MEC)

Mountain Equipment Co-operative (MEC) uses Twitter to connect with almost 30,000 customers and has achieved over 135,000 “likes” on its corporate Facebook account, which has worked to promote the co-operative's various initiatives; MEC's CSR-related postings are available on their Facebook account.

SoftChoice's CSR Blog

For its third Sustainability Report, SoftChoice, a North American information technology company, created a CSR blog to communicate their key initiatives and progress relating to sustainability. "Rather than offering a static, point-in-time snapshot of our efforts, we have created a real-time, interactive blog," says Melissa Alvares, Sustainability Programs Manager at Softchoice. "Our aim is to create a living record of our work that encourages engagement and the sharing of ideas from both within and outside our organization."

A large glossy report will not be effective for all audiences. For example, an on-line snapshot of your performance may provide the information most customers require. Those who want further details can download a more in-depth version.

Information packages, brochures, newsletters and mailing lists

Information packages, brochures, flyers, leaflets, and mailing lists allow audience-specific information to be disseminated strategically. Brochures can be sent to business partners and suppliers, while information packs could go to investors, trade unions and consumer associations. Building a mailing list is an easy way to gain market intelligence on stakeholders, and is a way to provide regular updates on activities.

Point-of-sale information and training salespeople

Providing point-of-sale information on your products and services, for example, by using packaging, signage, or a salesperson, may be the factor that influences someone to choose one company's brand over a competitor's. As such, buyers may be interested in knowing:

- the environmental characteristics of a product and its packaging (e.g., if it is energy efficient, biodegradable, non-toxic, made from recycled materials, organic, etc.);

- who made it and how (e.g., made locally, made abroad with fair trade labour, made with sustainably sourced materials, hand-crafted, etc.); and

- if a proportion of profits go to support community initiatives, charities or not-for-profit organizations.

Media and events

About one-third of Canadians learn how companies behave on social issues through news media.Footnote 27 Getting information on CSR initiatives into newspapers, blogs and radio is an excellent way to raise the profile of a business; press releases and interviews are the most common approaches to engaging the media.

Another way to spread news about your CSR initiatives is by attending issue-related events, and by seeking out speaking and presentation opportunities. If there are no relevant events near a company's location, consider partnering with a local organization to host an event, allowing a company to showcase its achievements and to engage in a broader dialogue with stakeholders.

CSR and small business

"We definitely do not have the resources to hire a professional firm to develop a CSR report. How do we share information about our CSR efforts despite these limitations?"

The easiest route for reporting is to post information on the company website or on social media. This is an inexpensive way to give an update on current CSR initiatives, including both successes and areas for improvement. A small organization can report to its business partners and staff at regularly scheduled meetings. By adding a few sections to basic company literature (brochures, pamphlets), small business owners can communicate CSR activities to their suppliers, customers and community.

The final task in the CSR implementation framework has to do with reviewing and scaling-up a CSR strategy; the next section turns to this topic.

Part 2—Building a CSR Plan of Action

2.6 Task 5: Evaluate and Scale-up

In this section you will learn:

- What is a CSR evaluation and why it is important

- How to review and scale-up a CSR strategy and initiatives

2.6.1 What is a CSR evaluation?

In a CSR evaluation, a company reviews its CSR strategy, initiatives, and performance, and identifies opportunities for improvements and modification. Reviewing and evaluating a CSR approach is about learning and is the fundamental step to ensuring continuous improvement.

An evaluation allows a company to do the following:

- to determine what is working well, why and how to ensure that it continues;

- to investigate what is not working well and why;

- to explore the barriers to success and what can be changed to overcome them; and

- to revisit original objectives and to make new ones, if necessary.

This base of information should allow a company to determine whether the current CSR approach is achieving its objectives and whether the implementation approach and overall strategy are correct. The goal is to understand which areas of a business are improving with respect to CSR, and which areas need further attention, and how to improve them.

CSR and small business

"How is a CSR review different from the self-evaluation that we did a year ago? This seems like an extra piece of work."

Reviewing progress at periodic intervals ensures that a company has an opportunity to identify and to act upon new challenges and opportunities that have arisen. Without regular reviews, there is a danger that a company will repeat problematic practices and will fail to act upon changes in products or processes that could open up new markets. The results of regular evaluations should reveal a company's progress. When the evaluation results have improved, then a company is probably on the right track. When the results have stayed the same or even decreased, then the CSR strategy may need to be revised.

2.6.2 How to do an evaluation

A company could consider the following questions for guidance in preparing its CSR evaluation:

- What worked well? In what areas did a company meet or exceed its targets?

- Why did it work well? Were there factors within or outside a company that helped it to meet its targets?

- What did not work well? In what areas did a company not meet its targets?

- Why were these areas problematic? Were there factors within or outside a company that made the process more difficult or that created obstacles?

- What did a company learn from this experience? What should continue and what should be done differently?

- Drawing on this knowledge and information concerning new trends, what are the CSR priorities for a company in the coming year? Are there new CSR objectives?

The evaluation should involve seeking input from management, a CSR team, employees and external stakeholders.

Reality Check

"I don't get it. What will an evaluation tell us that our $60,000 CSR report doesn't?"

The review stage is critical. It is really about sitting down and understanding what the CSR report is saying. What goals were set but were not actually achieved? Why? Are the reporting indicators the right ones? Are they aligned with a company's mission? Is the company engaging the right stakeholders? Are the right people working on advancing CSR inside a company? This is the stage to reflect on what needs to stay the same and what needs to change; it is critical to the continuous improvement of CSR performance.

2.6.3 Scaling-up a CSR approach

It is also important to think about next steps and about how to scale-up your CSR strategy. The Canadian Business for Social Responsibility (CBSR), which is a non-profit member organization with a mission to accelerate and scale up corporate social and environmental sustainability in Canada, has developed a road map for companies consisting of 19 aspirational and inspirational qualities which can help a company transition to a "transformational" company. The 19 qualities in the road map describe what visionary companies do, how they do it, and with whom they interact. This approach could provide helpful insights for scaling-up an existing CSR strategy. For more information on the transformational company approach, visit the CBSR's website.

Part 3 – Key CSR Issues

3.1 Engaging stakeholders

This section provides additional guidance on the critically important topic of stakeholder engagement.

3.1.1 What is stakeholder engagement?

A stakeholder can be defined as "an individual, or group of individuals, with interests that may affect or be affected by an organization."Footnote 28 Who stakeholders are varies greatly from one company to another and can include suppliers, local community members, employees, investors, non-governmental organizations, citizens and customers.

"Stakeholder engagement involves interactive processes of engagement with relevant stakeholders, through, for example, meetings, hearings or consultation proceedings. Effective stakeholder engagement is characterized by two-way communication and depends on the good faith of the participants on both sides. This engagement can be particularly helpful in planning and in decision-making concerning projects or other activities involving, for example, the intensive use of land or water, which could significantly affect local communities."Footnote 29

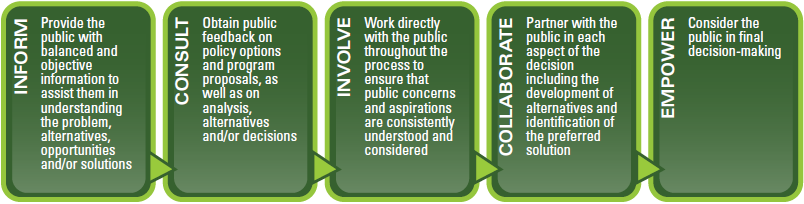

Engagement comprises both formal and informal ways of consulting and achieving the participation of the parties who have an actual or potential interest in, and effect on, your company. Consultation is the process of establishing a two-way dialogue with stakeholders. It implies understanding the views of stakeholders and taking those views into consideration, being accountable to stakeholders when accountability is called for, and using the information learned to drive innovation and business success.

Below are the five basic levels of engagement, adapted from the International Association for Public Participation's Spectrum of Participation.Footnote 30

Note that in this example the stakeholders are always referred to as the public; of course, stakeholders can vary from internal units to external organizations and can represent a wide range of public and private interests.

3.1.2 What are the benefits of stakeholder engagement? Why does it matter?

One way to understand the importance of engagement is to look at what can happen when it is not done: customers see a company as unresponsive to their needs; employees feel unappreciated; suppliers lose trust in a company; communities become uncooperative; and investors get nervous. Three key reasons, therefore, for engagement include building social capital, reducing risk and fuelling innovation. The following table elaborates on these points.

| Benefits |

Outcomes |

|

|---|---|---|

| Build social capital |

|

|

| Reduce risk |

|

|