Table of contents

- Abstract

- 1. Introduction

- 2. Background on the Business Accelerator and Incubator Performance Measurement Framework

- 3. Data

- 4. A profile of the 2020 cohort of companies in the BAI PMF

- 5. Business performance of the 2020 cohort

- 6. Regression analysis of the impact of BAI programming on business performance

- 7. Conclusion

- References

Abstract

Launched in 2016, the Business Accelerator and Incubator Performance Measurement Framework (BAI PMF) project is a voluntary performance measurement initiative co-created by ISED and the Business Accelerator and Incubator (BAI) community. The BAI PMF is a survey created to help improve performance measurement and reporting practices for BAIs across Canada and, over time, to develop a source of data to analyze the impact of BAIs on Canadian start-ups.

This study uses a merger of the 2017–2020 BAI PMF data, the latest available at the time of this study, and Statistics Canada's tax filing data from 2014 to 2020 to bring forward novel insights on the profile of companies receiving BAI support and the impact of BAI support on their economic performance.

Empirical findings indicate that these companies are young, growth-oriented firms with significant levels of R&D engagement. Most importantly, there is early evidence that BAIs are associated with the growth trajectory of high-potential Canadian start-ups. A fixed-effect regression analysis reveals a positive correlation between BAI support and business performance. During the year a company receives assistance from BAI, its employment tends to be 14% higher than that of a similar non-BAI PMF company, while its revenue is higher by 13%. In the subsequent year, a BAI-supported company continues to maintain a 13% higher employment size, although it no longer has an advantage in revenue.

This study establishes a basis for future research opportunities. When more comprehensive data spanning a longer duration become available, it will be possible to explore the long-term effectiveness of BAI services as well as the confounding effects of other government programs.

1. Introduction

Starting a business is a risky endeavour, and it can be even riskier if the business operates in a space requiring a depth of capital and high-skilled talent to bring products and services to market. When such high-potential start-ups scale successfully, they generate large revenues and create a strong demand for well-paid high-skilled talent, spurring local economic growth. Given the potential for these outsized benefits to the economy, governments are keen to sustain the growth of high-potential Canadian start ups and see them scale to become future Canadian anchor companies.

Business accelerators and incubators (BAIs) are viewed as playing a key role in supporting high growth potential Canadian start-ups by being one of their first touch points in their start and scale journey. BAI programs aim to reduce the risk of failure for high growth potential companies, broadening the funnel of Canadian start-ups and accelerating their growth. They offer services like business development, product validation, IP development, and visibility to potential investors and corporate customers. These services help young vulnerable start-ups reduce their risks and help them bring their products to market faster. Policy makers are interested in building out a strong and competitive pipeline of scalable companies and, in service of this objective, have provided significant public support to Canadian BAIs.

The Department of Innovation, Science and Economic Development (ISED) manages the Business Accelerator and Incubator Performance Measurement Framework (BAI PMF) initiative, aimed at evaluating the effectiveness of BAI programs in supporting the growth of high potential start-ups. This voluntary project surveys BAIs and their client companies on an annual basis, employing a national framework that was co-developed by ISED and the BAI community. Using the PMF data, this report brings forward novel insights on the types of companies seeking BAI services and how BAI programming supports their growth.

2. Background on the Business Accelerator and Incubator Performance Measurement Framework

Following an announcement in Budget 2016, ISED convened a Steering Committee of leading Canadian BAIs to create a national BAI PMF project that would benefit the participating BAIs, policymakers, and Canadian entrepreneurs. The Steering Committee developed a national framework and project parameters that would ensure the BAI community's continued trust and engagement in this project (ISED, 2017). The pilot project was launched in 2018 to improve the project's data collection methods and community engagement. In line with the BAI community's feedback, the PMF survey was shortened and data collection methods were simplified. The first findings from this project, based on analysis at Statistics Canada, were shared with the BAI community in 2019 (Williams, 2019).

As the BAI PMF graduated from the project's pilot phase, ISED engaged the Canadian Accelerator and Incubator Network (CAIN), and its subcontractor le Mouvement des accélérateurs d'innovation du Québec (MAIN), to serve as a data collection and ecosystem partner in promoting the survey among BAIs. CAIN and MAIN act as the voice of the BAI community on this project and, in turn, use these roles to advocate for and build engagement with the BAI community. In its role as data collection partner, CAIN simplified the collection process by working with the participants to improve survey data quality. Together, ISED and BAI PMF project partners are building the leading source of national BAI performance data. By linking to tax filing data provided by Statistics Canada, the PMF project has the analytical capabilities to deliver business performance insights.

3. Data

3.1. The BAI PMF Survey

Each BAI administers the survey to their client companies, collects and submits the administrative information of their clients. Given that this is a voluntary survey, the findings only apply to the companies surveyed. The BAI PMF survey includes questions for BAI participants, including the programs offered, and both profile and economic performance questions for client companies. This helps profile each BAI participant and a profile for each program for which they plan to contribute company-level data. In choosing to include a program in the PMF, BAIs are responsible for ensuring recipients of these service provide data for all of the questions and indicators included in the PMF. BAIs should only include data on programs that deliver sustained interventions (e.g., education, advisory, coaching and mentoring services delivered over several months or more) and that cater to growth-focused client firms. BAIs do not include programming or activities that deliver short-term interventions for transient clients (e.g., conferences, "lunch and learns," or walk-in advisory services). Together, profile and program data explain which types of companies are targeted and the nature of support received. Future research will look to include BAI programming as part of the analysis as this survey data improves. The company-level survey is focused on key metrics like company profile, job creation, start-up growth, business operation, and entrepreneurship among underrepresented groups, such as women and racialized communities.

BAI participants have the option of submitting their data through CAIN's secure platform or directly to Statistics Canada. Data submitted to CAIN is reviewed for quality and CAIN works with BAI participants to improve their data submission where necessary. CAIN collates all of the surveys and submits to Statistics Canada for analysis.

3.2. Overview of the participating BAIs

The number of BAI participants has grown over time. Each year's sample is referenced by their cohort year, with BAI participants collecting survey data for the previous calendar year. For example, the 2017 Cohort refers to PMF survey data collected in 2018 for companies that received BAI support in 2017. Table 1 provides a list of BAI participants and the years in which they contributed data to the project.

| BAI | 2017 Cohort | 2018 Cohort | 2019 Cohort | 2020 Cohort |

|---|---|---|---|---|

| Accelerate Okanagan | contributed data | contributed data | contributed data | contributed data |

| Accelerator Centre | contributed data | contributed data | contributed data | - |

| Alacrity Canada | contributed data | contributed data | contributed data | contributed data |

| Bioenterprise Corporation | contributed data | contributed data | contributed data | contributed data |

| Canadian Technology Accelerators (CTA) | - | contributed data | - | - |

| CEIM | contributed data | contributed data | contributed data | contributed data |

| Centech | - | contributed data | contributed data | contributed data |

| Co.Labs | - | contributed data | contributed data | contributed data |

| Communitech | contributed data | contributed data | contributed data | contributed data |

| Cultivator | - | - | contributed data | contributed data |

| Cycle Momentum (Ecofuel) | - | contributed data | - | contributed data |

| District 3 | - | contributed data | contributed data | contributed data |

| DMZ | - | - | - | contributed data |

| Economic Development St. John's | - | - | contributed data | - |

| Espace-inc. | - | - | - | contributed data |

| Esplanade Québec | - | contributed data | contributed data | contributed data |

| FounderFuel | contributed data | contributed data | contributed data | contributed data |

| Genesis Centre | contributed data | contributed data | contributed data | contributed data |

| Highline Beta | contributed data | contributed data | - | contributed data |

| Invest Ottawa | - | contributed data | contributed data | contributed data |

| La Suite Entrepreneuriale (CIDAL) | - | - | - | contributed data |

| LaunchPad PEI | - | - | - | contributed data |

| Lazaridis Institute | contributed data | contributed data | - | - |

| LE CAMP | - | contributed data | contributed data | contributed data |

| L-Spark | contributed data | contributed data | contributed data | contributed data |

| MaRS Data Catalyst | contributed data | contributed data | contributed data | - |

| NextAI | - | - | - | contributed data |

| Northforge | - | - | - | contributed data |

| OAFT | contributed data | contributed data | - | - |

| PEI Bio Alliance | contributed data | contributed data | contributed data | contributed data |

| Planet Hatch | - | contributed data | contributed data | contributed data |

| Platform Calgary | contributed data | contributed data | contributed data | contributed data |

| Propel ICT | contributed data | contributed data | contributed data | contributed data |

| Quantino | - | - | - | contributed data |

| Queen's University | contributed data | contributed data | contributed data | contributed data |

| SFU Ventures | - | - | - | contributed data |

| Startup Zone | - | contributed data | contributed data | - |

| TEC Edmonton | contributed data | contributed data | contributed data | contributed data |

| University of Toronto Entrepreneurship | - | - | - | contributed data |

| Venn Innovation | - | contributed data | contributed data | - |

| VIATEC | contributed data | contributed data | contributed data | - |

| Volta | contributed data | contributed data | contributed data | contributed data |

| Total BAI participants | 20 | 31 | 28 | 33 |

| BAI PMF companies | 539 | 2,461 | 2,116 | 1,877 |

| Source: BAI PMF survey data. | ||||

The BAI PMF project is possible thanks to the data contributions of the BAI participants. The project partners actively engage and welcome new BAI participants to the project, with the goal of including all Canadian BAIs in this initiative.

3.3. The role of Statistics Canada

Data analysis at Statistics Canada significantly expands the research capabilities of this project, particularly in overcoming certain survey data constraints. The PMF survey data at Statistics Canada is matched to the Business Register, Statistics Canada's continuously maintained central repository of baseline information on businesses and institutions operating in Canada. In addition, the PMF survey data is linked to the General Index of Financial Information (GIFI) tax filing data, which fills gaps in the survey data, supplementing it with additional business performance data thereby allowing researchers to track BAI PMF companies both backward and forward in time. The analysis presented in this report is based on Statistics Canada's data. Improvements on PMF survey data are ongoing, and ISED intends to include more findings based on survey data in future research releases. Where available, the report discloses analysis for Ontario and Quebec.

To balance Statistics Canada's extensive powers to collect information, the Statistics Act establishes rigorous legal obligations for Statistics Canada to keep information in trust and use it only for statistical purposes. Data obtained and kept by Statistics Canada cannot be used for non-statistical purposes. Much of Statistics Canada's credibility rests on confidentiality protection as a bedrock condition of operation. Statistics Canada does not publish identifiable information. In addition, a number of policies govern employees' activities.

Only employees with a "need to know" have access to the agency's data holdings, and the linkage of data to other sources must undergo a prescribed review and approval process, which involves the submission of documented proposals to senior management. These measures provide BAI participants a high degree of confidence in the BAI PMF project's data management practices.

Table 2 shows that the raw BAI PMF data included 8,062 businesses who received BAI services during 2017 to 2020. Among them, around 88.7% were matched with Statistics Canada's tax filing data.

| Cohort | Companies | Matched | Matching Rate |

|---|---|---|---|

| 2017 | 565 | 540 | 95.6% |

| 2018 | 2,964 | 2,675 | 90.2% |

| 2019 | 2,582 | 2,398 | 92.9% |

| 2020 | 1,951 | 1,539 | 78.9% |

| Total | 8,062 | 7,152 | 88.7% |

| Source: BAI PMF survey data. | |||

3.4. Comparison group

A comparison group was selected to provide a benchmark for analyzing the business performance of BAI participants in the BAI PMF project. From the population of businesses that have never participated in the program of a participating BAI, a sample comprising 1% of the pool was selected by stratified random sampling method for each year from 2017 to 2020.Footnote 1 This sample was restricted to active businesses with 100 or fewer employees. The strata for selection included province, firm size, and industry. Around 41,105 businesses were selected into the comparison group. This comparison group of non-BAI PMF participant companies was used in the statistical summary and in the regression analysis.

4. A profile of the 2020 cohort of companies in the BAI PMF

This study is a part of the BAI PMF research series conducted by ISED's Small Business Branch. The 2017, 2018, and 2019 Cohorts have been discussed in previous reports and, thus, this paper focuses on the 2020 Cohort, the most recent year for which these results were available.

4.1. Geographic distribution

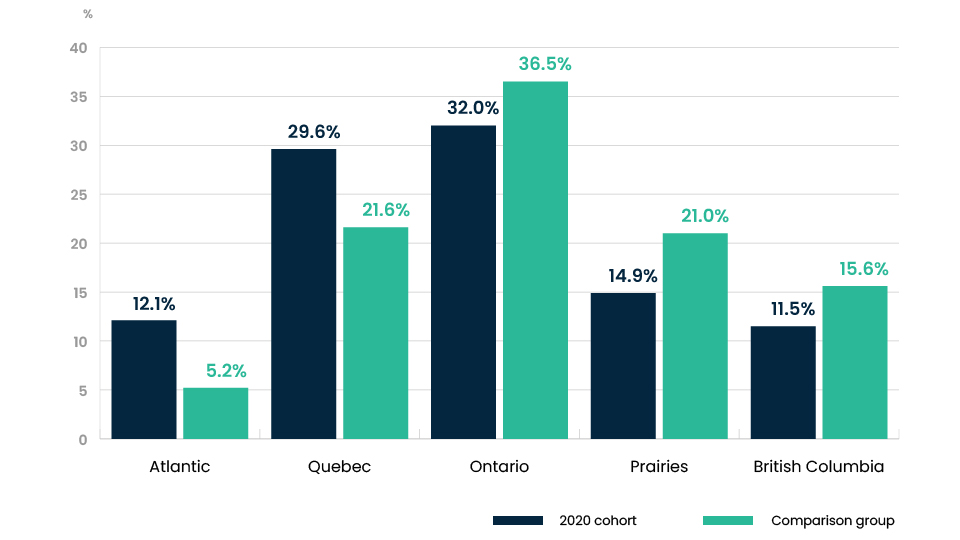

While there are BAI participants from across Canada, Figure 1 shows that the distribution of BAI PMF companies leans toward companies operating in Ontario (32.0%), followed by Quebec (29.6%). The remaining Canadian BAI PMF companies are roughly evenly distributed across Atlantic Canada (12.1%), the Prairies (14.9%), and British Columbia (11.5%). These results may not represent the population of BAI-backed companies, as could be inferred when contrasted against a comparison group of Canadian small businesses.Footnote 2

Figure 1: Geographic distribution of the 2020 PMF cohort and the comparison group, 2020

Sources: BAI PMF survey data, Business Register, and GIFI tax filing data.

4.2. Age distribution

The 2020 Cohort of the BAI PMF companies are younger than the comparison group. Around 40.2% of the BAI PMF companies are between 0 and 2 years and a further 28.6% between 3 and 5 years (Figure 2), while a mere 3% of the comparison group are 0 to 5 years old. Only 10.5% of the BAI PMF companies are over the age of 16, while, on the other hand, half of the comparison group are over 21 years of age, with the general age distribution skewed to being over 11 years of age. The data confirms the expectation that BAIs service very young start-ups. According to an ISED study on seed-stage capital (Tu, Clarke and Dolan, 2022), the average age of an angel investor-backed company is 3, while a venture capital-backed company is 6. This finding suggests that BAIs do act as the first touchpoint for young, high-potential start-ups, with the assumption that BAI-backed companies continue onto the funding escalator.

Figure 2: Age distribution for the 2020 PMF cohort and the comparison group, 2020

Sources: BAI PMF survey data, Business Register, and GIFI tax filing data.

4.3. Industrial distribution

Figure 3 shows that the industrial distribution of the 2020 Cohort is different from that of the comparison group. Around 45.2% of the BAI companies are in Professional, Scientific and Technical Services, whereas only 13.3% of the comparison group are in this sector. The second-largest group of the 2020 Cohort is the Manufacturing sector, whose share is 17.1%, but the proportion for the comparison group is only 4.0%. The smallest sector is Finance and Insurance (1.0%) for the 2020 cohort, but almost one tenth of the comparison group is in this sector. Moreover, for two other large sectors from the comparison group, Mining, Quarrying, and Oil and Gas Extraction, Utilities, Construction (12.8%) and Real Estate and Rental and Leasing (10.5%), their coverage in the 2020 Cohort is only 1.4% and 2.4% respectively.

Figure 3: Industrial distribution for the 2020 PMF cohort and the comparison group, 2020

Sources: BAI PMF survey data, Business Register, and GIFI tax filing data.

4.4. R&D engagement

Investing in R&D is an important indicator that a company is growth-oriented and, therefore, it is assumed that a high proportion of BAI-backed companies engage in R&D. The research at Statistics Canada examined the proportion of BAI PMF companies engaged in R&D in 2020, which was pulled from tax filing data where a company indicates whether or not they have spent on R&D in the year in which they participated in a BAI program. As expected, the proportion of BAI PMF companies engaging in R&D is high. For the 2020 Cohort, R&D engagement was at 21.7%, whereas the proportion for the comparison group is only 1.3% (Figure 4). For companies based in Ontario in this cohort, engagement stands at 30.6%, while in Quebec it is 26.4%.

Figure 4: Proportion of companies engaged in research and development, 2020

Sources: BAI PMF survey data, Business Register, and GIFI tax filing data.

4.5 Women's ownership

Actively supporting and reducing barriers for women entrepreneurs is an important policy priority of the Government of Canada that encourages the full and equal participation of women in the Canadian economy. A business is considered primarily owned by a woman if she has the largest share or the highest position among the major owners with equal shares. For the 2020 Cohort, 24% of the companies are majority women-ownership, while the comparison group of Canadian small businesses stands at 25%. Provincial-level data was available for Ontario and Quebec for companies in the 2020 Cohort, and 28% of companies in Ontario are majority women-owned and 22% in Quebec.

5. Business performance of the 2020 cohort

5.1. Employment

Figure 5 shows that companies in the 2020 Cohort are small, which is in line with expectations as the typical BAI client is a young start-up. Almost half of the 2020 Cohort, or 47%, has between 1 and 5 employees. Interestingly, the 2020 Cohort companies are slightly larger in the 6 to 10 and 11 to 20 employee category when contrasted with the comparison group.

Figure 5: Firm size of the 2020 PMF cohort and the comparison group, 2020

Sources: BAI PMF survey data, Business Register, and GIFI tax filing data.

There are two sets of definitions for high-growth firms. Using the definition developed by the Organization for Economic Cooperation and Development (OECD), a high-growth firm has an average annualized growth in employees greater than 20% per year, over a three-year period, and with ten or more employees at the beginning of the observation period (Eurostat-OECD, 2007).

Alternatively, according to the U.S. Bureau of Labor Statistics' (BLS) definition, a company is considered a high-growth firm when: (a) for companies with fewer than ten employees at the beginning of the period grow by eight or more employees over a three-year period, or (b) companies with ten employees or more has an average annualized growth greater than 20% per year over a three-year period (or 72.8% over the three-year period) (Clayton et al., 2013).

As shown in Figure 6, by either definition, the 2020 Cohort exhibits a significantly higher percentage of high-employment-growth firms than the comparison group.Footnote 3 Under the OECD definition, around 6.1% of the 2020 Cohort qualifies as high-growth firms, in contrast with 0.4% for the comparison group. When the BLS definition is used, the proportion of high-growth firms becomes 10.0% within the 2020 Cohort, while only 1.04% for the comparison group.

Figure 6: Share of high-employment-growth companies

Sources: BAI PMF survey data, Business Register, and GIFI tax filing data.

5.2. Average salary

The salary information was drawn from Canada Revenue Agency's (CRA) payroll deduction data. The average salary is the total wage bill divided by the number of employees. We stratified the 2020 Cohort's average wages into quartiles.Footnote 4 Figure 7 presents the first, second, and third quartiles of the 2020 Cohort and of the comparison group over a five-year period. The quartile values for the comparison group have also been included in Figure 7 to help compare against BAI PMF companies. The samples are restricted to businesses who report salary and employment information for each year from 2016 to 2020. After this filter, there are 124 businesses from the 2020 cohort and 16,445 businesses from the comparison group.

In general, the 2020 Cohort's average salaries are trending up from 2016 to 2020. At each quartile, the BAI PMF companies paid a higher average salary than the comparison group, and the gap widened over time.

For example, in 2016, the second quartile of the average salary (median) for the 2020 Cohort is $40,747, around 8.5% higher than the comparison group ($37,561). In 2020, the BAI PMF companies ($56,204) are 42% higher than the comparison group ($39,645).

The higher average wages paid out by the BAI PMF companies suggest either a greater investment in their talent or that those jobs command a higher salary than those of the comparison group.

Figure 7: Average salaries by quartile for the 2020 cohort and the comparison group, 2016–2020

Sources: BAI PMF survey data, Business Register, and GIFI tax filing data.

5.3. Revenue

Like average salaries, the revenues of the 2020 Cohort and the comparison group are also stratified into quartiles over the period from 2016 to 2020. Figure 8 shows the difference between these two groups. Again, the sample only contains businesses whose revenue information is available for each one of the five consecutive years.

In general, the 2020 Cohort enjoyed an increase in revenue at each level of quartile. For example, the third quartile revenue started at $586,352 in 2016, increasing significantly to $754,217 in 2018, with a final revenue figure of $978,881 in 2020, that is, a 67% increase in five years. By contrast, the comparison group's revenue has been relatively stable during the same period and they even experienced a decline in 2020.

It should be noted that the 2020 PMF Cohort primarily consists of young companies and 2020 was the year in which they participated in a BAI program. Therefore, it is not surprising that the BAI PMF companies exhibited lower revenue figures than the comparison group from 2016 to 2020.

Figure 8: Revenue quartile for the 2020 cohort and the comparison group, 2016–2020

Sources: BAI PMF survey data, Business Register, and GIFI tax filing data.

Considering the diversity in business regulations and environments across provinces, it is interesting to examine the business performance of the BAI PMF companies by region. However, due to a lack of observations, only Ontario and Quebec have enough observations for the quartile analysis.

The revenue level of each quartile is shifted up for the 2020 Cohort companies based out of Ontario (67 businesses) and Quebec (69 businesses), as shown in Figures 9 and 10 below. In 2020, the first quartile revenue for Ontario stands at $51,113, the second quartile at $201,028, while the third quartile revenue stands at $1,355,453. For Quebec in 2020, the first quartile revenue is $100,000, the second quartile stands at $274,520, and the third at $1,019,524. Across all the quartiles, the revenue levels in 2020 across all quartiles in both provinces are higher than the combined 2020 Cohort's revenue quartiles.

Figure 9: Revenue quartile for Ontario-based companies in the 2020 cohort, 2016–2020

Sources: BAI PMF survey data, Business Register, and GIFI tax filing data.

Figure 10: Revenue quartile for Quebec-based companies in the 2020 cohort, 2016–2020

Sources: BAI PMF survey data, Business Register, and GIFI tax filing data.

6. Regression analysis of the impact of BAI programming on business performance

The performance indicators discussed in the preceding section are descriptive statistics. Simply comparing these figures between the BAI PMF companies and the comparison group could be misleading, as these figures do not account for additional factors that could influence business performance. Therefore, this study used a regression analysis to investigate the influence of BAI programming services on a company's performance while accounting for other pertinent variables.

A fixed effect regression model was used to estimate the impact on company performance, which was measured by employment growth and revenue growth. The following function is estimated to consider the impact of BAI services on business performance:

(1)

where,

- measures the business performance of firm, it is either the number of employees or total revenue in year ;

- is a binary variable indicating whether a firm received BAI services in year ; Its coefficient estimate then measures the effect of BAI services on business performance;

- Subscript refers to the year before the reference year; therefore , the coefficient of , measures the effect of BAI on business performance ( ) in the subsequent year;

- is a vector of age groups observed in year , including 0–2 year (reference category), 3–5 years, 6–10 years, 11–15 years, 16–20 years, and 21 years or older;

- is the geographic location where the firm is located, including Ontario (reference category), Quebec, British Columbia, and the rest of Canada;

- refers to the firm's industrial sector, as measured by the two–digit North American Industry Classification System; the reference category is Professional, Scientific, and Technical Services;

- is a vector of firm characteristic variables, including the total assets, expenses, and liabilities in the previous year; for the model whose dependent variable is revenue, includes a set of categorical variables for the number of employees; for the model whose dependent variable is employment, includes the lagged revenue variable;Footnote 5

- are the unobserved time-invariant individual effects;

- is an independent and identically distributed residual.

6.1. Descriptive statistics

For the regression analysis, all four BAI PMF cohorts were included. Table 3 presents the descriptive statistics for the data. It is an unbalanced panel with around 32,352 businesses and 193,527 observations.Footnote 6

On average, BAI PMF companies have a higher level of employment than the non-BAI PMF companies, but their revenue is slightly lower. In the year before participating in a BAI program, these recipients' total asset is lower than the non-recipients, but their expenses and liability are higher.

In the year of participating in a BAI program, PMF companies had a higher representation among the employment groups with more than 5 employees, compared with the non-BAI PMF companies. The sample distribution also showed that PMF companies tend to be younger and more likely to cluster in Ontario than the non-BAI PMF companies. More than half of the PMF companies operate in the Professional, Scientific, and Technical Services sector, whereas this share is only 16% for the non-BAI PMF companies.

| - | Total | BAI | Non-BAI | |||

|---|---|---|---|---|---|---|

| Mean (1) |

SD (2) |

Mean (3) |

SD (4) |

Mean (5) |

SD (6) |

|

| ln(Employment) | 1.38 | 1.13 | 1.95 | 1.17 | 1.37 | 1.12 |

| ln(Revenue) | 12.40 | 3.02 | 12.28 | 3.27 | 12.40 | 3.01 |

| ln(Asset), lagged | 12.54 | 2.50 | 12.31 | 2.69 | 12.55 | 2.49 |

| ln(Expenses), lagged | 12.42 | 2.53 | 12.74 | 2.67 | 12.42 | 2.52 |

| ln(Liability), lagged | 11.64 | 2.69 | 12.28 | 2.67 | 11.63 | 2.69 |

| Firm size | ||||||

| 0 employees | 0.21 | 0.41 | 0.09 | 0.29 | 0.21 | 0.41 |

| 1–5 employees | 0.50 | 0.50 | 0.41 | 0.49 | 0.50 | 0.50 |

| 6–10 employees | 0.12 | 0.32 | 0.19 | 0.40 | 0.12 | 0.32 |

| 11–20 employees | 0.09 | 0.28 | 0.15 | 0.36 | 0.08 | 0.28 |

| 21–50 employees | 0.06 | 0.24 | 0.10 | 0.30 | 0.06 | 0.24 |

| 51+ employees | 0.03 | 0.17 | 0.06 | 0.23 | 0.03 | 0.17 |

| Firm age | ||||||

| 0–2 years | 0.03 | 0.17 | 0.22 | 0.41 | 0.03 | 0.16 |

| 3–5 years | 0.04 | 0.18 | 0.38 | 0.48 | 0.03 | 0.17 |

| 6–10 years | 0.14 | 0.35 | 0.25 | 0.43 | 0.14 | 0.34 |

| 11–15 years | 0.25 | 0.43 | 0.08 | 0.28 | 0.25 | 0.43 |

| 16–20 years | 0.23 | 0.42 | 0.04 | 0.19 | 0.24 | 0.42 |

| 21+ years | 0.32 | 0.47 | 0.04 | 0.19 | 0.32 | 0.47 |

| Region | ||||||

| Ontario | 0.37 | 0.48 | 0.58 | 0.49 | 0.37 | 0.48 |

| Quebec | 0.20 | 0.40 | 0.16 | 0.36 | 0.20 | 0.40 |

| British Columbia | 0.16 | 0.36 | 0.10 | 0.29 | 0.16 | 0.37 |

| Prairies | 0.21 | 0.41 | 0.09 | 0.28 | 0.22 | 0.41 |

| Atlantic | 0.06 | 0.23 | 0.08 | 0.27 | 0.06 | 0.23 |

| Other | 0.00 | 0.04 | - | - | - | - |

| Industry | ||||||

| Agriculture, Forestry, Fishing and Hunting | 0.05 | 0.21 | 0.01 | 0.12 | 0.05 | 0.21 |

| Mining, Quarrying, and Oil and Gas Extraction, Utilities, Construction | 0.14 | 0.34 | 0.01 | 0.12 | 0.14 | 0.35 |

| Manufacturing | 0.06 | 0.23 | 0.15 | 0.36 | 0.06 | 0.23 |

| Wholesale Trade | 0.06 | 0.23 | 0.03 | 0.17 | 0.06 | 0.23 |

| Retail Trade | 0.09 | 0.28 | 0.05 | 0.22 | 0.09 | 0.28 |

| Transportation and Warehousing | 0.06 | 0.23 | 0.01 | 0.08 | 0.06 | 0.23 |

| Information | 0.02 | 0.14 | 0.09 | 0.29 | 0.02 | 0.13 |

| Finance and Insurance | 0.04 | 0.20 | 0.02 | 0.15 | 0.04 | 0.21 |

| Real Estate and Rental and Leasing | 0.06 | 0.24 | 0.01 | 0.09 | 0.06 | 0.24 |

| Professional, Scientific, and Technical Services | 0.16 | 0.37 | 0.53 | 0.50 | 0.16 | 0.36 |

| Management of Companies and Enterprises, Administrative and Support and Waste Management and Remediation Services | 0.06 | 0.23 | 0.03 | 0.16 | 0.06 | 0.23 |

| Educational Services | 0.01 | 0.11 | 0.01 | 0.12 | 0.01 | 0.11 |

| Health Care and Social Assistance | 0.06 | 0.25 | 0.02 | 0.15 | 0.07 | 0.25 |

| Arts, Entertainment, and Recreation, Accommodation and Food Services | 0.06 | 0.24 | 0.01 | 0.10 | 0.06 | 0.24 |

| Public Administration and Other Services | 0.08 | 0.26 | 0.01 | 0.10 | 0.08 | 0.27 |

| Count |

193,527 |

3,642 |

189,885 |

|||

|

Sources: BAI PMF survey data, Business Register, and GIFI tax filing data. |

||||||

6.2. Regression results for the employment model

Using the logarithm of employment as the dependent variable, the regression results of Equation (1) are presented in Table 4. The first column includes only participation in a BAI program for the present year, while the second column adds to the regression the lagged BAI variable that indicates participation in a BAI program in the previous year.

The regressions find a positive and statistically significant impact of participation in a BAI program on the recipients' employment. The coefficients of the present BAI variables exhibit nearly the same magnitudes in both columns of Table 4, indicating the robustness of the model specifications and empirical outcomes. The following discussion will therefore focus on the second column of Table 4, given its more comprehensive model representation.

Since the regression model has a log-linear format, the effect of BAI can be calculated as the exponential of the coefficient ( ) minus one (that is, ). Therefore BAI's coefficient of 0.131 indicates that in the year when a company participates in a BAI program, its employment is 14.0% more than a non-recipient.Footnote 7

The coefficient of the lagged BAI variable (0.123) captures the second-year effect of BAI services. It implies that, in the year after a company receives support from BAI, its employment is 13.1% higher than a similar non-BAI company.Footnote 8 This finding reflects the timing of business operations, as it commonly requires several months or even over a year for a company to leverage the support from BAIs for business expansion.

The estimated coefficients of the other control variables in column (2) indicate that the employment size of a company is determined by a variety of factors. Companies aged 3 to 5 years, 6 to 10 years, and 11 to 15 years all hire more employees than the reference group consisting of businesses aged two years or younger. For example, the coefficient of the 6 to 10 age group is 0.117, implying that businesses in this group have 12.4% more employees than the default group.Footnote 9 On the other hand, firms older 20 years tend to have a smaller employment size than the reference group, as indicated by its negative coefficient estimate.

Businesses located in British Columbia, Quebec, Prairies, Atlantic, and all other regions combined do not exhibit a significantly different size of employment than Ontario.

Compared with the default industrial sector (Professional, Scientific, and Technical Services), businesses in Agriculture, Forestry, Fishing and Hunting, Manufacturing, as well as Retail Trade hire fewer employees. For example, the 0.118 coefficient estimate implies that companies in the primary industry hire 12.5% more employees than those in the professional service sector.Footnote 10

The coefficients of the lagged financial indicators measure the effects of these factors on the employment in the following year. Given the log-log specification of these variables, their coefficient estimates can be considered as the elasticity between the dependent variable and the independent variables. For example, a 10% rise in a company's revenue is associated with a 0.09% increase in the following year's employment size.Footnote 11

| - | (1) | (2) |

|---|---|---|

| BAI | 0.130Footnote *** (0.011) |

0.131Footnote *** (0.011) |

| BAI, lagged | - | 0.123Footnote *** (0.014) |

| Firm age (reference: Age 0–2) | ||

| 3–5 years | 0.048Footnote *** (0.012) |

0.037Footnote *** (0.012) |

| 6–10 years | 0.140Footnote *** (0.015) |

0.117Footnote *** (0.015) |

| 11–15 years | 0.099Footnote *** (0.015) |

0.075Footnote *** (0.015) |

| 16–20 years | 0.039Footnote ** (0.015) |

0.016 (0.015) |

| 21+ years | -0.025 (0.016) |

-0.048Footnote *** (0.016) |

| Region | ||

| Atlantic | -0.003 (0.108) |

-0.001 (0.108) |

| Quebec | 0.053 (0.072) |

0.057 (0.072) |

| Prairies | 0.053 (0.062) |

0.061 (0.062) |

| British Columbia | 0.075 (0.057) |

0.084 (0.057) |

| Other | 0.143 (0.130) |

0.143 (0.130) |

| Industry (reference: Professional, Scientific, and Technical Services) | ||

| Agriculture, Forestry, Fishing and Hunting | 0.115Footnote ** (0.048) |

0.118Footnote ** (0.048) |

| Mining, Quarrying, and Oil and Gas Extraction, Utilities, Construction | 0.058 (0.046) |

0.061 (0.046) |

| Manufacturing | 0.073 (0.047) |

0.076Footnote * (0.046) |

| Wholesale Trade | -0.012 (0.048) |

-0.012 (0.047) |

| Retail Trade | 0.082 (0.051) |

0.086Footnote * (0.051) |

| Transportation and Warehousing | 0.015 (0.074) |

0.017 (0.074) |

| Information | -0.028 (0.058) |

-0.026 (0.057) |

| Finance and Insurance | -0.011 (0.057) |

-0.009 (0.056) |

| Real Estate and Rental and Leasing | 0.006 (0.044) |

0.009 (0.044) |

| Management of Companies and Enterprises, Administrative and Support and Waste Management and Remediation Services | 0.005 (0.039) |

0.007 (0.039) |

| Educational Services | 0.072 (0.075) |

0.070 (0.075) |

| Health Care and Social Assistance | -0.002 (0.063) |

0.001 (0.062) |

| Arts, Entertainment, and Recreation, Accommodation and Food Services | 0.028 (0.053) |

0.031 (0.052) |

| Public Administration and Other Services | 0.055 (0.049) |

0.057 (0.048) |

| ln(Asset), lagged | 0.029Footnote *** (0.002) |

0.028Footnote *** (0.002) |

| ln(Expenses), lagged | 0.047Footnote *** (0.002) |

0.047Footnote *** (0.002) |

| ln(Liability), lagged | 0.016Footnote *** (0.002) |

0.016Footnote *** (0.002) |

| ln(Revenue), lagged | 0.010Footnote *** (0.001) |

0.009Footnote *** (0.001) |

| Constant | 0.022 (0.055) |

0.055 (0.055) |

| Observations | 193,527 | 193,527 |

| R-squared | 0.070 | 0.071 |

| Number of businesses | 32,352 | 32,352 |

|

Sources: BAI PMF survey data, Business Register, and GIFI tax filing data. Robust standard errors in parentheses.Footnote 12. |

||

6.3. Regression results for the revenue model

Table 5 presents fixed effect regression results for the model whose dependent variable is the logarithm of revenue. The sample includes 32,216 companies that cover 190,922 observations during the period from 2014 to 2020. The regression for the first column contains the present BAI indicator (i.e., participation in a BAI program in that year), whereas that for the second column includes both the present and the lagged BAI indicators. Again, the regression results are robust with the inclusion of the lagged BAI variable and, thus, the following discussion will concentrate on statistics in the second column.

The coefficient of the present BAI variable (0.122) indicates that, in the year of participating in a BAI program, a company's revenue is 13.0% higher than its non-BAI PMF counterpart.Footnote 13 The lagged BAI indicator, on the other hand, is statistically insignificant, which implies that the effect of BAI programming on a company's revenue diminishes in one year after participating in a BAI program.

In this revenue model, the age variables show a different pattern. Compared with the companies aged two years or younger, those aged 3 to 5 years and 6 to 10 years are not significantly different. For the other age groups, their revenues are significantly lower than the default group and there seems to be a negative relationship between revenue and age. For example, for businesses older than 20 years, their revenue is 84% lower than the youngest group.Footnote 14

Among the regions, Quebec companies seem to earn more revenue than those located in Ontario. There is no significant difference between the Professional, Scientific, and Technical Services sector and the other industries.

The coefficients of the lagged financial indicators are significantly positive. For every 1% increase in total assets, there is a 0.160% rise in the next year's revenue. Likewise, a 1% rise in total expenses is associated with a 0.407% increase in revenue in the following year.

Since the default employment groups represent companies without any employees, the coefficients of the categorical variables reveal a positive correlation between employment size and revenue: larger companies tend to earn higher revenue. For example, compared with the zero-employment companies, those with 1 to 5 employees exhibit a revenue higher by 219%, while the revenue of those with over 50 employees is 619.9% higher.Footnote 15

| - | (1) | (2) |

|---|---|---|

| BAI | 0.122Footnote *** (0.040) |

0.122Footnote *** (0.040) |

| BAI, lagged | - | -0.067 (0.048) |

| Firm age (reference: Age 0–2) | ||

| 3–5 years | -0.032 (0.041) |

-0.026 (0.040) |

| 6–10 years | 0.053 (0.044) |

0.065 (0.044) |

| 11–15 years | -0.174Footnote *** (0.044) |

-0.161Footnote *** (0.044) |

| 16–20 years | -0.404Footnote *** (0.045) |

-0.392Footnote *** (0.045) |

| 21+ years | -0.622Footnote *** (0.046) |

-0.610Footnote *** (0.046) |

| Region (reference: Ontario) | ||

| Atlantic | 0.181 (0.466) |

0.180 (0.466) |

| Quebec | 0.748Footnote ** (0.317) |

0.746Footnote ** (0.317) |

| Prairies | 0.395 (0.268) |

0.391 (0.268) |

| British Columbia | 0.194 (0.275) |

0.190 (0.275) |

| Other | -3.135Footnote * (1.906) |

-3.137Footnote * (1.906) |

| Industry (reference: Professional, Scientific, and Technical Services) | ||

| Agriculture, Forestry, Fishing and Hunting | 0.060 (0.103) |

0.058 (0.103) |

| Mining, Quarrying, and Oil and Gas Extraction, Utilities, Construction | 0.060 (0.129) |

0.058 (0.129) |

| Manufacturing | 0.077 (0.088) |

0.075 (0.088) |

| Wholesale Trade | -0.012 (0.048) |

-0.012 (0.047) |

| Retail Trade | 0.142 (0.122) |

0.140 (0.122) |

| Transportation and Warehousing | -0.062 (0.151) |

-0.064 (0.151) |

| Information | -0.097 (0.162) |

-0.098 (0.162) |

| Finance and Insurance | -0.107 (0.131) |

-0.109 (0.131) |

| Real Estate and Rental and Leasing | -0.000 (0.098) |

-0.001 (0.098) |

| Management of Companies and Enterprises, Administrative and Support and Waste Management and Remediation Services | 0.061 (0.091) |

0.060 (0.091) |

| Educational Services | -0.100 (0.173) |

-0.099 (0.173) |

| Health Care and Social Assistance | 0.010 (0.133) |

0.008 (0.133) |

| Arts, Entertainment, and Recreation, Accommodation and Food Services | -0.037 (0.127) |

-0.039 (0.127) |

| Public Administration and Other Services | -0.001 (0.105) |

-0.003 (0.105) |

| ln(Asset), lagged | 0.160Footnote *** (0.013) |

0.160Footnote *** (0.013) |

| ln(Expenses), lagged | 0.407Footnote *** (0.011) |

0.407Footnote *** (0.011) |

| ln(Liability), lagged | 0.089Footnote *** (0.008) |

0.089Footnote *** (0.008) |

| Firm size (reference: Employment is 0) | ||

| 1–5 employees | 1.161Footnote *** (0.032) |

1.160Footnote *** (0.032) |

| 6–10 employees | 1.468Footnote *** (0.039) |

1.467Footnote *** (0.039) |

| 11–20 employees | 1.646Footnote *** (0.047) |

1.647Footnote *** (0.047) |

| 21–50 employees | 1.844Footnote *** (0.058) |

1.848Footnote *** (0.058) |

| 51+ employees | 1.966Footnote *** (0.072) |

1.974Footnote *** (0.072) |

| Constant | 3.230Footnote *** (0.225) |

3.210Footnote *** (0.227) |

| Observations | 190,922 | 190,922 |

| R-squared | 0.193 | 0.193 |

| Number of businesses | 32,216 | 32,216 |

|

Sources: BAI PMF survey data, Business Register, and the GIFI tax filing data. Robust standard errors in parentheses. |

||

It is possible that companies who participate in a BAI program tend to have a stronger motivation in business success than those who do not turn to a BAI. In other words, if there is an unobserved firm characteristic affecting both the likelihood of receiving BAI support and the company's recruitment or sales, the regressions are then subject to a potential selection bias problem. However, due to a lack of variables on a company's motivation, it is difficult to apply a correction method to mitigate the bias. We also tried to add to the model other independent variables, such as profitability, but the regression results are similar to the current ones. Therefore, the estimated effects from Table 4 and 5 can be treated as an upper bound of the effect of BAI services on business performance.

7. Conclusion

The BAI PMF project is producing leading research on how BAIs impact the growth of the start-ups. The BAIs participating in this project want to demonstrate the value they provide to start-ups, recognizing they are the beneficiaries of significant public funding. This project is producing early evidence that BAIs have a significant impact on the growth trajectory of high potential Canadian start-ups.

This study uses a merger of the BAI PMF data and Statistics Canada's tax filing data to provide an overview of the characteristics of the BAI-supported companies and to assess the business performance of these companies.

The statistical summary indicates that the 2020 Cohort of BAI PMF companies tends to be younger and concentrated within the Professional, Scientific, and Technical Services sector, with a majority located in Ontario and Quebec. These companies demonstrate a greater inclination to invest in research and development, compared with the comparison group.

While the distribution of employment among BAI PMF companies is similar to that of the comparison group, BAI PMF companies exhibit a higher proportion of high employment growth, as defined by either OECD criteria or the BLS criteria. Between 2016 and 2020, the 2020 Cohort consistently paid higher salaries than the comparison group across each quartile, albeit with generally lower revenue levels across these quartiles.

By controlling for the influences from other factors, a fixed-effect regression analysis reveals a positive correlation between BAI support and business performance. In the year a PMF company received support from a BAI, its employment tends to be 14% higher compared with that of a similar non-PMF company, while its revenue is higher by 13%. In the subsequent year, the PMF company continued to maintain a 13% higher employment size, although the company no longer has an advantage in revenue. Limited by data availability, the current research focuses on the one- and two-year effects of BAI services. Future research will examine additional years following BAI graduation to understand whether there are long-term effects. In addition, the extensive data will also allow researchers to explore the long-term effect of R&D on these companies.

This research suggests that BAIs do work with high potential start-ups and that, by participating in a BAI, these start-ups are receiving important services that assist their growth in employment and revenue. It is possible that these new enterprises also receive various types of support from other government programs. When new data sources emerge, ISED can incorporate them into the research series to explore the confounding effects of multiple programs, which will help refine future policies in this space.

References

Clayton, R., Sadeghi, A., Spletzer, J. R., and Talan, D. M. (2013) "High-employment-growth firms: defining and counting them." Monthly Labor Review, June 2013, U.S. Bureau of Labor Statistics, Ottawa, Canada.

Eurostat–OECD (2007) " Manual on Business Demography Statistics," Paris: OECD.

Tu, J., Clarke, W., and Dolan, S. (2022) "Untangling the seed and early-stage funding environment in Canada," Innovation, Science and Economic Development Canada, Small Business Branch, Ottawa, Canada.

Williams, A. (2019) "BAI performance measurement framework: Key findings," Innovation, Science and Economic Development Canada, Ottawa, Canada.

Innovation, Science and Economic Development Canada (ISED) (2017) "BAI National Dialogue Summary."